This week will be filled with a large number of important events and publications of economic data that are likely to have a noticeable and long-term impact on the currency markets.

First, the meetings of the world's largest central banks should be noted – the Fed, the ECB, the Central Bank of Japan, and the Bank of England on monetary policy. But with all the importance of the decisions of all these banks, the results of the meeting of the US regulator will still play a leading role, behind which all the world's central banks have traditionally lined up in the last decade in the sense that they always check their monetary policy with the Federal Reserve.

If there is still some uncertainty about how the monetary rate may change in relation to the Bank of England, the ECB, and the Central Bank of Japan, then radical changes are expected from the Fed. Back in October, it was suggested that increased inflationary pressure in America could force the local Central Bank to accelerate the process of reducing stimulus measures, the meaning of which was to purchase government bonds and secured corporate mortgage securities, as well as to make the first increase in interest rates in the first quarter of 2022. Our expectations were confirmed in the forecast of a member of the Fed and the head of the Federal Bank of St. Louis, J. Bullard, who has voting rights on the Open Market Committee (FOMC).

Now, after a number of rather harsh statements, J. Powell said that investors had expectations that the initial reduction in asset repurchase by $ 15 billion per month could be increased to $30 billion by the decision on the outcome of the meeting on December 14-15. In addition, it should be considered that a strong incentive to such a decision is the consumer inflation data in the States published on Friday, which showed increased pressure from inflation. It can be recalled that in November, the inflation rate increased from 6.2% to 6.8% in annual terms, and the decline was less than expected in monthly terms. The consumer price index rose by 0.8% against the forecast of 0.7% and the October value of 0.9%.

How can the markets react to the Fed's decision to increase the volume of asset repurchase reductions from $15 billion to $30 billion per month?

We believe that it seems that this probability has already been generally won back by the previous reaction in the markets. Investors will be interested in the Central Bank's plans and its forecasts on macro indicators for the next three years, which it traditionally presents at the end of the year, in December. If the forecasts of GDP, inflation, labor market, and interest rates show a promising general weakness of the YS economy, which is manifested in GDP and employment figures, and at the same time demonstrate the expectation of increased pressure from inflation and, as a result, a vigorous increase in interest rates, then we can expect a new wave of declining demand for risky assets and strengthening the dollar's position in the currency markets.

However, if the Fed continues to try to be optimistic about the prospects of the national economy, smooth out the negative effect of the decision to increase the volume of asset repurchase reduction, and shows hopes that inflation pressure may stop, this will be regarded by investors as positive news and may cause a Christmas rally in stock markets.

Assessing the market picture, we believe that the markets are currently more inclined to the second scenario.

Forecast for the day:

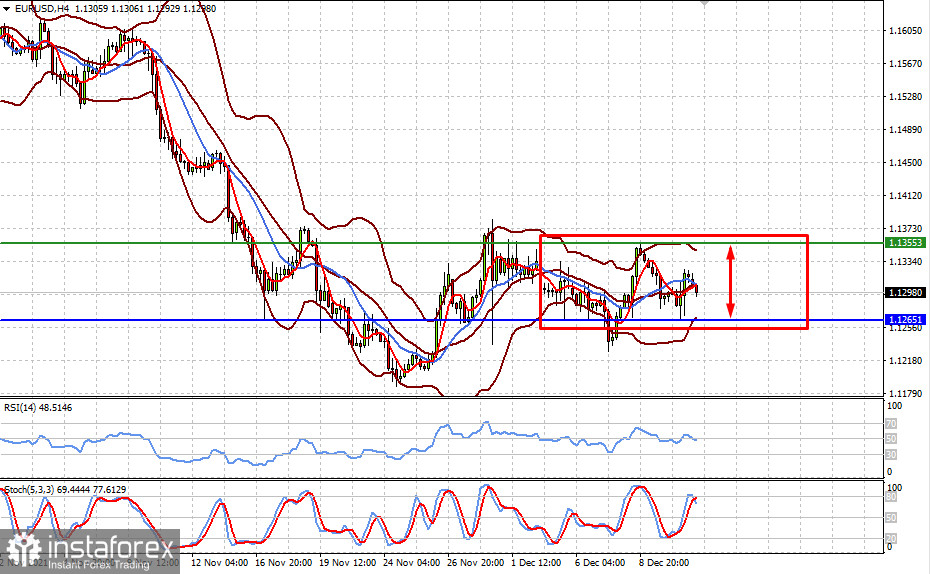

The EUR/USD pair is likely to consolidate in a narrow sideways range of 1.1265-1.1355 until the results of the Fed and ECB meeting.

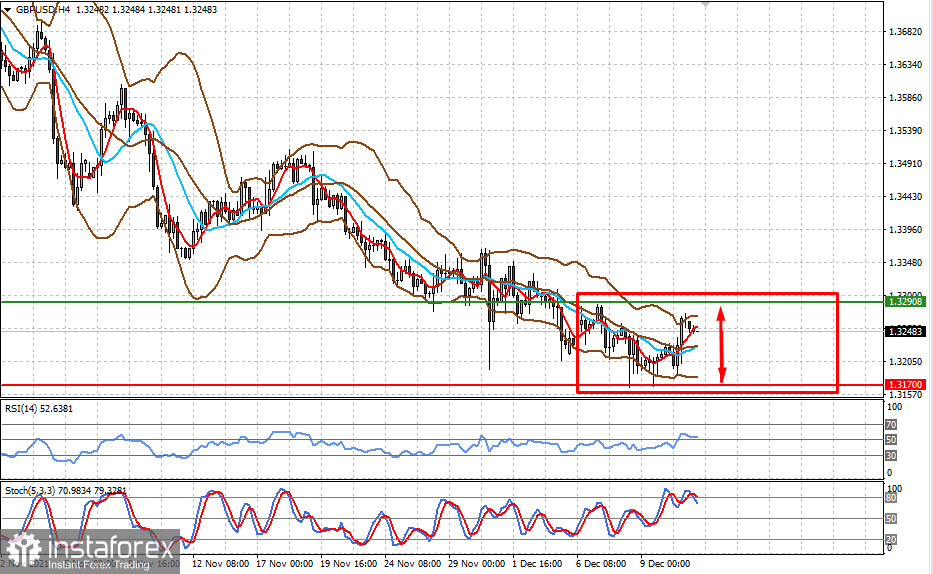

The GBP/USD pair is also likely to move in the range 1.3179-1.3290 before the Fed and Bank of England meetings.