When supply and demand pull the blanket over themselves, wait for consolidation! Brent is wandering around $92 per barrel in the mode of a damped pendulum. However, behind external calmness, the market hides internal instability. Instead of balancing it with a 2 million bpd cut, OPEC+ added uncertainty. The cartel made investors talk about geopolitical risks. Does Saudi Arabia support Russia or not? Are the White House attacks on Riyadh justified?

The role of jokers in the deck is still claimed by China and Russia. China, with its zero patient policy, has significantly confused investors. On the one hand, the reluctance of the PBOC to raise the key rate for the second month in a row and the extension of the maturity of medium-term loans indicate Beijing's commitment to loose monetary policy, which, in theory, should support demand. On the other hand, China has postponed the release of data on GDP for the third quarter. Are they really that bad because of COVID-19? If so, then the oil market should start to get nervous.

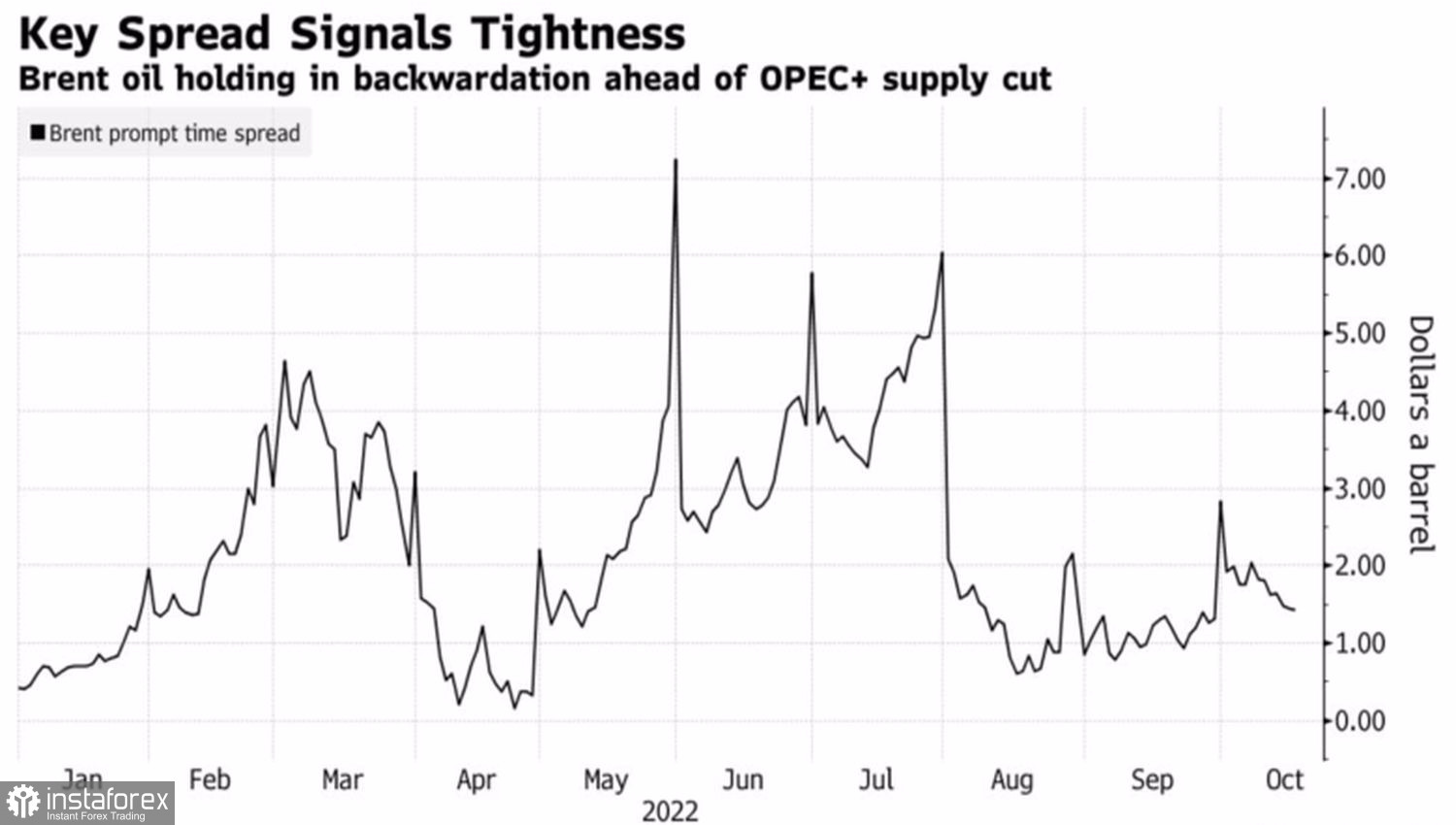

Spread dynamics in the oil futures market

Fearing a catch in the form of an unexpected rise in oil prices, the US spread rumors about the sale of another portion of barrels from the strategic reserve. In case of unforeseen circumstances, figures of 10-15 million appear. Inside Reuters claims that in the 2022-2023 fiscal year, which started in October, the White House may start with 26 million barrels.

