The US dollar traded mixed on Wednesday, commodity currencies weakened, defensive currencies (yen and Swiss franc) strengthened, and the demand for risk is decreasing.

Given the hawkish comments of FOMC members Bullard and Meester, in which they hinted that they advocated a 50-point rate hike at the last meeting, the markets will now carefully study the FOMC minutes in order to find out what arguments were offered for such a hike. The chances that the Federal Reserve will increase the pace of tightening again are slim, but the possible hawkish tone of the minutes (increased support for larger hikes or a growing feeling on the part of politicians that they are considering a policy peak at a slightly higher point) will reinforce expectations that the Fed cycle will exceed 5.25% in the middle of the year. If such a conclusion is made, the dollar will inevitably strengthen across the entire spectrum of the market.

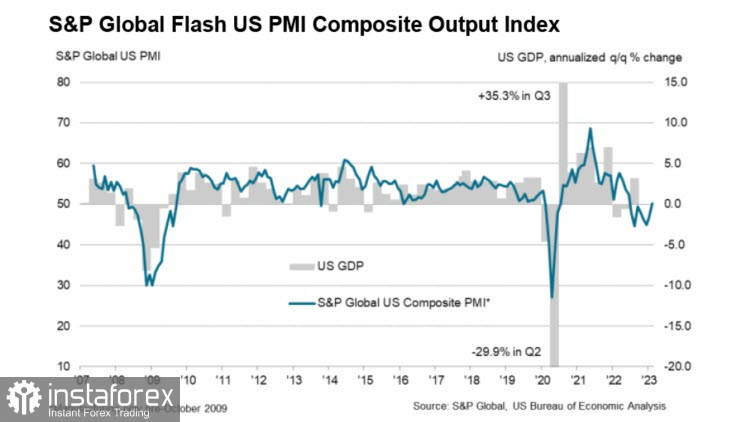

The February PMI in the US, following Europe and the UK, also turned out to be better than forecasts, the manufacturing index rose to 47.8 points (46.9 in January), and the services index returned to the growth zone at 50.5 points (46.8 in January).

Strong PMI supported the yield growth, 10-year UST approached 4%, the dollar is receiving support as the threat of recession has decreased, and the Fed may see a peak rate above current market expectations. European bond yields are also rising, as the European Central Bank is now expected to take more decisive action. The yield of 5-year TIPS bonds rose to 2.58% on Tuesday, compared with 2.09% on January 19, there is a possibility that inflation in February will show a higher value than in January.

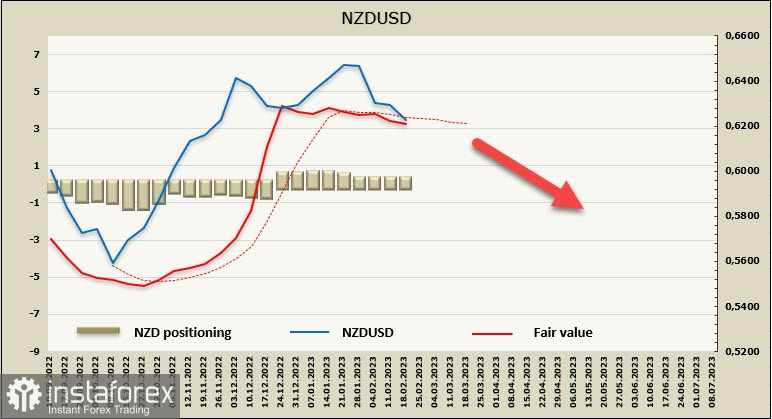

NZDUSD

The consequences of the devastating cyclone Gabrielle, which covered New Zealand in February, turned out to be catastrophic and left their mark on expectations for the Reserve Bank of New Zealand's decision, which was announced this morning. The huge consequences of the disaster, which led to large-scale destruction of infrastructure and caused serious damage to agriculture, practically ruled out a 75-point rate hike, so the final decision to raise the rate by 50 points, to 4.75%, did not surprise anyone, the markets reacted calmly, the volatility of the kiwi increased slightly.

Meanwhile, according to ANZ, a significant disruption of economic activity can be expected within months, and in the case of transport links – even years. Among other things, the disruption of transport infrastructure will negatively affect the number of tourists arriving in the country, efforts to restore the economy will lead to a shortage of resources, which, in turn, will again increase inflationary pressure. The government will have to look for a source for additional spending, which is likely to lead to a reduction in the pace of quantitative tightening.

With all that said, it should be expected that economic activity in the coming weeks will be increased due to the need to restore infrastructure, GDP growth will slow down, and inflation will receive additional fuel. All this together will put additional pressure on the kiwi.

The estimated price in the absence of CFTC data is directed downwards, the probability that the kiwi will resume growth is low.

We expect that NZDUSD will test the strength of the nearest support of 0.6186 and try to find a base in the wide support zone of 0.6125/60. If the effects of the cyclone turn out to be larger than according to preliminary estimates, it is possible that the decline will continue closer to 0.6000, but there is too little data to be sure.

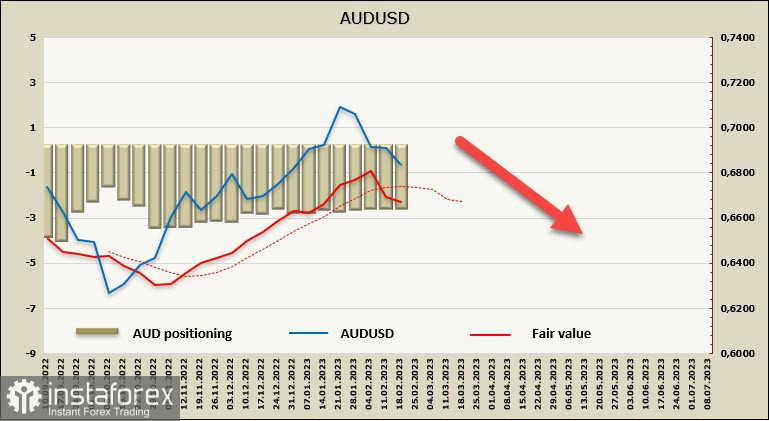

AUDUSD

The Reserve Bank of Australia minutes published on Tuesday were regarded by the markets as hawkish, since, as follows from the text, a 50-point rate hike was discussed at the Bank's meeting in early February. It is noted that at the moment the interest rate in Australia is lower than in other countries, and even if we take into account that wage growth is lagging behind, the positive effect from higher commodity prices and additional savings accumulated by households was estimated to be greater than in other countries. In other words, there is a serious threat of increased inflationary pressure in Australia, and the efforts of the RBA may not be enough.

Wage growth in the 4th quarter of 2022 was 0.8%, which is slightly below forecasts, annual growth accelerated from 3.2% to 3.3%, which is below the RBA forecast of 3.5%. This year, the RBA expects wage growth (4.2%) to accelerate. RBA Governor Philippe Lowe said last week that at the moment the results on wages do not contradict the fact that inflation is returning to the target level in a fairly painless way. It became clear from the RBA minutes that inflation is an absolute priority, and this is a positive signal for the aussie, however, it is not strong enough.

The estimated price has turned down, while there is no CFTC data, we assume that the priority is bearish.

AUD USD has fallen to a two-month low, there is reason to expect that the decline will continue. The nearest resistance is 0.6860, where the sell-off may resume, the target is 0.6775. US data could trigger some movement, updated data for the 4th quarter will be published on Thursday, personal income and expenses for January will be published on Friday, which will adjust inflation expectations, and as a result, the forecast for the Fed rate.