The oil market does not know who to believe. Either the International Energy Agency, which predicts that supply growth from non-OPEC countries will accelerate from 1.8 million bpd in 2019 to 2.3 million bpd in 2020, mainly due to the United States, Brazil, Norway and Guyana. Or a cartel that lowered estimates of an increase in the indicator next year by 34 thousand bpd to 2.17 million bpd. The main reason, according to OPEC Secretary General Mohammed Barkindo, needs to be sought in the United States. There, the growth in supply in 2020 will be reduced by 33 thousand bpd to 1.5 million bpd. Much will depend on the dynamics of US production, because the question of prolonging the Vienna agreement to reduce production by the cartel and Russia at the meeting on December 5-6 was practically resolved.

According to a study by the US Energy Information Administration, US oil production will hit a record high of 13 million bpd in November and will continue to grow faster than previously expected in 2020-2021. Shale production will increase to 9.13 million bpd in December. As a result, the share of American manufacturers in the global indicator will increase, while the share of OPEC and Russia, on the contrary, will decrease from 55% in the mid-2000s to 47% in 2030. The EIA version is more similar to the opinion of the IEA than to the position of OPEC. One can only guess what goals the cartel pursues, spreading information about the slowdown in the pace of US production of black gold?

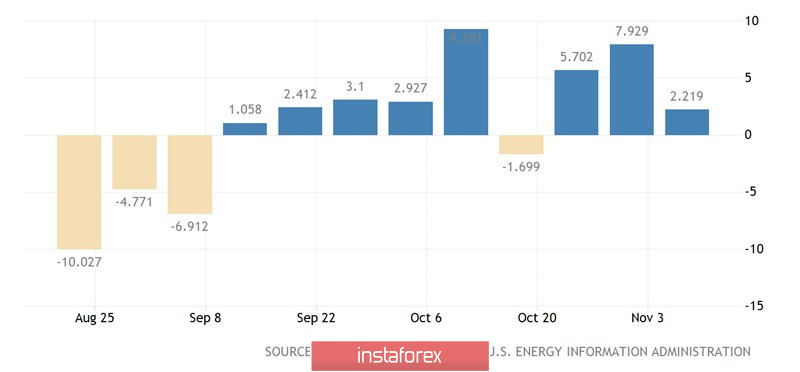

Official statistics does not provide an answer to the question "Who is right?". Oil stocks in the United States increased over eight of the last nine weeks, which indicates either excessive production, or a slowdown in demand. The first version, given the strength of the US economy, looks more believable than the second. On the other hand, the number of drilling rigs from Baker Hughes is steadily decreasing, indicating a reduction in business investment and potentially leading to a slowdown in production.

The dynamics of US oil reserves

The dynamics of Brent and the number of drilling rigs in the US

Along with questions about the growth rate of production in OPEC + and outside the cartel, there are other uncertainties in the oil market. In particular, investors are still not sure whether Washington and Beijing will be able to sign a trade agreement. Both sides are unhappy with the unwillingness of opponents to make concessions. China wants a rollback of tariffs, Donald Trump, on the contrary, threatens to increase them in case Beijing does not sign the agreement. At the same time, the Minister of Commerce Wilbur Ross assures that it will be endorsed by the presidents of the two countries. The United States will renew the license for American companies working with Huawei, and Beijing will remove duties on deliveries from the USA to the Chinese market of meat and poultry.

Technically, the struggle for Pivot levels of $62.05-62.45 per barrel continues on the Brent daily chart. The victory of the bulls will allow them to continue the rally in the direction of the Shark and Wolfe Wave patterns. On the contrary, if the important area remains under the control of the bears, the risks will peak to $59.25 and $56.4.