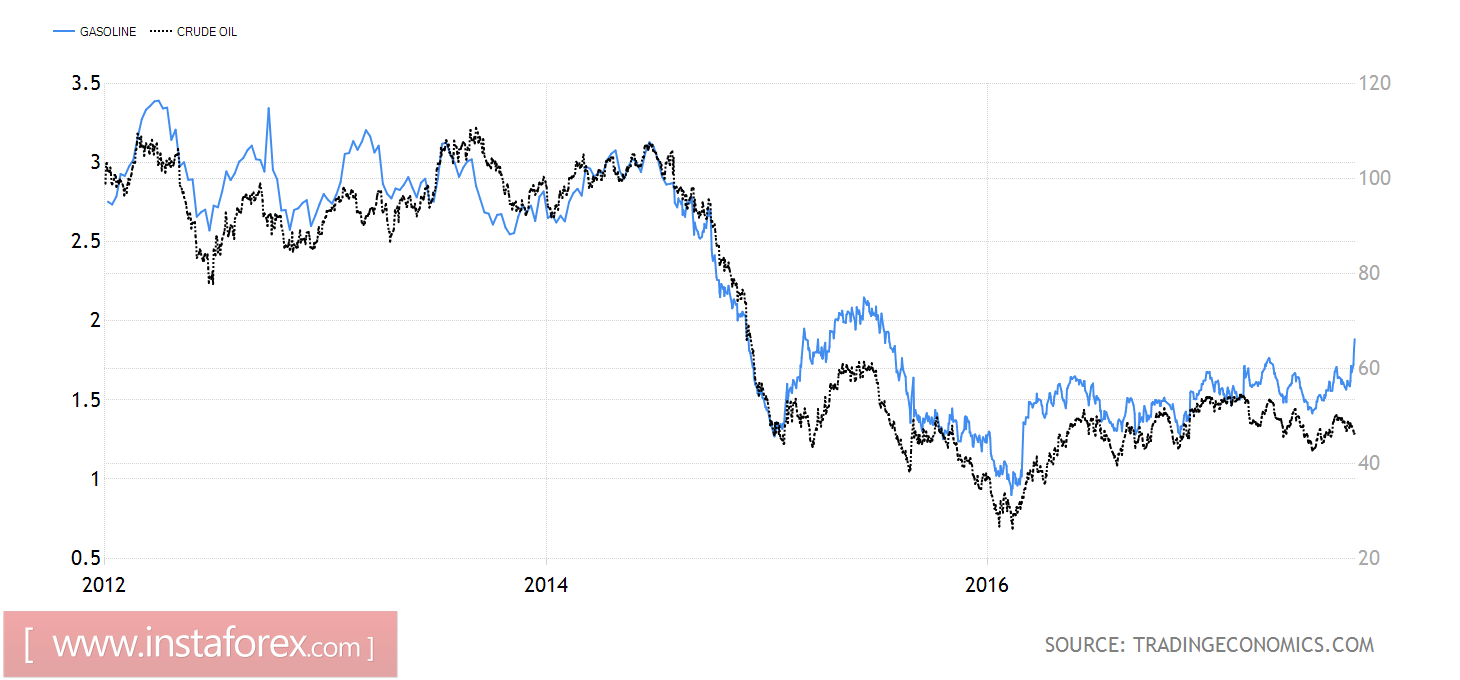

The hurricane, which is the the most destructive storm for the U.S. in the past dozen years and for Texas over the past half century, has forced the oil market to forget about OPEC and global demand, and focus on events taking place in the Gulf of Mexico. This region accounts for 17% of US oil production (9.5 million b/d) and more than 45% of oil refining. It becomes clear why the futures for gasoline soared to the highest level in the past three years, while Brent and WTI retained an inclination for consolidation, and the risks of further movement of quotations are reduced. The lion's share of oil demand is made by oil refineries, which in the Gulf of Mexico are substantially larger than those of the extracting companies.

Dynamics of futures for oil and gasoline

Source: Trading Economics.

