The Santa Claus rally on the U.S. stock market, which allowed the S&P 500 to reach its 68th historical high in 2021, increased risk appetite and contributed to the worst weekly result of the U.S. dollar since September, should not deceive anyone. At the end of the year, investors close positions, fix profits. They got tired of monetary policy and turned their attention to stock indices. At the beginning of 2022, everything should return to normal.

It is obvious that Omicron, the Fed's intention to accelerate the normalization of monetary policy, as well as problems with the passage of a new $1.75 trillion fiscal stimulus package from Joe Biden will lead to a slowdown in U.S. GDP from 7% to 2-3% in the first quarter. It is unlikely that this will stop the Federal Reserve, which needs to fight the highest inflation in almost four decades. FOMC forecasts provide for 3 acts of monetary restriction in 2022, QE will become history in March.

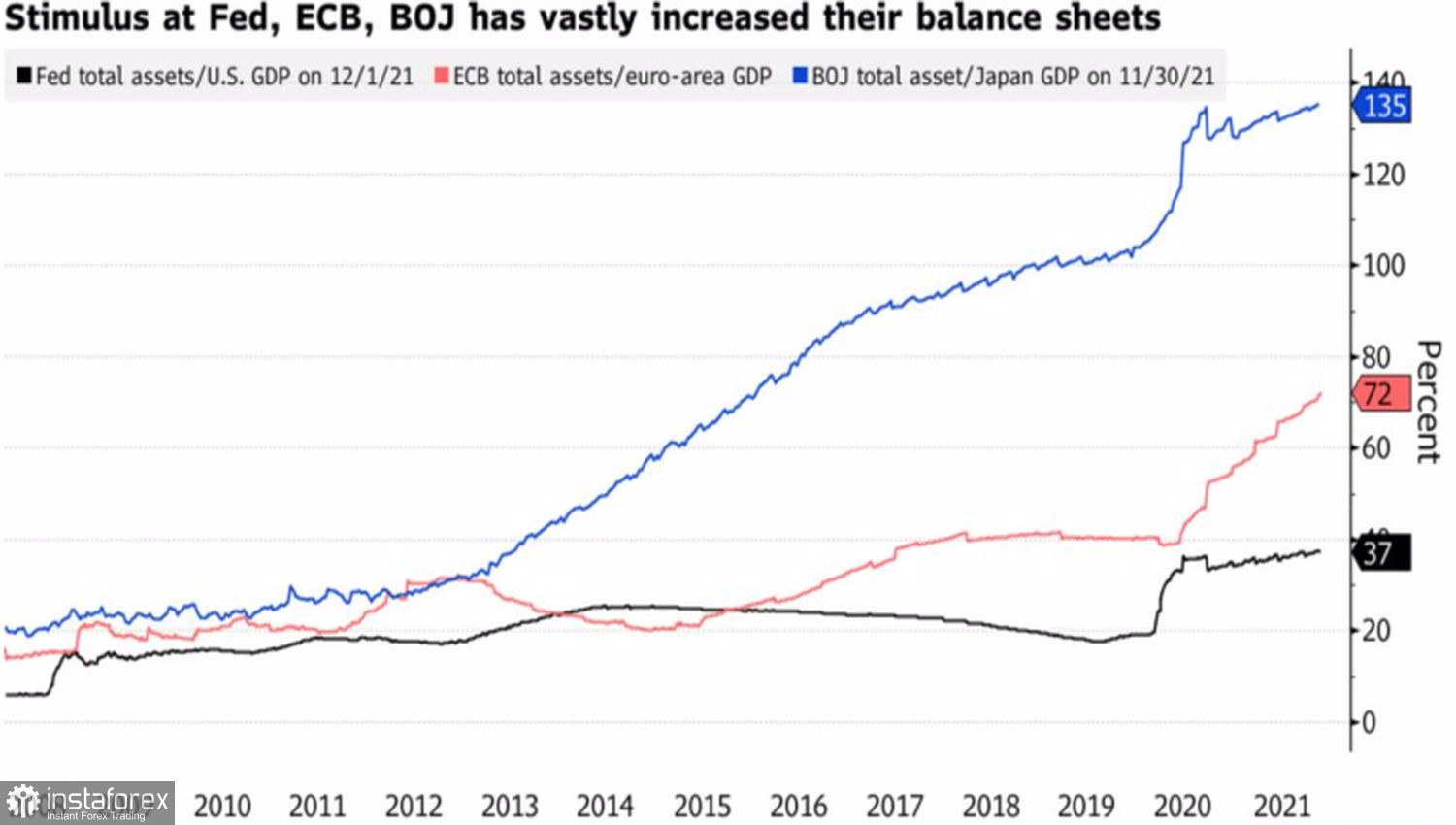

The eurozone economy is even weaker than the U.S., and the ECB is mired in deflationary thinking. They fear the repetition of when colossal monetary stimulus does not help the Central Bank of Japan to bring consumer prices back to the 2% target. Hence the reluctance to part with the quantitative easing program, and the firm belief that rates in 2022 will remain at the same levels. The faster growth of the balance of the European regulator in comparison with the U.S. unequivocally hints that the downtrend in EURUSD is likely to continue.

