China has allowed the euro to catch its breath. The growth of China's economy from 2.2% in the fourth quarter of last year to 4.5% in the first quarter of this year has become a real balm for the wounds of the EURUSD bulls. If in 2022, the largest Asian economy marked a modest 3% GDP growth due to COVID-19 problems, then in 2023, it is ready to aim for 5%. There is no better news for the export-oriented eurozone and its currency.

Fifteen years ago, China helped the Fed rid the global economy of the crisis. Now the IMF has high hopes for it. According to the authoritative organization, a third of global GDP growth this year will be associated with China. If its economy continues to accelerate, the improvement of appetite for risk will give the green light to the bulls on EURUSD.

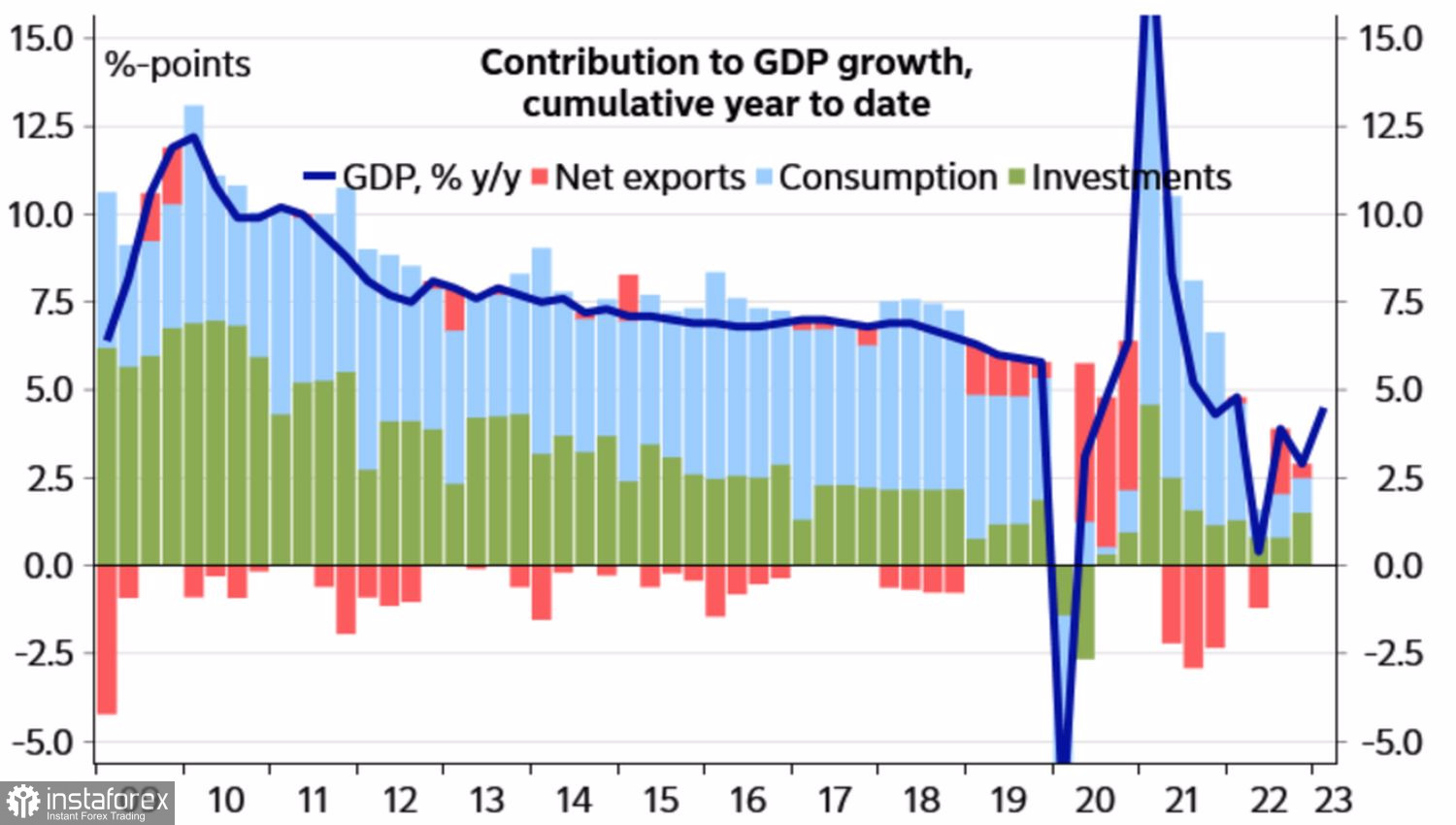

Dynamics and Structure of the Chinese Economy

The continuation of the rally of the main currency pair is supported by the "hawkish" rhetoric of ECB representatives and the growth of Germany's business prospects to the highest level in a year, according to research by the German IFO Institute. Bundesbank President Joachim Nagel said the fight against inflation genie is far from over, it should be put in a bottle. The futures market is in doubt as to whether the European Central Bank will raise its deposit rate by 25 bps or 50 bps in May, which amid the potential end of the Fed's monetary tightening cycle, is supporting the EURUSD bulls.

