The US consumer inflation declined by 0.1% for the month of March. This is the first time that the data dropped since May 2017 against the backdrop of falling gasoline prices. At the same time, core inflation (Core CPI) increased by 0.2% with a year-on-year growth of 2.1%. The report as a whole should be recognized as positive, since the Fed is primarily focused on Core CPI in developing solutions for the rate.

The publication of data on inflation did not have a noticeable effect on the mood of the markets, which are completely absorbed in the worsening geopolitical situation.

Politics, as you know, is a concentrated expression of the economy. The Trump administration, despite its seeming randomness, has consistently taken steps that can fill the budget and reduce the dependence of the government on borrowing.

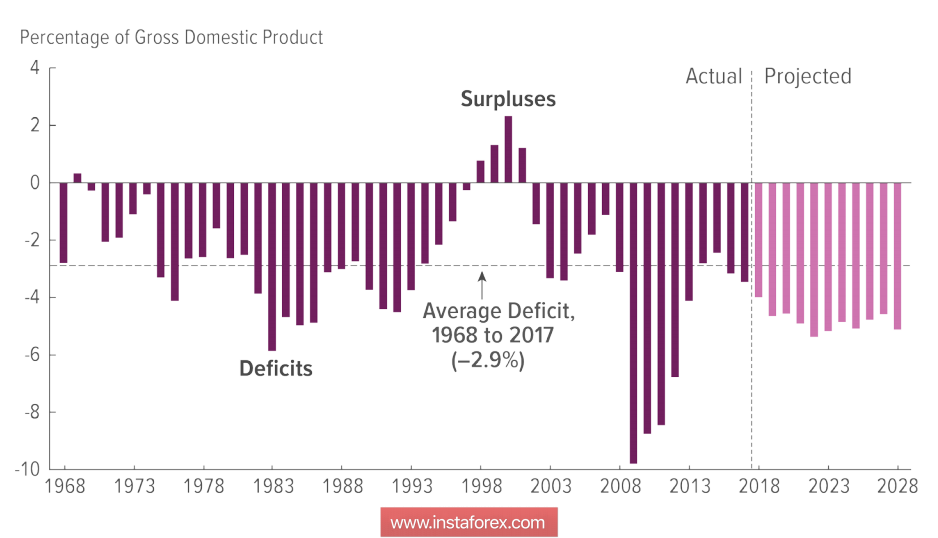

Forecasts, however, are still far from optimistic. On Wednesday, the head of the Congressional Budget Office (CBO), Keith Hull, presented an updated forecast for the next 10 years, taking into account, among other things, the effect of the tax reform that has already begun. According to calculations, the budget deficit in 2018 will be at 804 billion, and this estimate is 43% higher than the previous one. And by 2020, the deficit will already exceed $ 1 trillion.

Thus, the SVO does not see any prospects for the tax reform, as it does not expect the growth of budget filling. Moreover, the economy will begin to decline. In 2010, the NWS expected GDP growth at 1.8%, which is below the world average.

To finance the deficit, the US authorities will be forced to increase the level of public debt, which will reach its highest level since 1946 and exceed 100% of GDP. This means that the growth rate of public debt will exceed the growth rate of the economy for the entire decade. Against the backdrop of an increase in the Fed's rate and growth in government bond yields, interest payments on public debt will grow from the current 1.6% of GDP to 3.1% of GDP, and will become the main expense of the government after spending on defense.

Thus, the forecast of the NWO directly contradicts the estimates of the consequences of the reforms of the presidential administration. The next elections to the US Congress will be held in the fall and Trump will need to look for evidence of the effectiveness of reforms now.

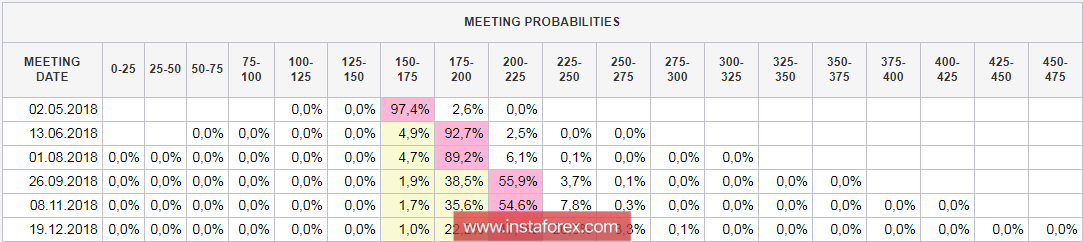

The minutes of the Fed meeting on March 20-21 were neutral, with a slight preponderance of the negative. Despite the fact that the protocol expresses confidence in the prospects for economic growth and the achievement of inflation rate of 2%, there was no unanimity among the members of the FOMC. Moreover, several members of the Committee expressed the opinion that the planned growth of the rate can be postponed until new information is received. Markets are confident that another increase will take place in June but the chances that there will be 4 in the current year have decreased, which led to a decrease in the dollar index after publication.

Some explanations for the end of the week from the FOMC members will follow on Thursday and Friday. The performances of Kashkari, Kaplan, and Bullard are expected then. However, the overall score is unlikely to change.

The trade war between the US and China has temporarily receded into the background but there is no reason to expect that it will end without starting. Trump is forced to follow the path of protectionism, since there is no other way to save the budget and to achieve at least some preferences for American companies. At the same time, China appears to be full of determination, which has never been seen in its history. The head of the International Monetary Fund (IMF) Christine Lagarde said on Wednesday that protectionism will lead to irreparable consequences for world trade and will contribute to a slowdown in the world economy. However, it is unlikely that it will help correct trade deficits. These prospects are of a long-term nature and will contribute to the growth of demand for protective assets.

The dollar will be under a slight pressure and will probably decline against the yen and the euro, as well as gold which may grow. No significant macroeconomic publications are expected until the end of the week. Volatility will be determined by geopolitical factors and the rhetoric of officials.