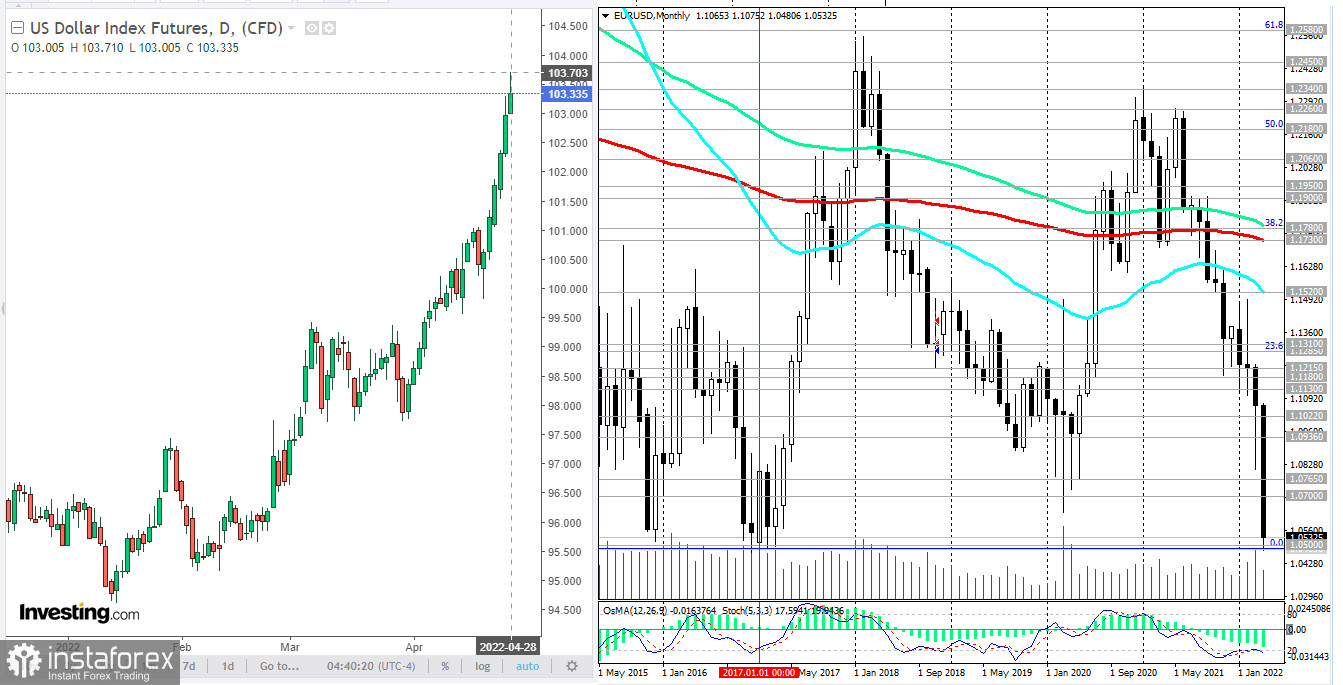

At the time of writing, EUR/USD was trading near 1.0533, up from today's and a new 5-year low of 1.0480. In April, the EUR/USD pair "lost" more than 5%.

Economists at Commerzbank said yesterday that if Russian gas supplies to Europe are cut off on a large scale (Russian gas supplies to Poland and Bulgaria are currently cut off), large parts of the EU, especially the eurozone, will be at risk of recession. In their opinion, the euro in this case can reach parity against the dollar.

The EUR/USD pair is falling not only due to the weak euro but also to the strengthening dollar ahead of the Fed meeting next week.

Cleveland Federal Reserve Bank President Loretta Mester said in a media interview on Friday that she expects the central bank to raise rates by half a percentage point following its regular meeting on May 3-4, but more hikes will follow.

"I would say 50 basis points will be on the table for the May meeting," said Fed Chairman Jerome Powell last week. The president of the Federal Reserve Bank of New York, John Williams, also said that raising the rate by half a percentage point is "a very reasonable option."

Thus, the accelerating divergence of the curves reflecting the direction of the monetary policies of the Fed and the ECB will continue to encourage dollar purchases at the expense of the depreciating euro. How can one not remember the carry-trade strategy, when a more expensive currency is bought at the expense of a cheaper one in the expectation of a further divergence of their exchange rates.

Of the news for today, which will cause an increase in volatility in the market and in the EUR/USD pair, it is worth highlighting the publication (at 12:00 GMT) of the preliminary harmonized consumer price index (HICP) of Germany, which is an indicator for assessing inflation and is used by the Governing Council of the ECB to assess the level of price stability (forecast 7.6% in April against 7.6% in March, 5.5% in February, 5.1% in January), and a preliminary estimate of the US annual GDP. This indicator is one of the key (along with data on the labor market and inflation) for the Fed in terms of its monetary policy. If the data points to a decline in GDP in the 1st quarter of 2022, the dollar could come under pressure. Forecast: 1.1% (versus 6.9%, 2.3%, 6.7%, 6.3% in previous quarters of 2021).