EUR / USD, GBP / USD

The main event yesterday was the FOMC minutes of the Fed that came out in an expected moderately optimistic tone. According to the famous saying "He who seeks, he will find," therefore, the market agreed that the Committee's forecasts for reducing long-term inflation could lead to a slow down in the Fed's rate increase in the future. The GDP outlook and employment affected by hurricanes came in optimistic. San Francisco Fed President John Williams and Kansas City Fed President Esther George favored the rate increase, however, Chicago Fed President Charles Evans was not yet determined about the December increase. Nevertheless, the indicators for inflation forecasts are very positive which came out on Friday. The basic CPI for September is expected to grow by 0.2%, and could further grow from 1.7% to 1.8% on an annualized basis. The total CPI is expected to grow from 1.9% YoY to 2.3% YoY.

In general, the positive background for the euro was the suspension of independence by the head of Catalonia. The Prime Minister of Spain, Mariano Rajoy, lead the republic about a week in order to smooth out the situation and pledged to preserve unity reconsidering some points of the constitution. Apparently, the administration will not agree and this factor will disappear from the market soon.

But the North Korean factor is becoming more acute. South Korean intelligence reported on the forthcoming nuclear test during the National Congress of the Communist Party of China (CPC) on October 18-19, 2017. While military exercises began between Japan and South Korea expeditiously. Also, US President Trump said that he considers the nuclear deal with Iran which is extremely unfavorable for the US, while preparing to make a statement on this topic in the next few days.

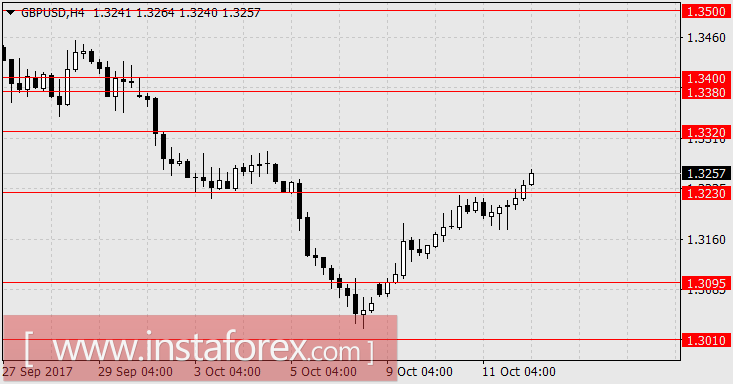

Today, the industrial production data from the eurozone in August will be published with 0.6% forecast. According to the United States, jobless claims are expected to fall from 260,000 to 251,000, while PPI for September is up by 0.4% and base PPI growth is 0.2%. At 17:30, Jerome Powell and Lael Brainard will have their speeches. Today, an auction is held for the placement of 30-year US government bonds worth 12 billion dollars. The US external debt for a month and a half was able to pass from the defrost limit, and increased by 539 billion dollars, to 20.347 trillion. The overall factors do not give us grounds to consider the growth of counter-dollar currencies as some type of stable trend. We are expecting the euro to decline to 1.1775. The risk of continuing short-term growth is possible if Catalonia made a quick decision to "make up" with Madrid. In this case, growth in the range of 1.1970 / 90 is possible. For the British pound, we are expecting a decline to 1.3095, further to 1.3010.

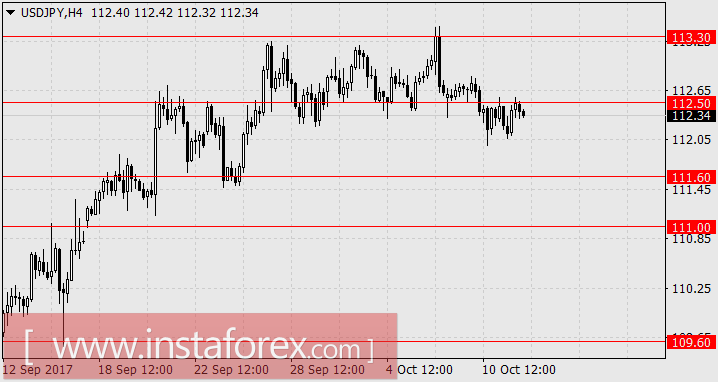

USD / JPY

As expected in the previous forecasts for the yen (10.10), the price failed to grow and continued to fell. Even the excellent data on machine-building orders did not help the yen. On an annual basis, the volume of orders in the machine-building sector increased from 36.2% to 45.3%, while the base order index increased from -7.5% YoY to 4.4% YoY, with the expectations of 0.8% only. The monthly increase for August was 3.4% against expectations of 1.1%. The Japanese yen did not receive support from both government bonds in the US and Japanese securities, while yields change in a narrow range last week. As expected, the United States is interested in low profitability in the period of intense debt placement. The position of incumbent Prime Minister Shinzo Abe looks solid in the first two days prior the official start of election campaign. It is expected that his Liberal Democratic Party in the bloc with Komeito will gain more than 300 seats out of 465. In the current situation, we are expecting the yen to decline to 111.60 and further to 111.00.