After the escalation of geopolitical conflicts in the Middle East and the confidence of investors in the extension of the OPEC agreement at the Vienna meeting on November 30, which caused oil prices their peak level in the last 2.5 years, the market was at a deadlock. Many "bullish" factors are already taken into account in the futures quotes, while the revived growth of the number of drilling rigs from Baker Hughes (+9 to 738 by the week-end results by November 10) strengthens the risks of increased activity of American producers. They managed to increase production to a record 9.62 million b/d ( a 14% increase from mid-2016), even as the drilling process slows down and prices are lower than current ones. Confident consolidation of the Brent above $60 per barrel unleashes companies from the US hands, which in turn lays the foundation for the development of correction.

According to the International Energy Agency, shale production in the U.S. by 2025 will generate up to 80% of the increase in the global indicator. States who are the largest importer of oil will turn into an exporter, radically changing the situation of the entire market. Will OPEC be able to cope up with this? Given this, a regular extension of the Vienna agreement is necessary, which so far is working, although not without issues. If the cartel cut production in October to 32.59 million b/d (-0.46% m/m), then Russia for 10 months of 2017 produced 2% more than in the same period last year. Moscow was most vocal about the need to extend the validity of the Vienna agreement, however, it does not fulfill its obligations!

At the same time, Saudi Arabia notes that in less than one year global oil reserves have decreased by 180 million barrels and currently exceed their five-year averages by 154 million barrels. Riyadh calls 2018 the year of the restoration of the oil market, but it seems that it is the only country working on it, while all the others use the price increase for their own interests. OPEC predicts that in 2017 and in 2018 global demand will increase by 1.53 million and by 1.51 million b/p, which will help to balance the market. However, it is necessary to understand that there is also an offer.

In my opinion, the lack of new drivers reinforces the risks of Brent pulling back from current levels. Especially since the net position on the North Sea grade at ICE Futures Europe has once again notched a record high. By the results of the week by November 7, they exceeded 543, 000 contracts, marking an increase of 2.4%.

Dynamics of Brent and speculative positions

Source: Bloomberg.

Fitch Ratings argues that the price increase above $ 60 per barrel can not be sustained. In 2018, the value of oil will be the same as in the current year. While the average price of Brent in 2017 is $54.5 per barrel.

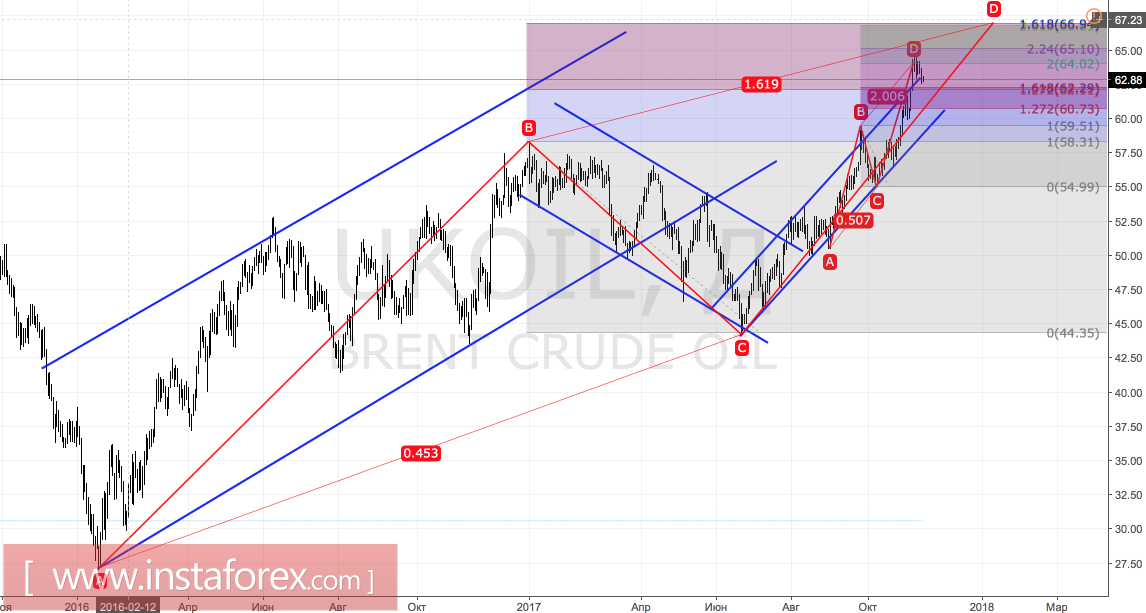

Technically, the North Sea grade rollback after reaching the target by 200% on the child pattern AB = CD looks natural. To continue the rally in the direction of $ 66.95 (161.8% for the maternal pattern AB = CD), the November high needs to be updated. The nearest support levels are located near the $62.3 and $60.75 marks.

Brent, daily chart