US stocks closed in the "red zone" yesterday just before the negotiations between Nancy Pelosi and Steven Mnuchin resumed, whose goal is to overcome differences between Republicans and Democrats about financial support. However, investors believe that it will not be possible to agree on a stimulus package before the US elections on November 3, since there is no positive news regarding the negotiations.

As a result, most of the stock indices of the Asia-Pacific countries are also sold out. This is followed by the opening of Europe, which is expected in the "red zone" too. Moreover, rising tensions will increase the pressure on commodity currencies, so the dollar has every chance to start strengthening after yesterday's weakening again. The market optimism which was received last Friday after the US retail sales report in September are already used up.

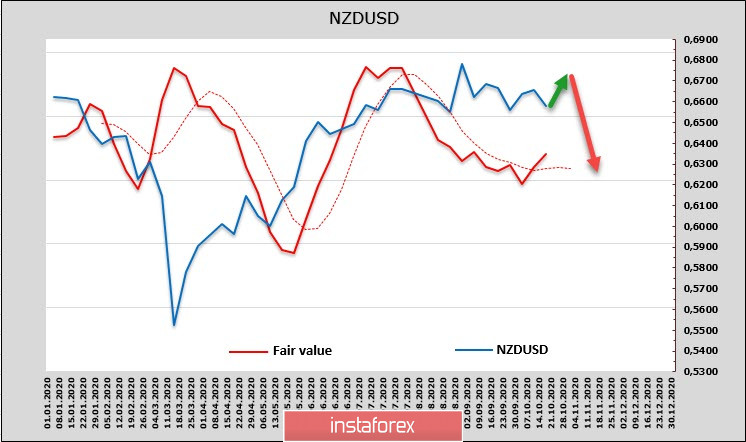

NZD/USD

Recent macroeconomic data provide a slightly more positive view of both the prospects for the recovery of the New Zealand economy and the fate of the NZD. The housing market is recovering significantly faster than expected, indicating stronger consumer demand. At the same time, forecasts for GDP, labor market, and inflation are revised upward.

The service sector activity index exceeded the 50p level in September, while the manufacturing sector climbed from 50.7p to 54p. As a result, the quarterly NZIER survey shows the growth of business confidence in the 3rd quarter.

The turning point in firms' moods about business expansion, headcount and investment is noteworthy. For example, this turning point has not yet occurred in the US, despite the partial economic recovery after failing in the second quarter.

These positive changes add confidence, but they are not yet enough to change the overall trend. The pace of economic recovery is forecast to slow down from January, and as promised earlier, the RBNZ will cut its key rate by 0.5% at its April meeting. The only thing that has clearly changed is the assessment of risks – they are now considered balanced, and failure in the economy is unlikely.

Over the reporting week, net long position in NZD slightly increased, but the trend remains neutral. A decline in the estimated fair price in August-September led to a halt in the growth of NZD/USD, but the kiwi went into a sideways range on the spot. Today, there are chances to grow again.

The formation of a local bottom at the lower limit of the range of 0.6480/6510 and a return to the upper limit of the channel 0.6760/80 is the most likely scenario, as there are not enough bases to get out of the range. Despite temporary positivity, investors expect that the RBNZ will significantly weaken the NZD with the planned measures to reduce the rate and expand QE, so the growth is highly likely to be used for profit-taking and entering long-term short positions.

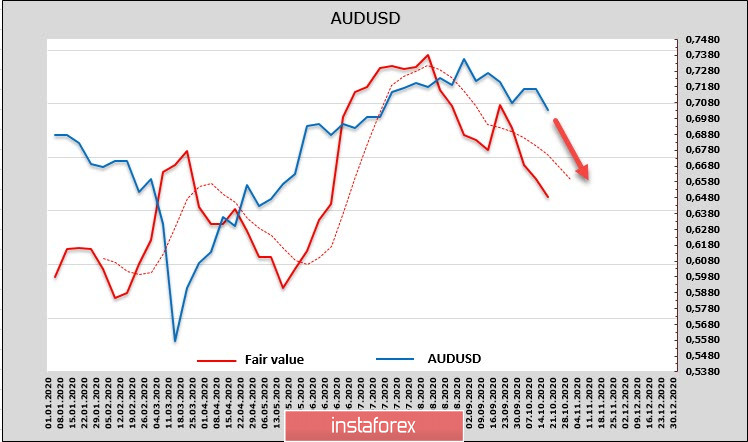

AUD/USD

The net long position was reduced by 494 million to 276 million over the reporting week, that is, virtually to zero. There is no trend in futures, considering the dynamics of the stock and debt market in Australia. Moreover, there is a prolonged downward trend.

Last Friday, RBA's head, Mr. Lowe hinted that the Central Bank will most likely consider the issue of further expanding stimulus measures on November 3. In particular, he allowed to lower the current rate of 0.25% to 0.10%, as well as the possibility of direct quantitative easing within 5-10 years.

Technically, the Australian dollar looks weak this morning, which is mainly due to the prospect of easing the RBA policy. After it rebounded from the border of the 0.7245 channel, it is very likely to decline to the support level of 0.7005 and further to the lower border of the 0.6850/70 channel.