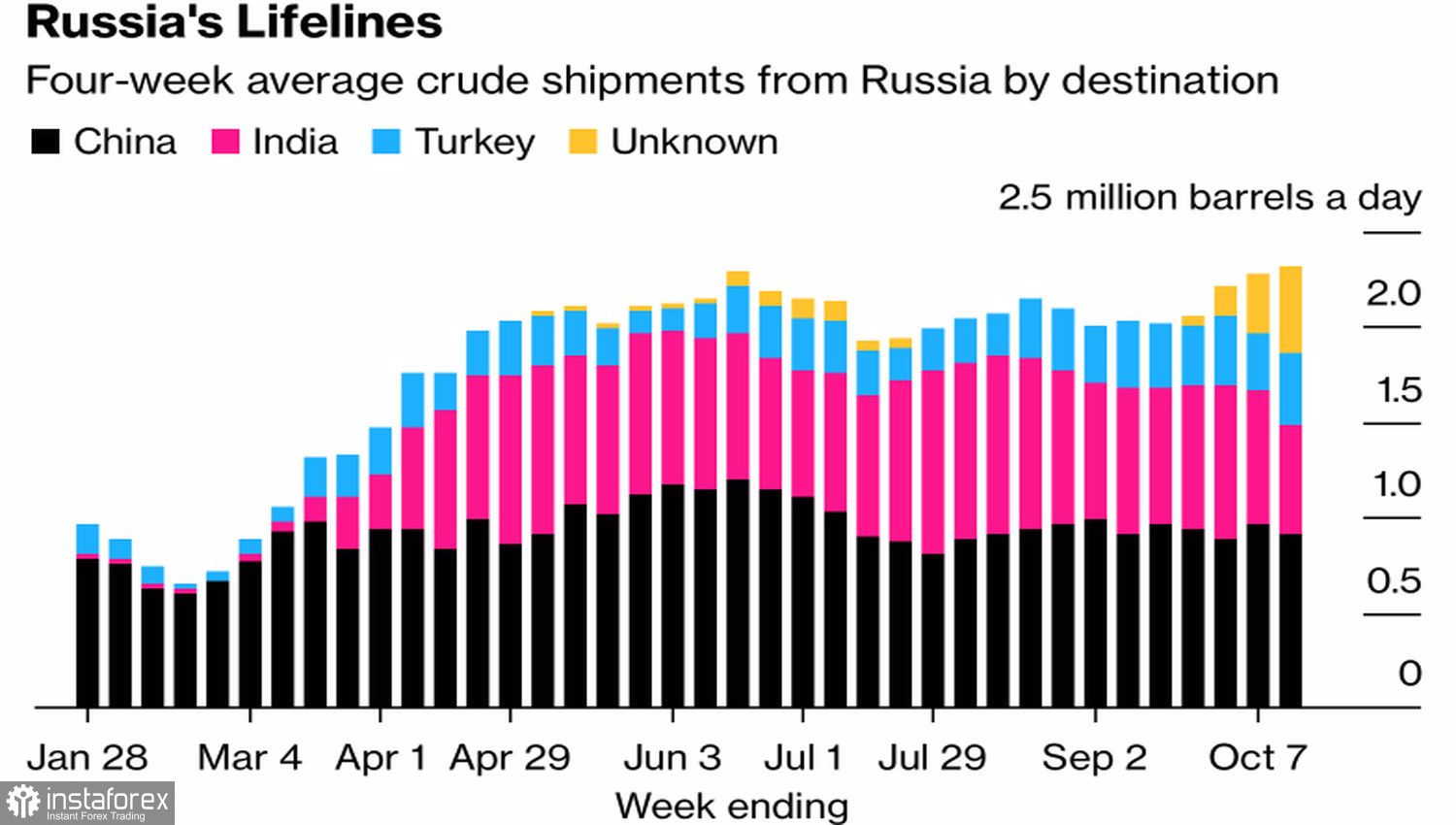

The third source of uncertainty is Russia. Before the imposition of an EU embargo on its oil, there is nothing left, and the cards do not stop shuffling. Formally, sea flows of oil from the Russian Federation to the three largest consumer countries represented by India, China and Turkey decreased by 350,000 bpd, however, the volumes on tankers, which have yet to show their purpose, increased by 450,000 bpd. It is quite possible that the three buyers are increasing their activity.

Dynamics of offshore oil flows from Russia

In my opinion, secrets are connected with Europe. It often happens that in anticipation of the bans, which will come into force in early December, oil importers increase their activity. If so, we will see a reduction in supply from Russia soon, which is bullish for Brent.

However, the bears are not particularly upset. According to the Bloomberg model, the probability of a recession in the US has jumped from 65% to 100% over the next 12 months. Experts polled by a popular publication expect that the GDP of the eurozone in 2023 will decrease by 0.1%, Germany - by 0.5%. China, with its COVID-19, is forced to hide statistics. The situation in the world's largest economies leaves much to be desired, which is hitting global demand and pushing oil down.

Technically, on the daily chart, Brent is trading in close proximity to fair value at $92/bbl. Here is the upper limit of the long-term downward trading channel. Under such conditions, we buy oil from $95 and sell from $91.