Some said that the main result of the November FOMC meeting was the start of the QE program tapering. Others thought Jerome Powell hinted at a federal funds rate hike in 2022. I paid attention to the Fed's silence on what is happening in the financial markets. Given how the ECB and the Reserve Bank of Australia and a little later the Bank of England reacted earlier, we can assume that the Fed is generally satisfied with the signals given by investors, which is good news for the US dollar.

If the European Central Bank or the RBA are not happy with market projections for a rate hike in 2022, they usually announce this. The Fed has been stubbornly silent on the behavior of CME futures, which signal a 70-75% chance of two acts of monetary restraint next year and a 35-40% chance of three. I suppose that the Fed is not ruling out that possibility either. The return of the economy to full employment in the middle of next year and the inflation remaining at high levels may force the Fed to tighten its monetary policy.

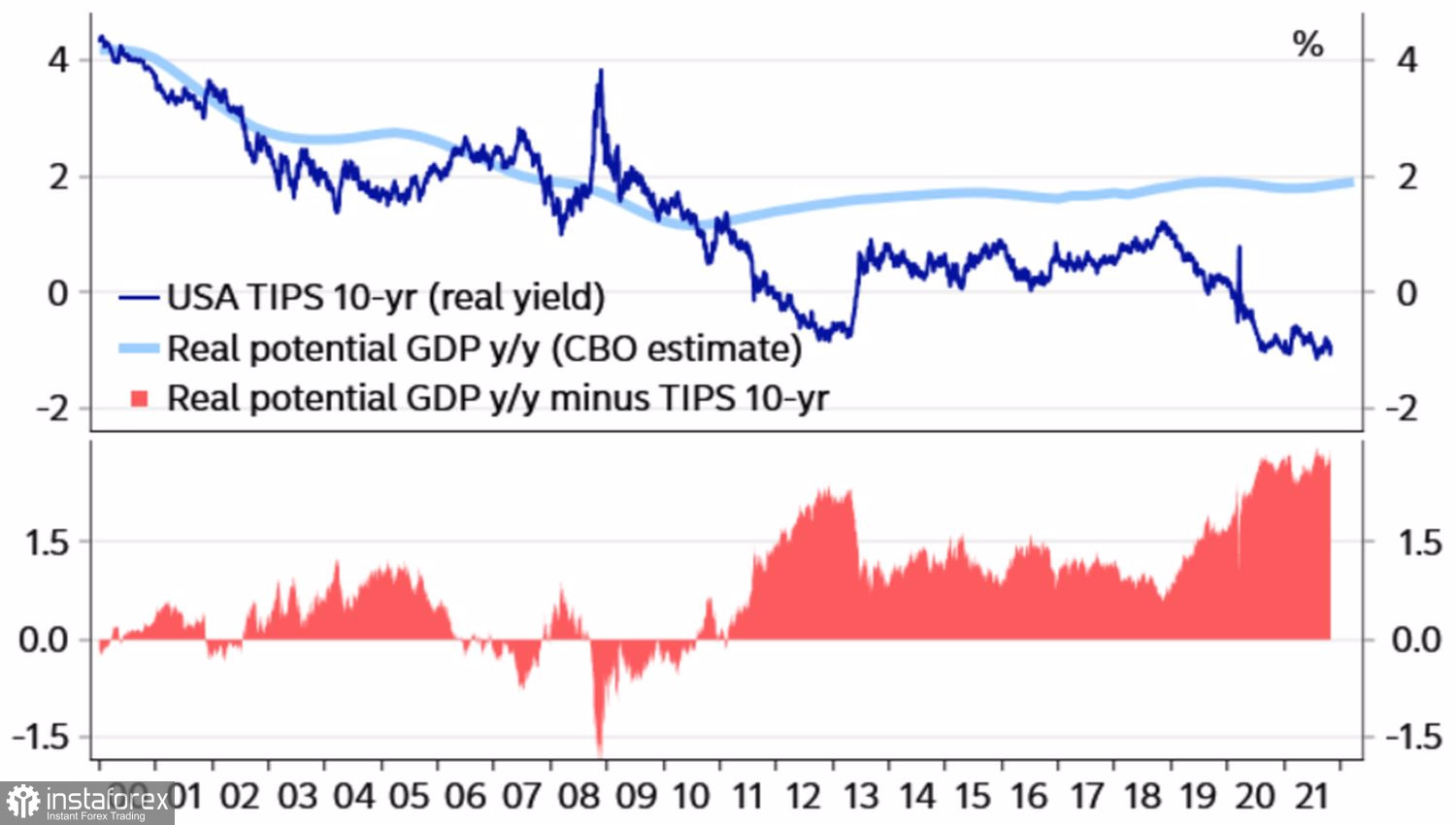

Based on the trend of real potential GDP, rates in the United States are currently extremely low and they have room to grow.

