The dollar is in no hurry to move into a correction, despite the current strong overbought. In the short term, the US dollar index is expected to consolidate around the highest levels in 20 years. The next resistance lies at 104.20. A breakthrough higher would be at 105.00 and 105.63 (11 Dec 2002 high).

Meanwhile, there is some stabilization of risk sentiment on Tuesday, which is happening to the detriment of the greenback. A strong and prolonged correction is not expected, ING economists say. Buying interest will remain, given the tightening of the Federal Reserve's policy, concerns about economic growth and unstable sentiment towards risky assets.

Currencies that are correlated with the business cycle are under a lot of pressure right now. Investors are reducing investments in countries that show outstripping growth in the phase of the business cycle upturn. The Australian and New Zealand dollars sank 3-4% against the US counterpart, the decline of the pound and the euro turned out to be slightly less - 1-2%.

The economies of Australia and New Zealand cannot help feeling the pressure coming from a slowing China. For them, China is one of the main trading partners, and liquidity concerns primarily affected the Norwegian krone. The USD/NOK pair has gained almost 5% since May 5.

The Fed said in its report on financial stability that liquidity in key markets is declining. It was a kind of signal for investors to flee from risky assets. After such a warning from the central bank, the decline intensified.

Further movement in the currency market will depend on the incoming news. Today, the calendar is not of particular interest to traders. Market players may take a look at the NFIB report on small businesses in the US, in particular, how firms assess the situation in the labor market. Of course, the speeches of a number of officials will not be missed. Markets are focused on forecasts of further policy tightening in the US. In addition, they are interested in whether officials will voice fears of stagflation in the country.

The focus on Wednesday will be on inflation data. Annual inflation is expected to slow to 8.1% in April from 8.5% a month earlier. The indicator has continuously accelerated over the past seven months. Even if it slowed down in April, it won't change anything about the Federal Reserve's rate plans. At the June meeting, the Fed is likely to raise rates again by 50 bp.

While other global central banks are falling behind the Fed, their national currencies are suffering. If the Bank of England (BoE) raises rates, which does not particularly save the pound from falling, then the European Central Bank is only at the stage of discussing this topic. Bullish momentum in the EUR/USD pair can be created by officials such as Joachim Nagel and De Guindos, whose rhetoric is associated with the prospect of a rate hike at the July meeting. The EUR/USD pair is likely to be the most sensitive to these comments, as a rate hike in Europe is not a settled matter, but only a matter of debate. It is difficult to say how long it will take the doves and hawks of the ECB to come to an understanding.

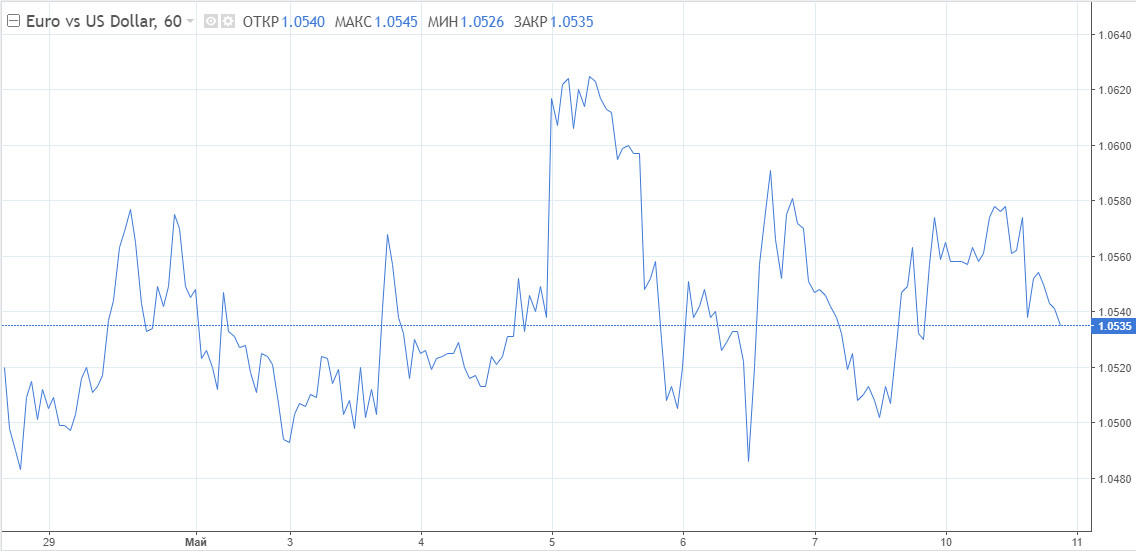

From a technical point of view, the EUR/USD quote still remains in the 1.0480-1.0600 range in anticipation of new important information. The potential for strengthening towards 1.0600 and above is present, but it will be problematic to realize such a rebound.

If the bounce picks up further momentum, then bulls should first break the round at 1.0600 and then aim for a weekly high at 1.0640.However, it is unlikely that the euro will be able to adjust higher, taking into account the discussion of the embargo on Russian oil.

The attempt will be doomed to failure. With the abandonment of Russian oil, the EU will face a new round of inflation, which, as the movement of the single currency in March and April has already shown, should negatively affect the subsequent dynamics and forecasts for EUR/USD.

The GBP/USD pair tried to develop a corrective momentum on Tuesday. The pound has retreated from the lows since June 2020 around 1.2250, but it is not easy to settle above the 23rd figure.

Analysts are skeptical about today's attempts by pound bulls to organize some positive movements today. The recovery of the British currency will not last long anyway, as the general fundamental background does not favor the growth of risky assets. As confirmation of this version, one can name a landslide Monday. Global stock markets have experienced the biggest crash since the start of the pandemic in 2020. Traders will continue to bet on defensive assets.

This is far from the only reason why the pound is ordered to go up. The BoE raised the rate to 1% last week and predicted a peak inflation of 10.2%. The central bank's leadership does not rule out a further rise in prices in the country, and they are expected to grow faster than the country's citizens. As a result, there will be an even stronger decline in consumer activity.

With such realities, the UK economy in the fourth quarter is waiting for a recession. According to the BoE, GDP will contract by 0.25% in 2023, while growth of 1.25% was previously forecasted.

In the GBP/USD pair, bearish sentiment will intensify, so selling is most profitable. The first target is 1.2100.