Central bank balance sheet dynamics

The U.S. dollar will also benefit from an earlier increase in the federal funds rate than is currently predicted by the derivatives market. The CME derivatives issued June as the most likely date for the first act of monetary restriction, but some FOMC hawks are ready to take action in March. If inflation in the U.S. accelerates to 7%, other representatives of the Central Bank will join their number.

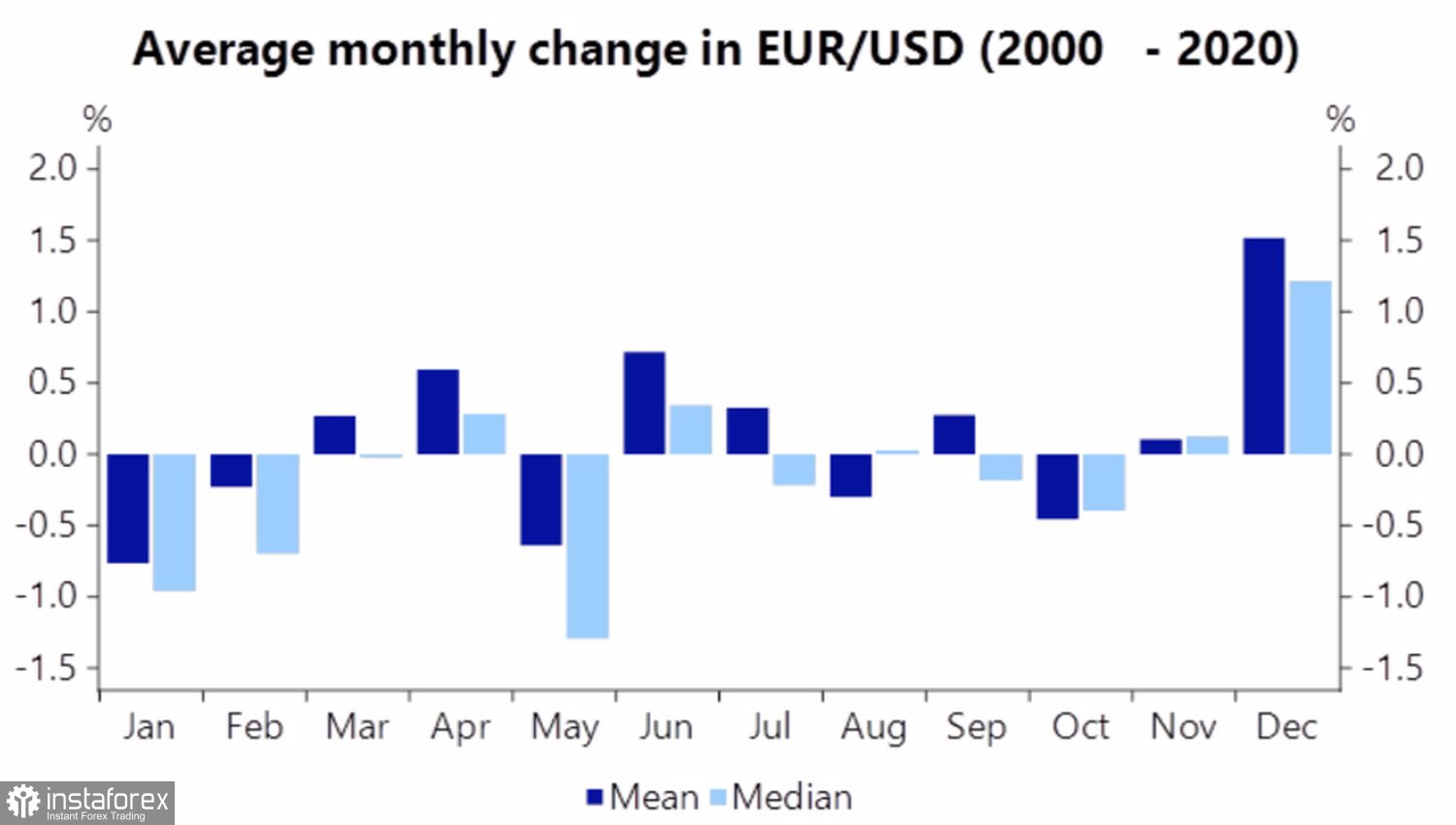

At the end of December, the EURUSD bulls were supported by a seasonal factor: the last month of the year, as a rule, is favorable for the euro and U.S. stock indices. In contrast, the S&P 500 falls more often than it rallies in January, and the U.S. dollar feels more than confident amid worsening global risk appetite.

