The US Fed's emergency meeting on Monday did not lead to any unexpected actions, which investors were slightly afraid of. The issues of the credit market state are considered and its prospects are reassessed in connection with the expected rate hike in March. The probability that the Fed will immediately raise the rate by 0.5% at the next meeting has fallen to 33%, which should somewhat calm the markets.

At the same time, Fed officials continue to verbally intervene. The president of the St. Louis Fed, James Bullard, repeated on CNBC his call for the Fed to raise the discount rate by 100 basis points by July. The head of the Kansas Fed, Esther George, also reiterated that the Fed should raise rates outside scheduled meetings and start selling bonds from its portfolio. These speeches support the overall hawkish background on the US dollar, although investors are not in a rush to buy it based on the CFTC report last week.

April gold futures are at a three-month high, while oil rose above $96 per barrel for the first time since 2014. All this indicates the weakness of the US dollar, which is currently supported largely by the rhetoric of Fed officials and the artificial escalation of geopolitical tensions.

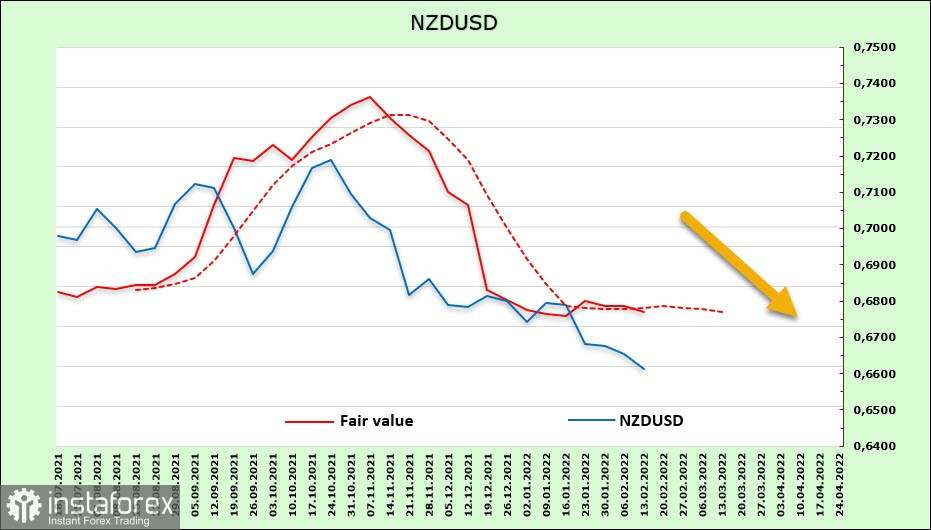

NZD/USD

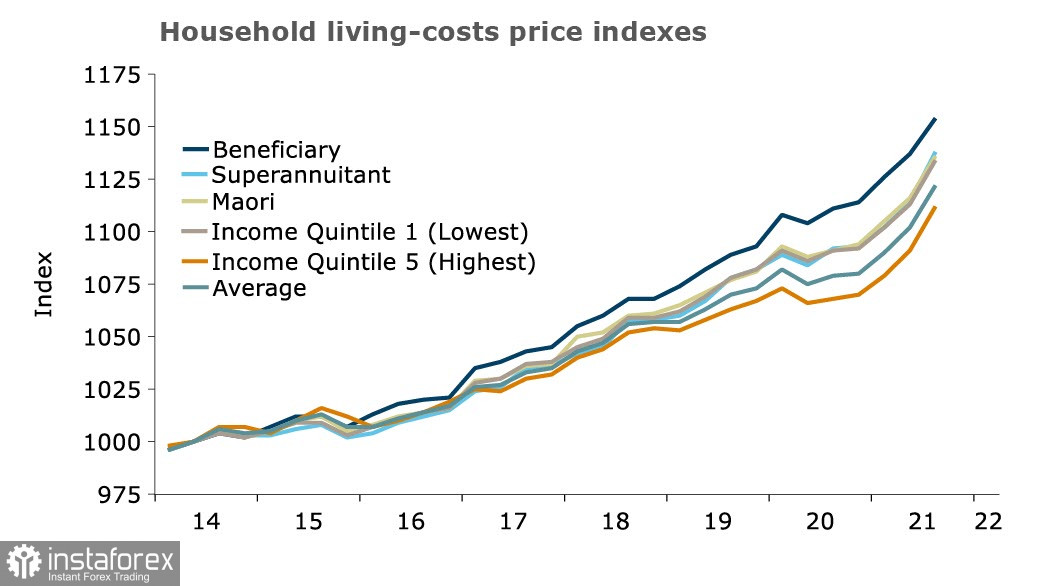

It became slightly clearer why the RBNZ is not in a hurry with rates, despite a record increase in inflation. It can be recalled that six months ago, it seemed that the RBNZ would be ahead of other central banks in terms of normalization rates. But this was not the case. This week, Stats NZ published data on the Household Price Index (HLPI) for the fourth quarter. These data are similar to the Consumer Price Index (CPI), but the HLPI provides detailed information on how the rising cost of living affects different households. Here, it shows that there has been a significant increase in the cost of living in all households in recent years.

The total cost of living in the 4th quarter rose by 5.2%, which is slightly lower than inflation (+5.9%), but it makes it clear that if the RBNZ starts raising the rate in an attempt to ease the growing inflationary pressure, heavily indebted households will experience significant cost-covering problems.

