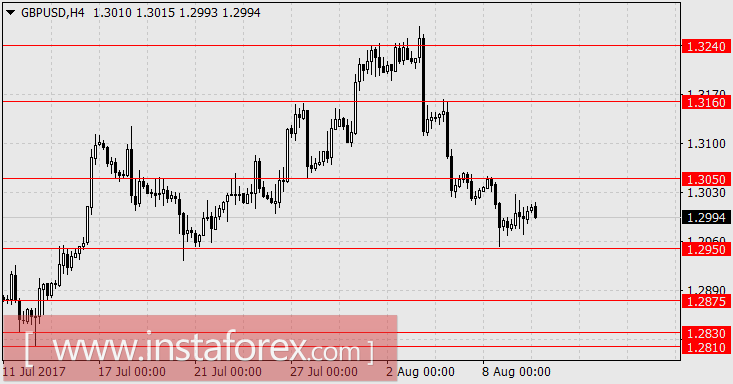

EUR / USD, GBP / USD

On Wednesday, quotes for the euro and the pound have changed a bit, but for meaningful movements, there were no economic or political reasons. Industrial production in Italy in June increased by 1.1% against the forecast of 0.2%. Wholesale inventories in the US in the final estimate for June added 0.7%, but labor costs in the second quarter increased less than the expected 0.6% against 1.1%. The Federal Reserve Bank of Atlanta forecast for GDP for the second quarter still lowered from 3.7% to 3.5%. The stock indices slightly subsided (S & P500 -0.04%, FTSE100 -0.59%) at yesterday's "courtesy exchange" between Pyongyang and Washington, but the declining yields on US government bonds to the close of the day returned to their original positions.

Today, markets can revive, France and Great Britain are entering industrial production in June. The forecast for France is -0.6%, for Great Britain 0.1%. For another country in the euro area, the Italy is also deteriorating the data. The trade balance for June could reach 3.87 billion euros from 4.34 billion before. The UK trade balance is expected to increase from -11.9 billion pounds to -11.0 billion. The production in the construction sector in the UK is projected to grow by 1.4% in June after a reduction of 1.2% in May.

According to the US, producer price indicators will come out for July. The base index is expected to increase by 0.2%, the overall index is 0.1%. At 15:00 London time, the president of the Federal Reserve Bank of New York, William Dudley, speaks on the inequality of salaries in various states. Perhaps, the monetary policy will be affected within the framework of the FRS's dual mandate, which provides for one of the purposes of control over employment. At 19:00 London time, the budget report for July will be published. The forecast is -60.9 billion against -90.2 billion in June. The forecast is excellent, the smallest deficit for the given month since 2008.

Tomorrow, according to the CPI in the US, the indices are expected to grow, we expect the euro to decline to 1.1640, then to 1.1560. For the pound, the first target is the level of 1.2875 and the second target is the range of 1.2810 / 30.

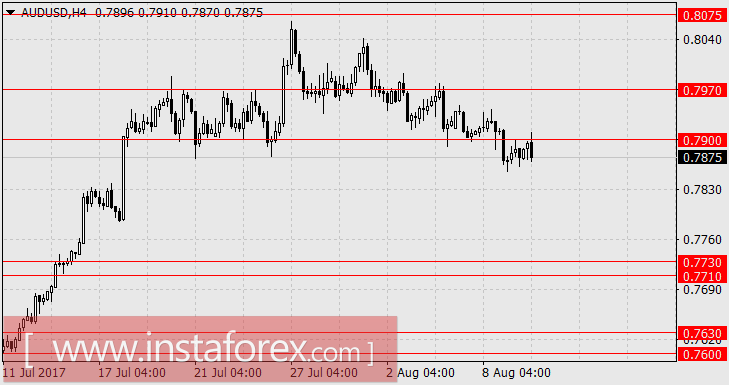

AUD / USD

The Australian dollar is steadily following the strengthening of the US currency (that is, falling against the USD), and if the trend continues, this decline could accelerate. As for example, the decline of the New Zealand dollar, which received a new impetus from the comments of the head of the RNBZ Graham Wheeler at today's meeting of the Central Bank, with the wish to see a lower rate of the national currency. Wheeler exactly repeated the recent statement of his colleague from the RBA, F. Loe, which means full coherence in actions. Yesterday, the consumer sentiment index in Australia fell by 1.2% in August against growth of 0.4% in July. The housing loans in June increased by only 0.5% against expectations of 1.5% and 1.1% a month earlier. The Chinese CPI fell from 1.5% y / y to 1.4% y / y.

The commodity prices are also gradually decreasing: iron ore -0.7%, copper-0.7%, oil slightly increased yesterday, but today it is falling again (-0.03%), meat and grain futures are cheaper from the beginning of the week, The general downward trend in agricultural futures continues from the second decade of July.

We are waiting for prices in the range of 0.7710 / 30.