In recent months, the US economy has emerged as immune to the global downturn and remains relatively strong. This is confirmed by yesterday's increase in the ISM index for services whose values are close to cyclical peaks. This strongly contrasts, for example, with the barometers of the Euroland, which have fallen strongly this year. Only that the strength of the economy will no longer translate into the perception of the Fed's intentions. The FOMC has clearly presented the policy and risk perspectives asymmetric, i.e. better data in the coming weeks will not give rise to more hikes in the upcoming quarters or to raise the target level for interest rates.

The key, of course, is the wage growth, which remains close to 2.8 percent. Every year. The labor market is ruthlessly tightening, which should put pressure on wages also in the coming months. This is, of course, still positive for the USD through a channel of inflation expectations raising the yield on debt and working towards extending the spread of profitability to the debt of other G-10 and EM economies. Only that the impact of the speeding labor market on the valuation of US bonds will be smaller than before because it will not go hand in hand with building expectations for a more hawkish Fed position. In the USD valuation, there is a lot of positive information and the positioning has normalized (investors abandoned the extreme skepticism towards the dollar prevailing in the first quarter). All this indicates that the potential for further appreciation of the dollar has been largely exhausted. The more so because in the valuation of many currencies, the discount of negative factors is evident. This applies, among others euro and pound - both currencies have space to continue to rebound.

In the case of data for June, it is expected that monthly wage growth will be maintained at 0.3%, which, year-on-year, should lead to the equalization of this year's maxima of 2.8%. The rate of creation of new jobs is still well above the ceiling allowing stabilization of the unemployment rate, which, therefore, has a chance to decline from 3.8 to 3.7 percent. The change in non-farm employment is estimated at 195,000, ie on a level consistent with the average value for the last year. It is hard to resist the impression that the bar of expectations is highly suspended, which can only aggravate the negative reaction of the dollar in the event of disappointment. However, it is very unlikely that today's readings would be able to sow seeds of uncertainty about the condition of the American economy.

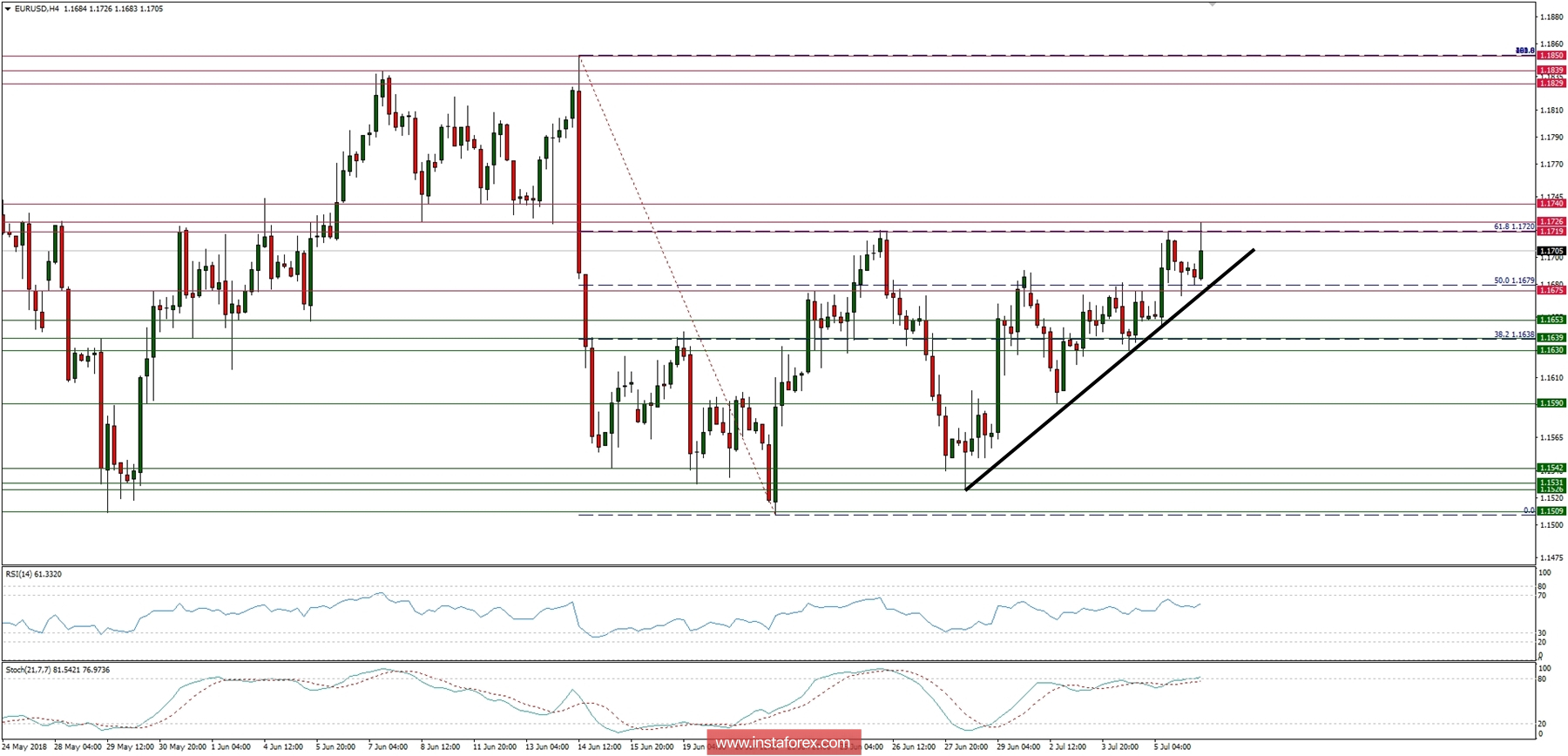

Let's now take a look at the EUR/USD technical picture at the H4 time frame before the NFP Payrolls are released. The market is again testing the 61% Fibo at the level of 1.1720 and this retracement level will play a crucial role during today's NFP data release. Any violation of this level will likely open the road towards the next target at the level of 1.1829. In a case of a worse than expected data, the price might fall below the black intraday trend line support around the level of 1.1670 and head towards the next target at 1.1630.