Data on food, rent, and housing prices will be released this week. If there is a steady increase, then the RBNZ will have no choice but to raise the rate, but if growth slows down, this will reduce market expectations for the rate. In any case, it can be assumed that there is no more outstripping growth in yields and the demand for New Zealand assets will remain low, which excludes a strong growth in demand for NZD.

The futures market is unchanged. The net short position in NZD fell by 87 million over the reporting week, reporting to -689 million. It shows that there are no purchases from investors as the estimated price does not increase.

As expected last week, the New Zealand dollar held above the local low of 0.6520 but found no reasons to rise either. An upwards pullback is possible. The nearest resistance is 0.6810/20, but it is more likely to continue trading in the range.

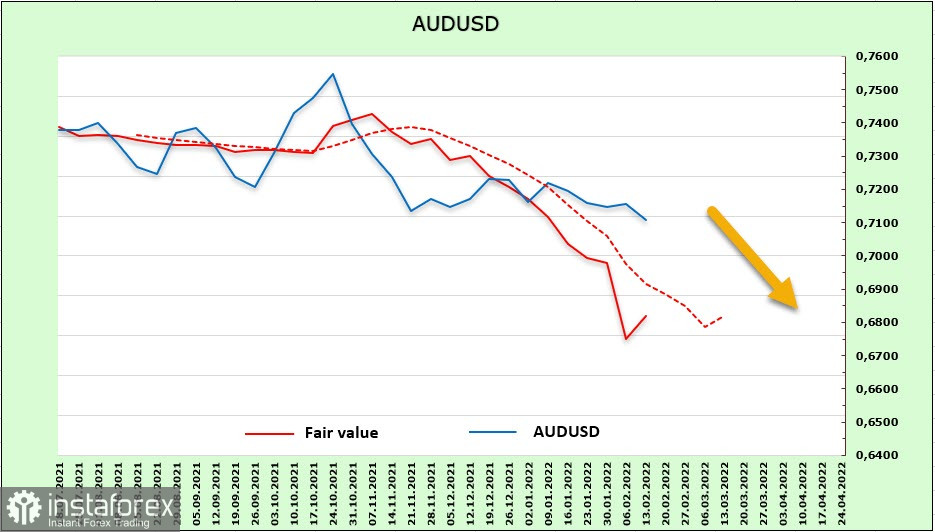

AUD/USD

The Australian dollar continues to be under pressure despite the rise in commodity prices. The CFTC report showed that the net short position did not decrease over the past week but even increased by 436 million, namely to -6.127 billion. This is a strong bearish edge. The settlement price shows the first signs of the end of the decline, which gives a chance for a corrective pullback.

Given the faster-than-predicted economic recovery, rate hike forecasts are shifted to late 2022, which is a weak bullish factor for the Australian dollar that will not solve anything on its own. High uncertainty remains, and the RBA's pace of normalization will noticeably lag behind Fed.

The Australian dollar continues to trade closer to the middle of the bearish channel. The probability of breaking through the support level of 0.70 and moving further to 0.6760/70 remains high, which is currently the most likely scenario. A possible upward correction is limited by the zone 0.7290/0.7300 and it is logical to use growth attempts for sales.