Similar to the rally in US stock market indices, the rapid rise in oil prices from April lows, which continued through the end of summer, looked quite exaggerated. The market has clearly overestimated China's appetite for fuel and the unexpectedly high demand for gasoline in the United States despite the ongoing pandemic. Finally, everyone has counted on the OPEC+ production cuts. As soon as all the mentioned drivers lost their steam, Brent and WTI have entered the downward correction. Moreover, the rising US dollar supports the bearish trend on both the benchmarks.

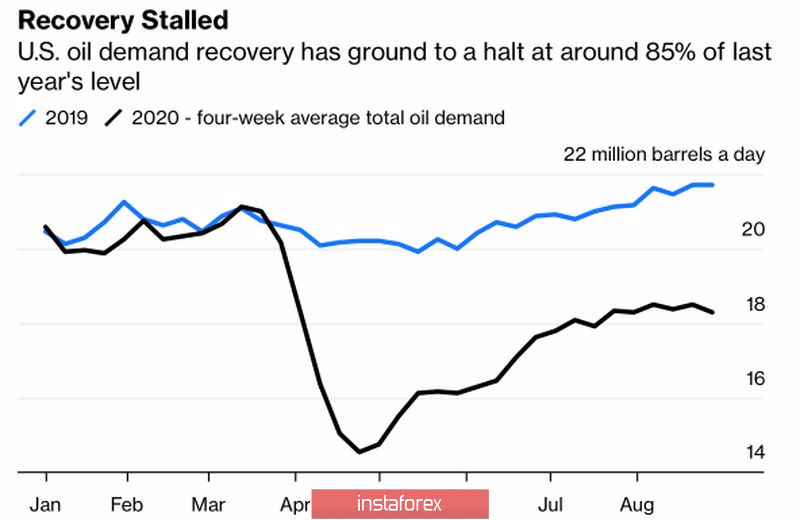

The US oil producers may not be able to return to their pre-crisis output levels. However, the demand for gasoline may offset this factor. This time, the driving season in the United States was less active due to the COVID-19 impact. Thus, before the recession, the oil refineries capacity in the Gulf Coast was 95% in the same period last year, while ahead of Hurricane Laura it dropped to 81%. According to Commerzbank estimates, the demand for gasoline in the US is 8-10% below the levels seen in August-September 2019. Most importantly, the US gasoline demand is unlikely to catch up with the last year's levels.

US oil demand dynamics

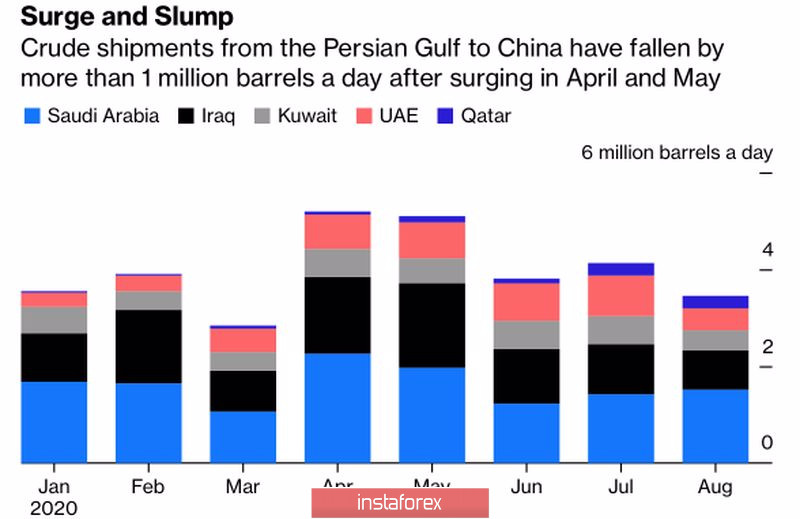

The Asian market provides little support to oil as well. India, one of the world's largest consumers of oil, ranks second in the list of countries most affected by the pandemic. Besides, China's appetite for crude is gradually decreasing. Low crude prices in April and May encouraged China to stock up on oil until it filled up all its tanks. Obviously, China's storage capacity has become limited. This may be the reason why Beijing had to reduce its oil imports from the Middle East by about 1 million barrels per day in summer compared to spring shipments.

China's oil imports from Middle East

The Brent's fall to $40 per barrel may not seem so surprising given several factors. First of all, the OPEC+ members decided to limit the output cuts the have agreed on earlier this year. Then, we shall not forget about the struggle between Saudi Arabia and Russia for the market share. In addition, the US dollar began to regain ground. In the meantime, Saudi Arabia is cutting its export prices, while Moscow intends to increase production as with the global demand recovers. The fears of the second wave of COVID-19 in Europe and an increase in the number of new cases in 22 out of 50 US states add more pessimism to the market.

However, I think that the situation in the energy market is less gloomy as it seems. The drop in the US dollar index came amid concerns about the dovish rhetoric of Christine Lagarde at the ECB September meeting. The US dollar is likely to remain in bear market in the long term. As China's GDP recovers, the demand for black gold in this country will increase. What is more, the coronavirus death rate is low, which is good news for global fuel demand. The plunge in oil prices is closely associated with the correction of US stock indices. As soon as the stock market rebounds, Brent and WTI will again see a bullish trend. I think that the pullback for both grades is limited. So, I suggest buying Brent on a breakout of resistance at $41.5 and $42.2 per barrel.

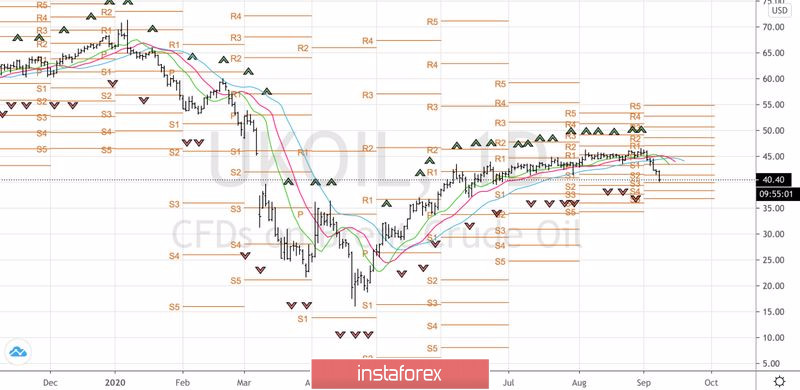

Brent daily chart