The dollar is strengthening, and the dollar index (DXY) is rising at the beginning of today's European session.

The driver of the current growth in DXY is the British pound (its share in DXY is approximately 12%). The sterling has been actively declining since the opening of today's trading day, and especially since the beginning of the European trading session after the release of a weaker-than-expected UK retail sales report by the UK Office for National Statistics (in March, retail sales fell by 1.4%, while economists expected a fall of 0.2%) and a report by Markit Economics, indicating a fall in the UK composite Purchasing Managers' Index (PMI) in April to a 3-month low of 57.6 from 60.9 in March (the forecast was 58.5 ). Index values above 50 indicate an increase in activity, however, a relative decrease in the indicator may negatively affect the quotes of the national currency.

The decline in S&P Global/CIPS composite purchasing managers' index was also attributed to higher prices and rising costs of living. S&P stressed that Covid-19 continues to negatively impact many companies. In addition, the consequences of Brexit and the increase in the delivery time continue to slow down export sales, while the military conflict in Ukraine and the sanctions imposed on the Russian economy negatively affect the UK's foreign trade.

GfK's consumer confidence indicator released yesterday, which fell in April to the lowest level since 2008-2009 to -38 (after falling to -31 in March), only complements the current negative picture for the pound.

The possible resignation of Prime Minister Boris Johnson is also added to the above negative factors.

Today, market participants who follow the pound quotes will pay attention to the speech (at 14:30 GMT) of Bank of England Governor Andrew Bailey. Financial market participants are waiting for clarification of the situation from him regarding the further policy of the country's central bank in the current conditions of a sharp deterioration in the geopolitical situation in Europe and economic indicators in the UK. Bailey may also give explanations regarding the decision taken by the BoE a month ago to raise the interest rate (the next meeting is scheduled for May 05) and touch upon the state and prospects of the British economy after Brexit and the partial lifting of quarantine restrictions due to the coronavirus. If Bailey does not touch on monetary policy issues, then the reaction to his speech will be weak.

Meanwhile, the dollar received support after yesterday's statements by Fed Chairman Jerome Powell signaling the possibility of raising interest rates by half a percentage point in May. He also made it clear that such increases may be required in the future to reduce inflation. "It is appropriate in my view to be moving a little more quickly," Powell said.

Powell stressed that the market is "overheated" and that it is their job to bring it to a more constructive mix of supply and demand. The Fed, according to him, is primarily "focused on lowering inflation."

"The economy doesn't work without price stability," Powell said.

The Fed is trying to cope with the difficult task of providing a "soft landing" for the economy, while also helping to reduce inflation. "I don't think you'll hear anyone at the Fed say that that's going to be straightforward or easy," said Powell.

Investors now expect the Fed to raise rates by 50 basis points in each of the next two meetings, and the growing divergence in the Fed's and other major global central banks' conditional monetary policy curves will further strengthen the dollar and lift the DXY index, economists say.

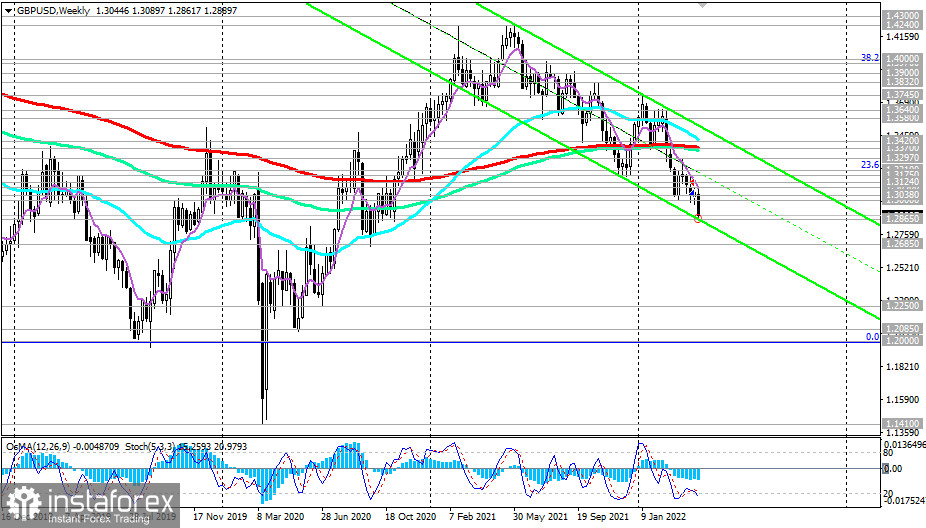

Meanwhile, today the GBP/USD pair has updated the minimum since November 2020, also reaching an intraday low near 1.2865. The next immediate target in case of further decline is 1.2800, 1.2700, and 1.2685.