Since the Bank of England governor's address was on Tuesday, we should begin with him. Yesterday, Andrew Bailey made several significant claims. He specifically mentioned the country's severe labor shortage and low unemployment. In the scope of the negotiating process between employers and labor, this circumstance calls for a change in advantages. In other words, contenders for a post now dictate their demands to the employer, who must likewise meet the applicant's compensation demands. The increase in wages, according to Bailey, can "inject new life" into efforts to combat inflation. The consumer price index should benefit from the decline in energy prices, but lowering inflation may be hampered by the rise in wages.

Six months ago, I wrote about the labor shortage in the UK. Many migrant workers started to favor EU nations over the UK after Britain left the EU since it was objectively harder to get a work permit in the UK. There is now a 300,000-employee shortfall across many industries. So I can state the following in light of UK pay: They are still expanding (the most recent report shows +6.4%), but at a slower rate than inflation (10.5%). As a result, Britons' real incomes are decreasing. At the same time, the more wages grow, the slower inflation falls. And as today's news demonstrated, it hasn't yet plummeted.

The indicator only fell by 0.2% in December as the consumer price index slowed to 10.5% y/y. I wouldn't even consider such a decline to be a decrease. From its 40-year high of 11.1%, inflation has dropped by 0.6% in the past two months. According to Andrew Bailey's predictions, the reduction in energy prices should slow the rate of price growth in 2023, but it's important to keep in mind that the Bank of England has already raised the rate eight times in a row, which caused inflation to decline by 0.6%. For instance, the indicator has been falling in the United States for six months straight while falling faster in the European Union for two.

Thus, a minor slowdown in inflation necessitates more vigorous action on the part of the Bank of England. Although I cannot guarantee it, the market anticipates that the regulator will begin to speed up the tightening of monetary policy again. Given everything mentioned above, there was a rise in demand for the British pound today. However, if the Bank of England only increases the rate by 25 basis points in early February, it may be a significant letdown and cause a steep decline in the value of the British pound. Although there is a severe recession in the UK, data from November showed that the economy is increasing slowly rather than contracting. At its upcoming meeting, the Bank of England will likely increase the rate by 50 basis points. The British shouldn't be shocked by this.

