Oil is an indicator of the health of the global economy. It is not surprising that when caution replaced euphoria in the diagnoses of its further development, Brent took a step back. Yes, the improvement in the IMF forecast for global GDP for 2023 from 2.7% to 2.9% can be considered a bullish factor for the North Sea variety, as well as positive statistics on Chinese business activity. However, these factors have already been taken into account in the futures quotes, while investors are concerned about other topics.

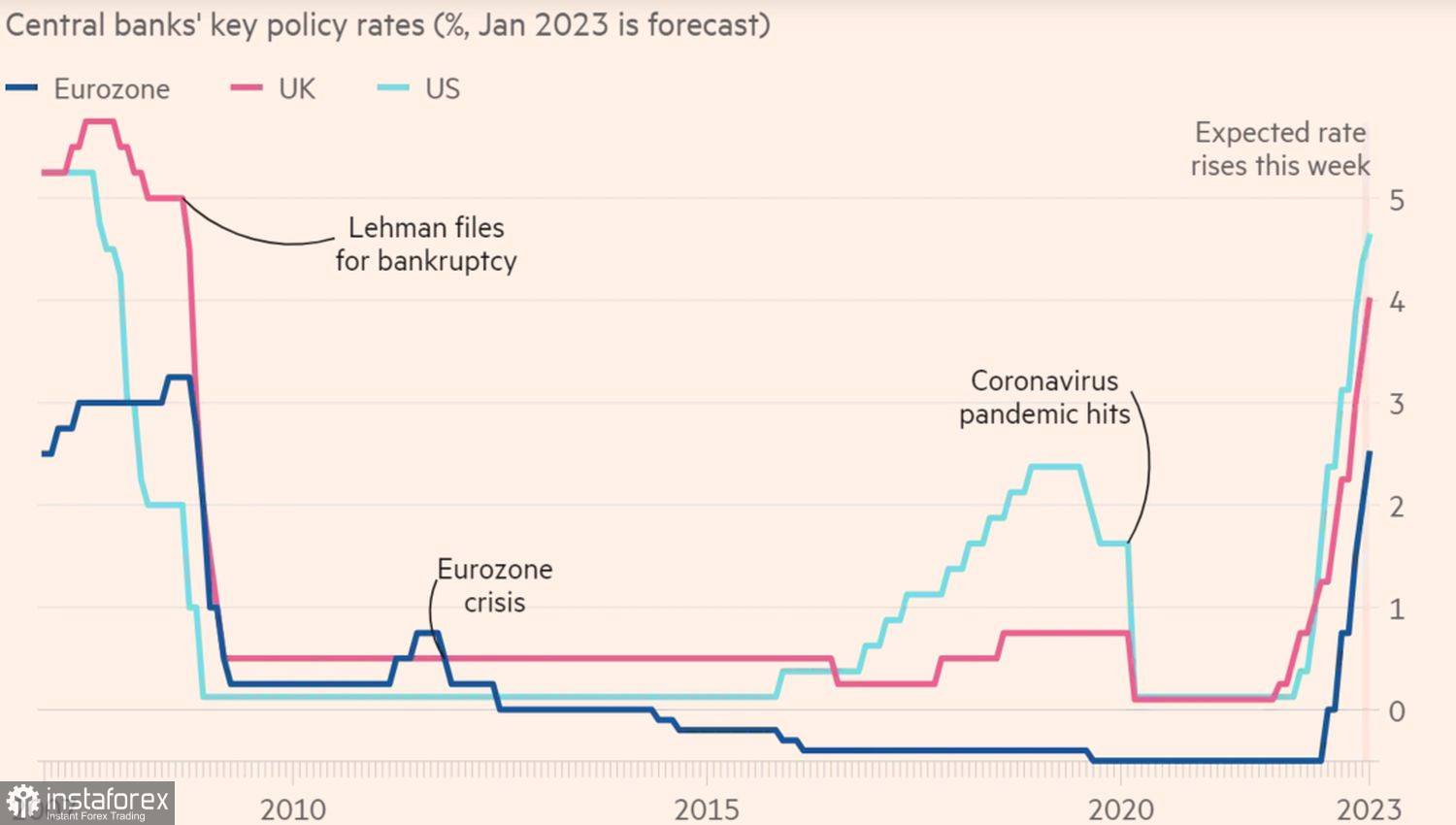

Numerous meetings of the world's leading central banks, ready to raise rates to 15-year peaks and continue the most aggressive monetary restrictions, have returned the topic of recession to the market's focus for several decades. So far, events in the world economy are developing like a textbook: high inflation - tightening of monetary policy - recession in the economy. In this scenario, the demand for oil usually suffers. So wouldn't it be better to wait out the meetings between the Fed and other regulators, then start buying Brent again? Add to that a possible surprise from OPEC+, which could further cut production, and the caution looming over the market becomes quite understandable.

