在英国,一场大规模的生活成本危机可能会彻底停止国民经济的增长。随着税收上升和通货膨胀率升至10%,预计消费者和企业将控制支出。在这种情况下,第四季度可以实现的最大产量与2021年第四季度的数据相差无几。

英国制造业协会(association of manufacturers of Great Britain)在6月8日发布的报告中称,第二和第三季经济勉强维持在低位,今年最后三个月甚至会略有萎缩。总的来说,2023年,GDP将仅增长0.6%,远低于英格兰银行的官方预测。

随着物价上涨降低了家庭生活水平,增加了企业及其员工的成本,英国陷入衰退的风险越来越大。

经济合作与发展组织(OECD)也认同产油国协会的看法,认为明年经济成长有可能停滞,因消费者支出因油价上涨而萎缩。经合组织(OECD)和国际货币基金组织(imf)表示,英国正面临七国集团(G7)工业化国家中最高、最持久的通胀。

价格超压

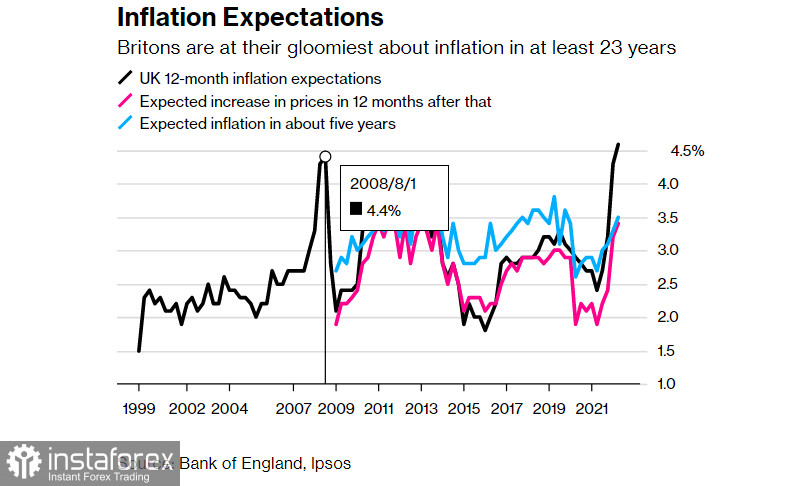

今年4月,通货膨胀率达到了9%的40年来最高水平,预计这一水平甚至还没有达到通常会在10月下降的峰值,届时预计电费将进一步大幅上涨。

今年5月接受调查的消费者预计,未来12个月店内价格将上涨4.6%。这一数字较2月份的4.3%和去年同期的2.4%有所上升。

即使五年后,通货膨胀率仍有望达到3.5%,远高于2%的目标。

总体而言,超过四分之三的英国成年人担心生活成本的上升,低收入和弱势群体表达了最大的担忧。根据英国国家统计局4月份电价上涨后的一项民意调查,16岁以上人群中,77%的人"非常或多少担心"通胀冲击。68%对此感到担忧的人表示,他们已经减少了在生活必需品上的支出。

所有这些都导致了对英国制造商产品需求的下降。在这方面,英国经济中的破产现象已经加剧。

虽然今年前三个月企业和企业家的整体破产率与2021年大致相同,但如果排除最小的公司和在偿债期间被清算的公司,整体情况要糟糕得多。

破产办公室的数据显示,第一季度破产申请增加了一倍多,4月份的初步指导数据显示较上年同期增长21%。随着能源和材料成本的上升,英国企业的日子变得艰难,这一趋势不太可能消退。

另一项私人研究显示,截至3月底,近1900家英国公司陷入财务困境,较上年同期增长19%。

预计今年消费者支出和企业投资的增幅也将低于此前的预期,到2023年将持平。

协会主席对岛上的工业状况表示了极大的关注。

然而,到目前为止,英国央行的态度非常坚决。

值得关注的只有财政部长瑞希·苏纳克的一份声明,即在危机发生时,没有一家英国银行机构有理由要求政府援助。

这一声明并非凭空而来。在此之前,包括汇丰控股(HSBC Holdings plc)、劳埃德银行集团(Lloyds Banking Group plc)和巴克莱银行(Barclays plc)在内的8家主要金融机构对资产进行了传统的自我评估。