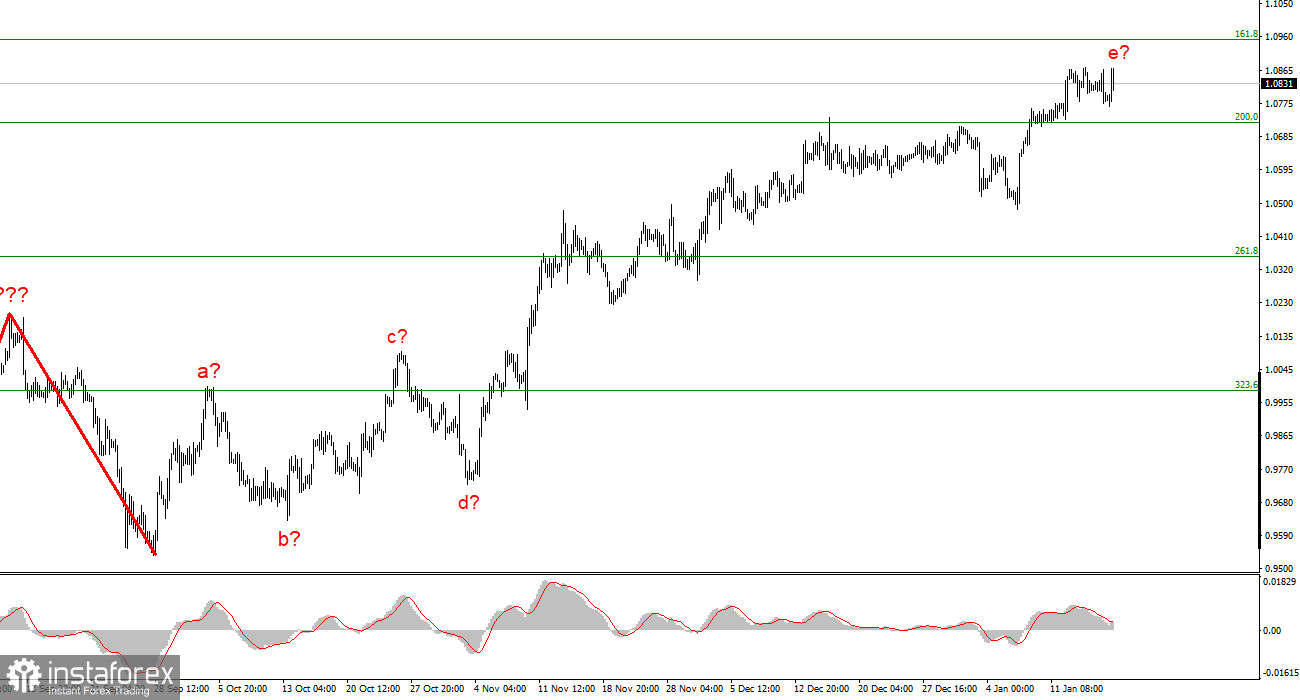

I conclude that the upward trend section's building is about finished based on the analysis. As a result, given that the MACD is indicating a "down" trend, it is now viable to contemplate sales with targets close to the predicted 0.9994 level, or 323.6% per Fibonacci. The potential for complicating and extending the upward portion of the trend remains quite strong, as does the likelihood of this happening. The market will be ready to finish the wave e when a bid to break through the 1.0950 level fails.

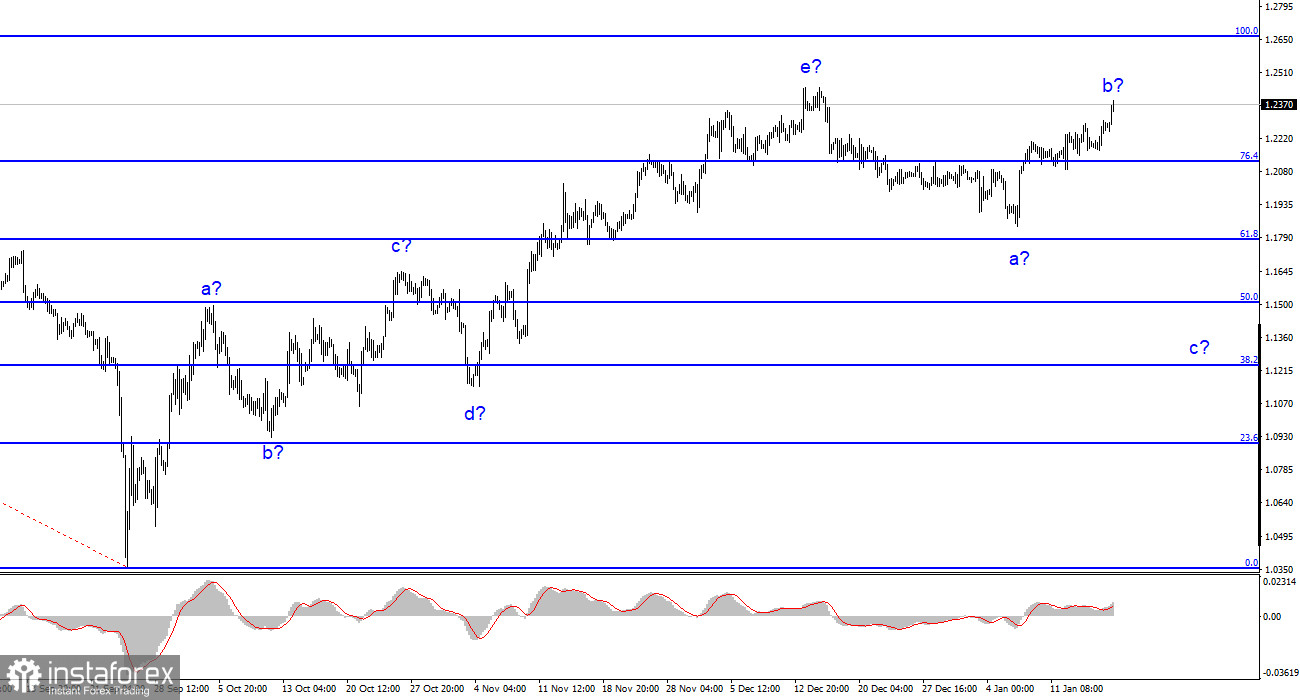

The building of a downward trend section is still assumed by the wave pattern of the pound/dollar instrument. According to the "down" reversals of the MACD indicator, it is possible to take into account sales with objectives around the level of 1.1508, which corresponds to 50.0% by Fibonacci. The upward portion of the trend is probably over, however, it might yet take a longer form than it does right now. However, you should exercise caution when making sales at this time because the value of the pound tends to rise.