EURUSD dynamics in different months of the year

The rally of U.S. stock indices is facilitated by the positive statistics for the United States, indicating that the economy is strong. However, if it is firmly on its feet, and inflation is significantly higher than the target, why not raise rates? If it is strong, why is there any fear that tightening monetary policy will significantly slow down GDP? I believe that at the beginning of 2022, investors will realize the absurdity of such concerns and will return to buying the U.S. dollar.

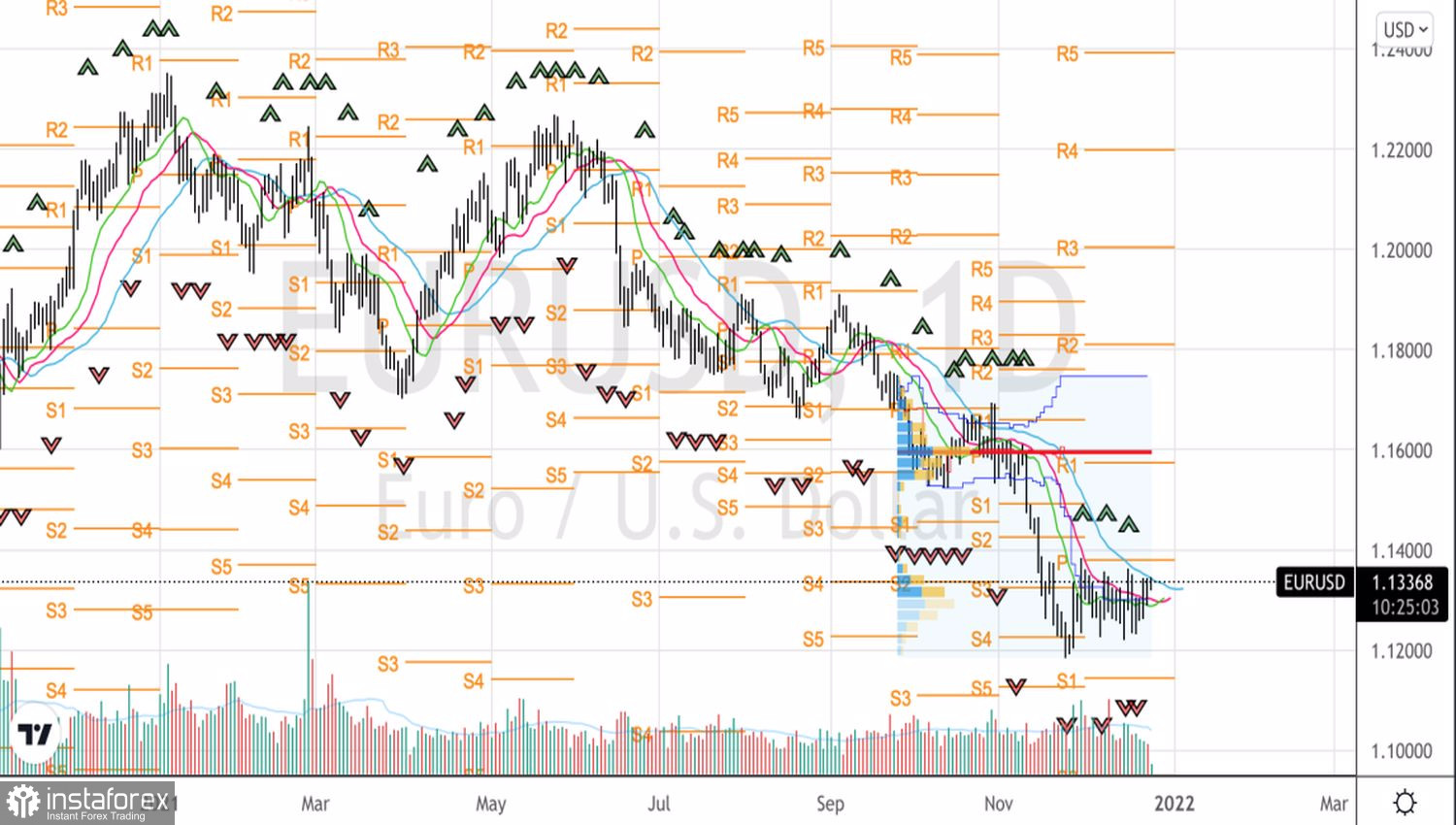

Technically, the formation of an inverted "Splash and Shelf" pattern on the daily timeframe of EURUSD indicates that traders have the opportunity to open positions both to buy on the breakout of the upper border of the consolidation range ("shelf") 1.1225–1.1355, and to sell in case of a successful storming of the support at 1.1225.

EURUSD, Daily chart