所谓的可解性估计首次发表。英国央行在2019年要求银行进行自我检查,但由于新冠肺炎疫情,原定公布日期推迟了。评估将在2024年重复进行,然后每两年进行一次。

每家公司都必须提交一份报告,说明如果公司倒闭,所有重要部门——贷款和吸收存款——将如何继续。和解规定的存在,是为了给当局或新管理层重组或清算公司所需的时间。

例如,巴克莱(Barclays)在其报告中表示,零售银行业务与投资银行业务的分离简化了该集团,并降低了客户和客户在公司其他方面受到干扰或公司动荡影响的可能性。

显然,英格兰银行不仅考虑到了2008年的经历,当时纳税人支付了数十亿英镑来支持苏格兰皇家银行(Royal Bank of Scotland)等机构。据我所知,也考虑到了两年来银行在低息贷款中畅游的超软政策。与2008年一样,这些资金几乎完全流向了次级和投机工具的金融市场,对实际生产的融资几乎没有影响。

这在一定程度上是隔离的结果,因为企业本身要求的贷款减少了,因为面对限制和另一波疫情的威胁,它们不确定是否有能力充分工作。

然而,有一种感觉是,英国财政部终于意识到有必要针对制造商,或至少在行业内提供专门援助。

就减轻英国人的债务负担而言,这也是相当合理的。英国人现在有信心,他们的税收不会被用于向股东派发疯狂的股息或向银行管理层发放奖金。

央行明确表明的立场证实了其意图的严肃性,即即使该银行需要关闭,客户仍将能够像往常一样继续访问他们的账户。

但这其中有一个大问题。

事实上,为了保持经济的持续发展,两年前就应该采取这一步了。如今监管机构的储备已经耗尽,各种扶持和发展资金早已耗尽,艰难的6个月还在前方。

不过,迟做总比不做好。

英国央行(Bank of England)表示有信心认为,被纳入审查的金融机构中不会有一家破产,因为它们的规模都没有大到足以承担系统性风险。

有些令人担忧的是,这些调整机制很大程度上是基于2008年危机的经验。

监管机构的调整计划往往基于一种越来越罕见的假设,即银行将在周五晚上倒闭,公司和监管机构可以在市场休市期间应对后果。

英国对英格兰银行行动的信心正在稳步下跌

报告显示,公众对英格兰银行的信心处于历史低点,英国人预计未来几年通胀率将继续高于目标。

根据英国人对消费价格态度的季度研究,历史上第一次,对央行工作不满的人多于满意的人,而且不能说这是没有根据的。

随着支持率的下降,只有25%的人说他们对英格兰银行的表现感到满意,受访者说他们对通货膨胀的悲观程度比1999年开始这项调查以来的任何时候都要高。

这些结果无疑将加大英国央行行长安德鲁•贝利(Andrew Bailey)及其同事的压力,要求他们在下周史无前例地连续第五次加息。我们可以预期将加息25个基点,使总加息幅度达到1.25%。

这根本不是什么好消息,主要是因为如果人们不再相信央行有能力控制消费价格,他们就有可能寻求更高的工资作为补偿,这可能会导致1970年式的通货膨胀螺旋年,这将导致生活成本更大的增长。

生活费用的上涨将吓跑一些为了赚钱而留在英国的移民。这意味着,这一事件将导致劳动力外流,廉价劳动力更加短缺,需要再次提高生产者的工资。

而这些仅仅是内部经济因素。英国是乌克兰的利益相关者和供应商之一的乌克兰冲突,以及中国正在爆发的冠状病毒,也使预测更加糟糕。

总的来说,英国经济的前景看起来相当黯淡。显然,英国货币也将受到冲击。因此,我们可以预期英镑/美元货币对的趋势将进一步发展。