TIPS yield and real GDP chart

The acceleration of the US inflation is supported by rising wages, used car prices and rising rents. The airfares and tourist services sectors are likely to improve as the pandemic in the US eases. The same factor may contribute to a sharper job market recovery than expected, as well as accelerated GDP growth in the fourth quarter. The US economic indicators will outperform their European counterparts over the next few months, including the rise in COVID-19 cases and the energy crisis in Europe. All above is a sure sign that the EUR/USD pair may continue its downtrend.

The dynamics of forex rates are determined by the monetary policy of central banks, which affects the value of assets. In this regard, the differential of interest rate swap spreads signals that the downside potential of the major currency pair is not exhausted. It is not big news, as the Fed is likely to raise rates three times in 2022 and the ECB is not going to do so until at least 2023. According to Christine Lagarde, three conditions are required for monetary tightening, and they will not be met next year.

EUR/USD and real swap spread chart

Data on the US inflation for October will be released on November 12. According to Bloomberg experts, consumer prices will accelerate to 5.5% and core inflation to 4.1%. However, the rates may hike higher in 2022.

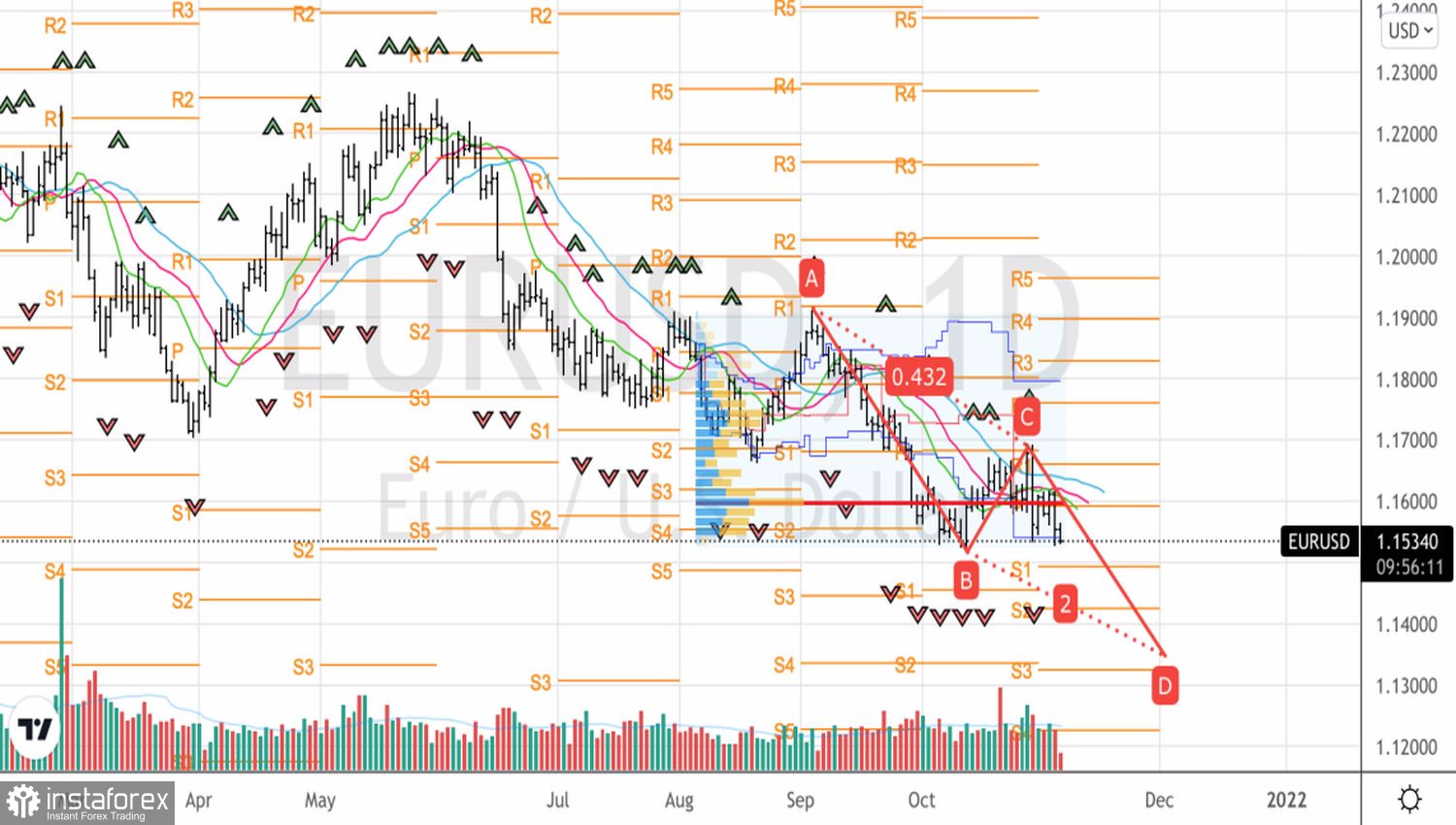

Technically, there is no reason to doubt the strength of the downtrend. A retest of 16-month lows may form the AB=CD pattern, the target of which at 200% corresponds to the level of 1.135. It is better to hold short positions on EUR/USD from the level of 1.1595 and increase their volume on pullbacks.

EUR/USD daily chart