Dynamics of rates of the world's leading central banks

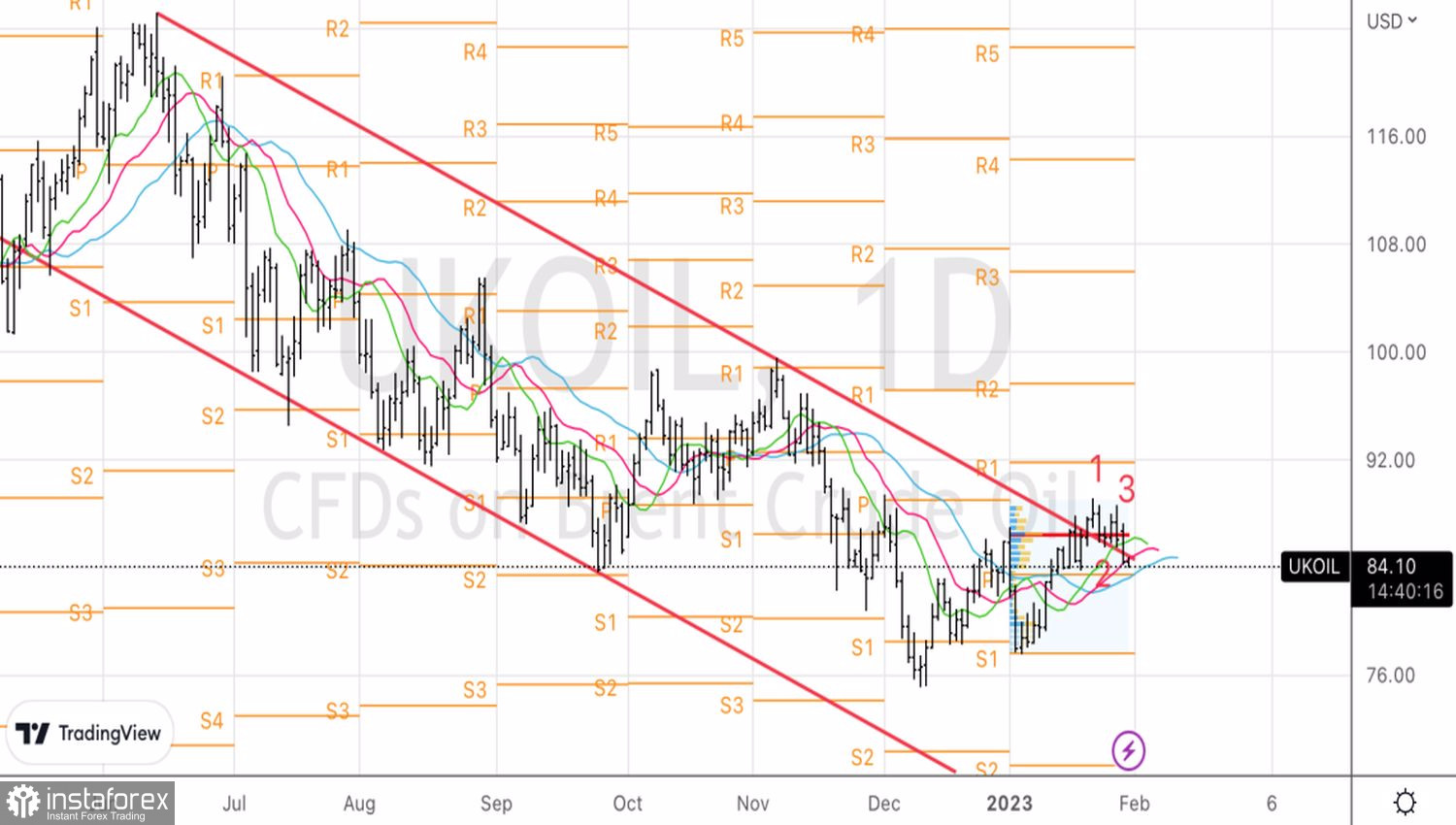

Investors prefer to walk away from risk on the assumption that Jerome Powell will use hawkish rhetoric. The closing of speculative positions on the North Sea, which reached its highest level in 11 weeks on January 24, is the basis of the pullback. To make things worse, the Brent and WTI tested the 100-day moving average, which brings in technical sellers.

However, the increase in backwardation from 3 to 60 US cents per week indicates that the success of the bears are temporary.

Dynamics of WTI and moving average

Indeed, the IMF is more optimistic than it was in 2022. It believes that the global economy will look stronger in 2023 as Europe adapts to the energy crisis, the reopening of China's economy, improved financial conditions and the weakening of the U.S. dollar. China's GDP will accelerate from 3% to 5.2%, which will be a tailwind for commodities. And Beijing is already beginning to justify the advances given to it: in January, China's manufacturing PMI rose above the 50 mark for the first time in 4 months, indicating an expansion of the economy.

Oil is under pressure from rumors of a 50% increase in Russian oil shipments from Baltic ports in January compared to December, amid growing demand in Asia and potentially higher prices. But this may be a temporary phenomenon. Oil exports from Russia will decline going forward.

Technically, the bears on Brent are making titanic efforts to return quotes to the lows of the downward long-term trading channel and win back the 1-2-3 pattern. Nevertheless, a rebound from the $83.5–84 convergence zone or a return of oil above $85.75–86 per barrel should be used for buying.