The ongoing conflict in Ukraine has completely overshadowed the events in the global economy. In fact, this week, the attention of investors will be fully drawn to Fed Chairman Jerome Powell, who is expected to comment on the future policy of the central bank in the context of global crisis, the ongoing COVID-19 and the military conflict in Ukraine, which has brought the world to the brink of a nuclear catastrophe. It was previously pointed out that the market has an opinion that the Fed, in the wake of the aforementioned events, may go for a less aggressive increase in interest rates. For example, rates will not be raised by 0.5%, but by 0.25% instead.

In terms of statistics, there will be data on US employment on Wednesday, which many expect to show an increase. They assume that new jobs in the non-agricultural sector rose by about 350,000 in February, as compared to a fall of around 301,000 in January. If the numbers do not disappoint, then demand for dollar will surge. Another employment report will be released on Friday, where many expect to see a 450,000 rise in jobs.

How will the markets react to this data?

If, in general, both the reports from ADP and the Department of Labor turn out to be higher than the estimates, the Fed will be forced to raise rates by 0.50%. This is because they have to fight the growing threat of inflation, which has reached 40-year highs.

Positive data from the US will also lead to a sharp increase in dollar.

Forecasts for today:

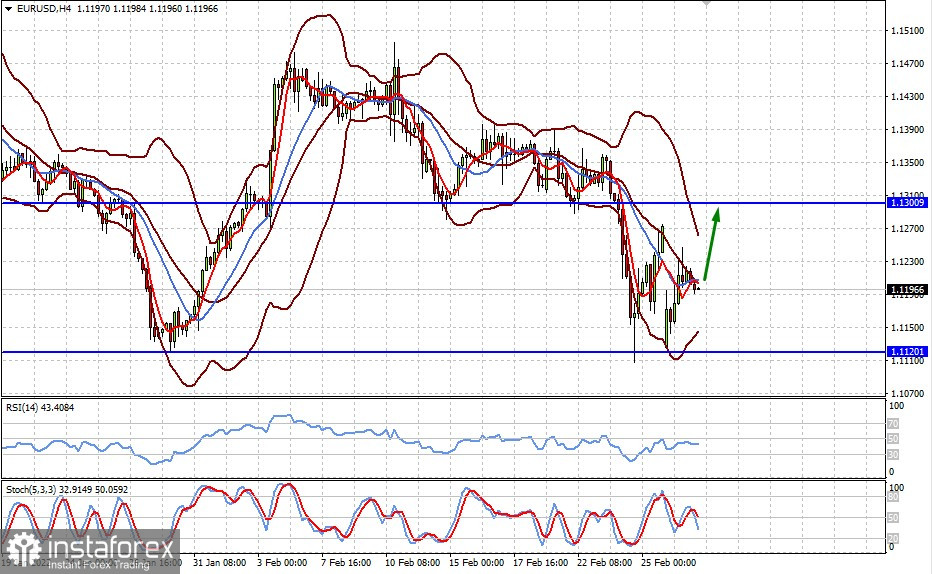

EUR/USD froze in anticipation of the EU inflation data tomorrow. Many expect that it will grow 5.3% y/y, from 5.1%. If that really happens, euro will rise to 1.1300.

Rising inflation may force the ECB to raise interest rates at its next meeting.

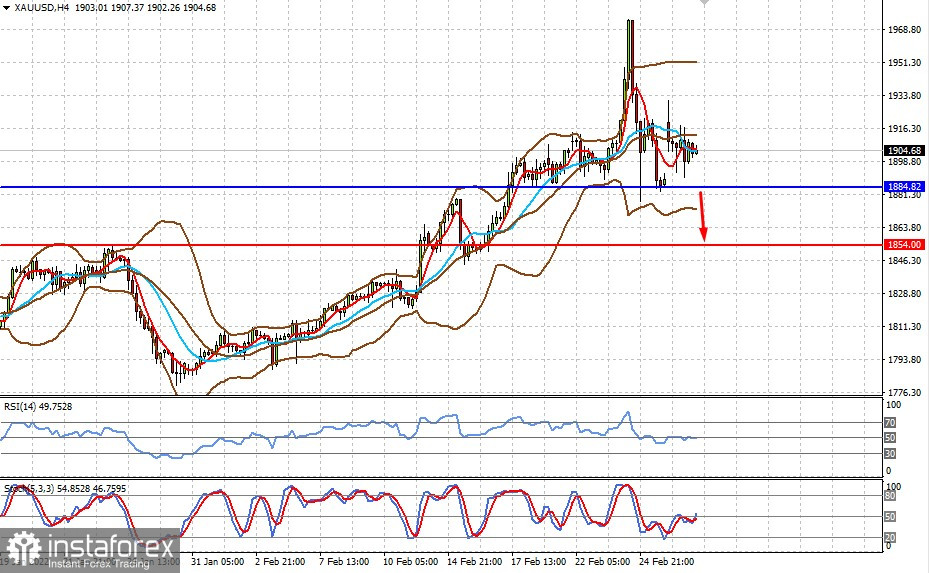

Spot gold is consolidating near 1900.00. Positive data from the US labor market and a possible decrease in geopolitical tensions around Ukraine may lead to a weakening of interest in gold as a defensive asset. In this case, we can expect a decline to 1854.00.