A sharp aggravation of US relations not only with China, but also with Europe, contributes to an increase in the demand for protective assets and sales in the stock markets. The S & P500 lost 0.66% on Tuesday and the Nikkei lost more than 1% on Wednesday morning. At the same time, all Asian indices are traded in the red zone without exception. Sales are caused by the threat of expanding the geography of the US tariff war to France and Germany, while China sharply tightened its position after frankly brutal pressure, and the chances of concluding at least some package before the end of this year have decreased.

NZD/USD

Kiwi is growing rapidly in early December, almost reaching the upper boundary of the medium-term channel 0.6540/50, and there are quite rational reasons for this - one of which is a number of indicators of the state of the New Zealand economy show steady growth.

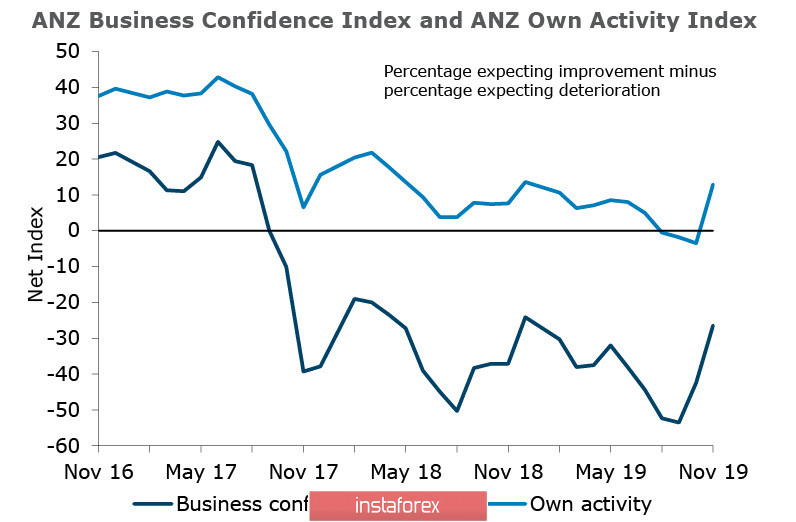

Moreover, the business optimism index of the RBNZ rose to -26.4p, which is the best result for 11 months. The forecast of activity from ANZ is the highest this year and consumer confidence and commodity price indices have also grown, which gives hope for inflation.

On the other hand, banks that are active in New Zealand tend to regard this surge in activity as a result of a 0.75% decline in the rate of RBNZ. A lower rate contributes to an increased demand for housing as well as an increase in mortgage loans. The situation in the economy of New Zealand looks more optimistic than in the whole world; optimism is also supported by the growth of the US treasures profit spread, which is regarded by the markets as a reduction in the threat of a global recession.

The NZD trade-weighted rate is still near 10-year lows, which gives serious support to exports, while dairy prices are stable.

On Thursday, a key event of the month will take place - the decision of the RBNZ on the amount of bank capital. Increased requirements for bank capital will put increasing pressure on lending rates and limiting the availability of loans, but opinions on the consequences of such tightening are diametrically opposed. The market, in turn, has not developed a consensus on what to expect from the RBNZ since any soft decision will support the growth of kiwi, and at the moment, this is the most likely development of events.

The growth of NZD/USD to the resistance zone of 0.6580 / 6600 in the coming days looks reasonable, support is 0.6477/85, and the kiwi still looks stronger than most commodity currencies.

AUD/USD

According to the results of the meeting that ended on Tuesday, the RBA left the interest rate unchanged at 0.75%, as predicted. The RBA's accompanying statement looks quite optimistic and there is a decline in global risks and emphasis is placed on the fact that the Australian economy has "reached a tipping point" and has good chances to increase growth rates again.

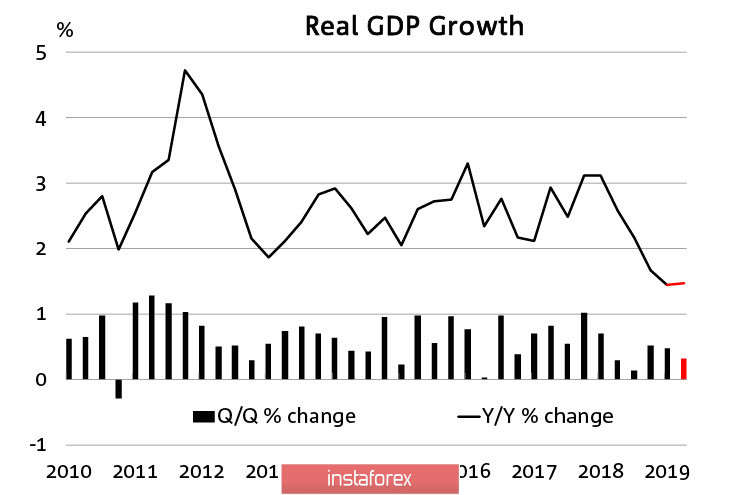

At the same time, RBA expects that the growth of GDP will accelerate to 3% in 2021, unemployment will decline below 5%, and inflation will be stable in the range of 2-3%. However, all three indicators look worse than forecasts at the moment - inflation in the 3rd quarter is at the level of 1.7%, and the forecast for the 4th quarter does not suggest changes. Meanwhile, the unemployment rate in October is 5.3%, but the graph of GDP growth rates speaks for itself.

Do we really see a change, as the RBA hopes? or can the decline continue? According to the RBA, there is actually not much optimism, since the USA and China which are the key trading partners of Australia, are moving away from signing a trade agreement rather than approaching it. Therefore, the risks to the Australian economy are not reduced.

More so, Australia's S & P / ASX 200 index is falling for the second day in a row, losing more than 1.5% on Wednesday morning, and thus, a rising panic will put pressure on the Aussie for some time to come. The RBA decision supported corrective growth, but it is highly likely that it will be used by the bears to take profits, after which the decline will resume. On the other hand, updating the maximum of 0.6861 is unlikely and the Aussi is likely to consolidate below 0.6825 / 30 and go into the sideways range with a tendency to resume decline.