EUR / USD, GBP / USD

On Monday, the euro and the pound began with a downturn. This first move was in response to the draft adoption of the US tax reform by the Congress. The second move was against the general trend for the pound, when Michel Barnier and Theresa May reported on the progress in the Brexit negotiations. The concern in question was the Irish border. Now, Theresa May agrees that the Republic of Ireland and Northern Ireland should continue the duty-free trade regime. However, in the evening, the head of the European Commission, Jean-Claude Juncker, said that it was impossible to come to an agreement this week. The pound turned down. The total pressure on the euro, the US tax reform (from the filing of France) since. European companies operating under the US may be subject to additional taxation. European economic indicators came out weak. The index of investor confidence in the eurozone Sentix for the current month fell from 34.0 to 31.1.

The world flow of capital, as it seems to us, has a stable direction in the USA. Over the past month, the Treasury has attracted a debt of 78 billion dollars, increasing the national debt to 20.531 trillion dollars. The plan for the first quarter involves raising $ 512 billion, which is more than in the days of open QE. As we said earlier, the US did not stop in pursuing a soft policy, even against a background of higher rates, conducting a short-term debt to a long-term one. Now, the process becomes more open.

The best way to attract investors is to strengthen the national currency. Today, for American investors, this is an opportunity. Retail sales in the eurozone for October are expected to decline by 0.6%. The final estimate of Services PMI for November is expected to be unchanged at 56.2 points. The final estimate of the eurozone's GDP for the third quarter is also projected without a change at 0.6% (2.5% y / y). In the UK, Services PMI is expected to fall from 55.6 to 55.2. At 12:30 Moscow time, the minutes from the last meeting of the Bank of England will be issued. We do not expect to see any features in them.

In the US, the final evaluation of Services PMI in November could be increased to 55.4 from 54.7 while ISM Non-Manufacturing PMI is expected to decrease to 59.2 from 60.1. The US trade balance for October is projected at -46.2 billion dollars, the worst indicator for October since 2008. This represents the largest negative macroeconomic factor for the dollar today.

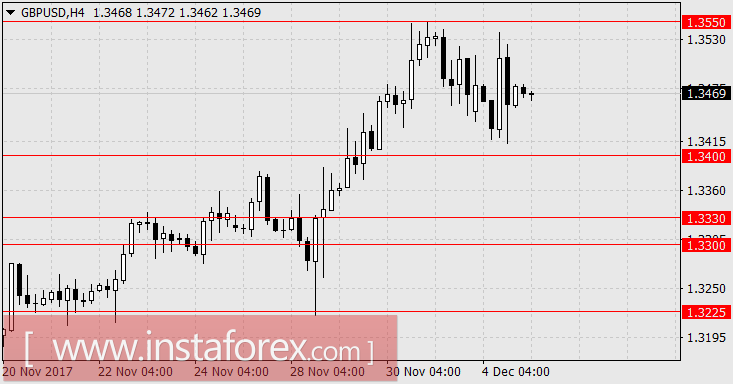

Based on the forecasted data, a situation that can not be strengthened. Investors can prepare for further developments this week. The main event will be data on employment in the US. We are waiting for the consolidation of the euro in the range of 1.1875-1.1930 and for the pound, we expect a decline in the range of 1.3300 / 30, as the next stage of the talks on Brexit. the middle of the month.

USD / JPY

In the last five sessions, the Japanese yen is moving exactly the same as the US stock indices. Yesterday, the Japanese consumer confidence index for November showed an increase from 44.5 to 44.9 with the expectation of growth to 44.8. Today, Caixin reported an increase in Chinese PMI services to 51.9 from 51.2 in October. The subsequent Japanese indicators will be released on Friday. On that day, Japan's GDP is expected to be revised for the third quarter in the final estimate to 0.4% from 0.3% with an increase in capital expenditure by 0.5% for the quarter. Meanwhile, the the balance of payments is expected to grow from 1.84 trillion yen to 1.93 trillion. Thus, the main risk of a fall in the USD / JPY pair is the behavior of the stock market. Here, the main concern of investors may be an increase in the corporate income tax to 22% from 20% as promised by Trump. However, the discussion on this issue will continue until the 20th of December. In the meantime, the market can grow on positive US statistics.

We are waiting for the yen in the range of 113.20 / 80.