As a result, the downward dynamics of US stocks, which faithfully served the bulls for Brent and WTI for the past few weeks, could be their tombstone. According to Goldman Sachs, Harvey will deduct about 1.4 million b/d from the production volume (about 15% of the total in the States), while the refinery with a processing capacity of 4.1 million b/d (23%) work will be in offline mode. Despite the fact that the American Petroleum Institute showed a decrease in stocks by 5.78 million barrels by the end of the week by August 25, and Bloomberg experts expect to see -1.9 million barrels from the US Energy Information Administration, the first figure does not take into account the impact of the hurricane, and the second figure can give an unpleasant surprise to buyers. In any case, to restore the previous dynamics of reserves will take time, while the risks of reducing demand against the background of the end of the driving season in the United States will keep futures under pressure.

Accumulated demand can become a key driver of price changes in the medium term. Goldman Sachs predicts that Harvey will cut 0.2 pp from the US GDP in the third quarter due to a decrease in consumer activity, industrial production and an increase in unemployment. This circumstance is a "bearish" factor for Brent and WTI.

Pressure on oil was created by geopolitics and the strengthening of the US dollar against the backdrop of locking in profits on the "bearish" positions on the American currency. EUR/USD could not gain a foothold above the psychologically significant 1.2 mark on fears of a "dovish" rhetoric of Mario Draghi in September, and large players preferred to increase their lows, which affected other USD pairs and the USD index. At the same time, North Korea described the launch of a ballistic missile flying over Japan as a prelude to an attack on Guam, which increases the risks of military action in Asia and can affect the demand for oil from China and other countries.

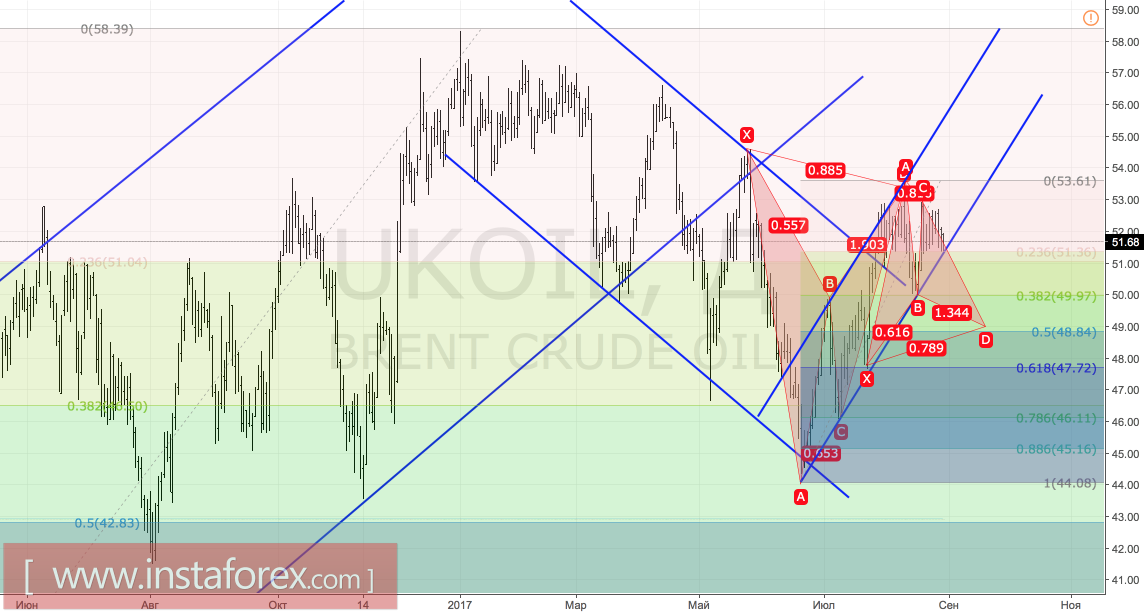

Technically, a breakthrough of support at $51.35 per barrel and the decline of Brent quotes from beyond the upstream trading channel will increase the risks of implementing the Gartley pattern. Its target at 78.6% corresponds to the $49 mark. To restore the "bullish" upward trend it is necessary to return prices to the upper boundary of the consolidation range of $51.5-52.7 and take the resistance by storm.

Brent, daily chart