Oil reacted quite calmly to OPEC's decision to reduce production by 1 million bpd and to the deterioration of the global appetite for risk due to the escalation of the US-China trade conflict. The fall of the world stock indices led by Shanghai Composite, which lost about 20% of its annual highs, increases the risks of slowing global GDP and reduction of aggregate demand for oil. At the same time, the decline in production from the cartel has largely been recouped, problem countries continue to experience difficulties, which directly affects supply.

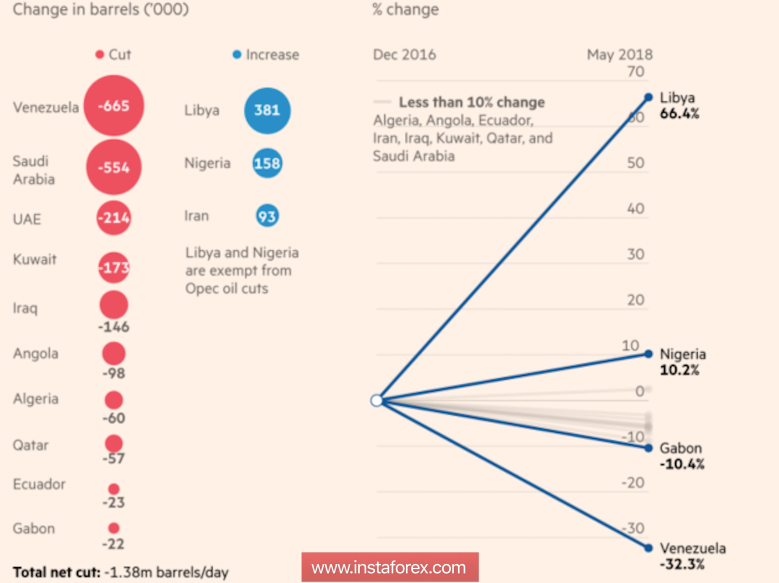

At the end of 2016, OPEC and 10 other producing countries, including Russia, agreed to reduce production by 1.8 million bpd in order to change the current "bearish" oil market conditions. A year and a half later, we are concerned about the risks of Brent growth in the direction of $100 per barrel, Riyadh and Moscow are changing the terms of the agreement. Iran expresses its disagreement, sarcastically noting that the June decision of the cartel is equivalent to the implementation of the orders of Donald Trump, who previously accused OPEC of artificially inflating prices. However, Tehran's position is clear. Due to economic sanctions, its production may be reduced by another third by the end of 2018, but in fact a holy place is never empty. It will be occupied by others.

The calm reaction of oil to the decisions of the summit on June 22-23 can be explained by the absence of a serious cut. Due to Venezuela's political and economic crisis, sanctions against Iran, and military clashes in Libya, the cartel has already exceeded its 2016 commitments by 150%. It pumped 1.3-1.4 million bpd less than the Vienna agreement. This allowed Russia to produce more. In this regard, the current negative of 1 million bpd looks like a necessity. What next?

Performing OPEC commitments

According to Standard Chartered, the volume of production before the end of the year may decrease by 1.5-2.3 million bpd due to Venezuela (-500 thousand bpd) and Iran (-1 million bpd). Yes, there is the US factor, however, despite the increase in shale oil production to a new record high of 10.9 million bpd, infrastructure problems make the potential for its increase limited. The company expects the continuation of the decline in global reserves and the growth of prices for oil by another $10-15 per barrel. In my opinion, the forecast is quite realistic, but consolidation in the range of $70-80 per barrel looks more likely. Most likely, the pressure on prices will continue to be exerted by the factor of trade wars and the related deterioration of the prospects of the world economy and global demand for oil.

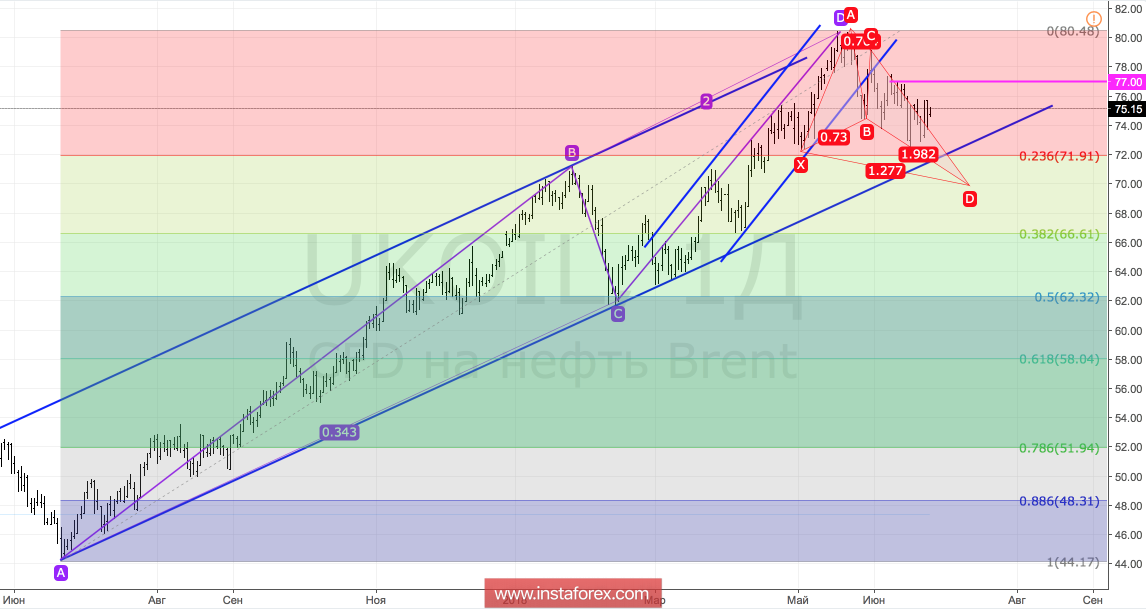

Technically, the realization of the "Bump and Run Reversal" pattern continues. Brent quotes at arm's length approached the trend line of the introductory stage, the confident breakthrough of which will increase the risks of the correction in the direction of $66.6 per barrel. However, to begin with, "bears "will have to pass the convergence zone near $69.75 (target 127.2% on the "Bat" pattern ). The pullback from the lower limit of the upward trading channel will create conditions for the development of medium-term consolidation in the range of $70-80 per barrel.

Brent, daily chart