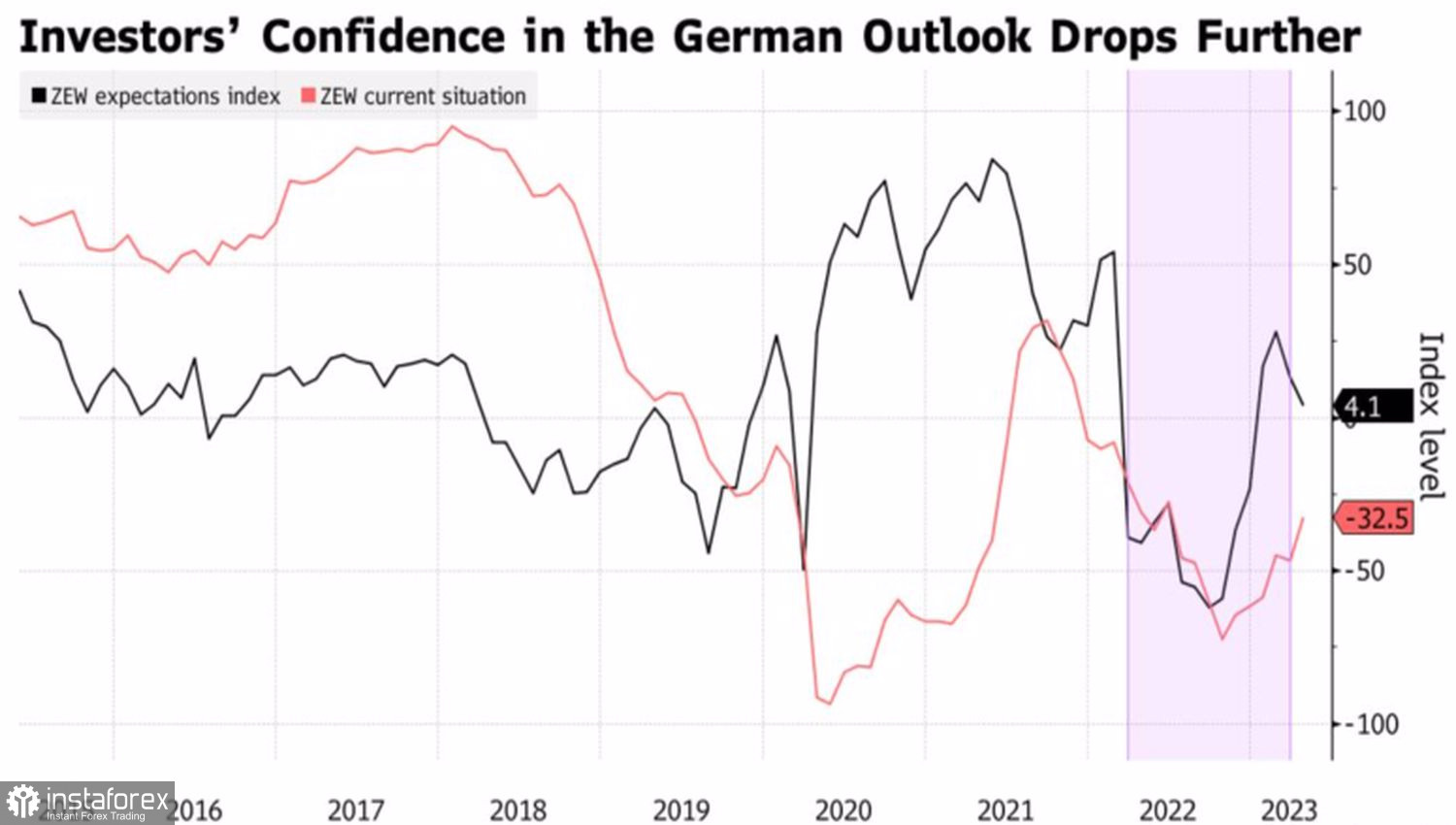

On the contrary, data from the German ZEW Institute paints a mixed picture: the business expectation indicator disappointed investors, while the index of current business conditions in Germany pleased.

Dynamics of business sentiment in Germany

The results of the polls are certainly influenced by the banking crisis and the ECB's monetary policy. What's important is that the Eurozone is no longer thinking about a recession, unlike the United States, where there is constant talk of a downturn. As a result, according to Bank of America, investors have become more cautious and increased the share of bonds in their portfolios. At the same time, the differential weighting of debt securities versus equities hasn't been this high since the 2008–2009 global economic crisis.

If a serious recession does not happen, bonds will be discarded, which will trigger a rally in yields and strengthen the U.S. dollar. The second risk for EURUSD is that the inflation rate in the U.S. will remain elevated for a long time. This will force the futures market to abandon the idea of a dovish Fed reversal in 2023 and put a leverage on the USD index.

Thus, the main currency pair both wants and pricks. Greed over a potential boom in China rivals fear over a possible continuation of the Fed's monetary tightening cycle. The consequence of this confrontation is likely to be consolidation.

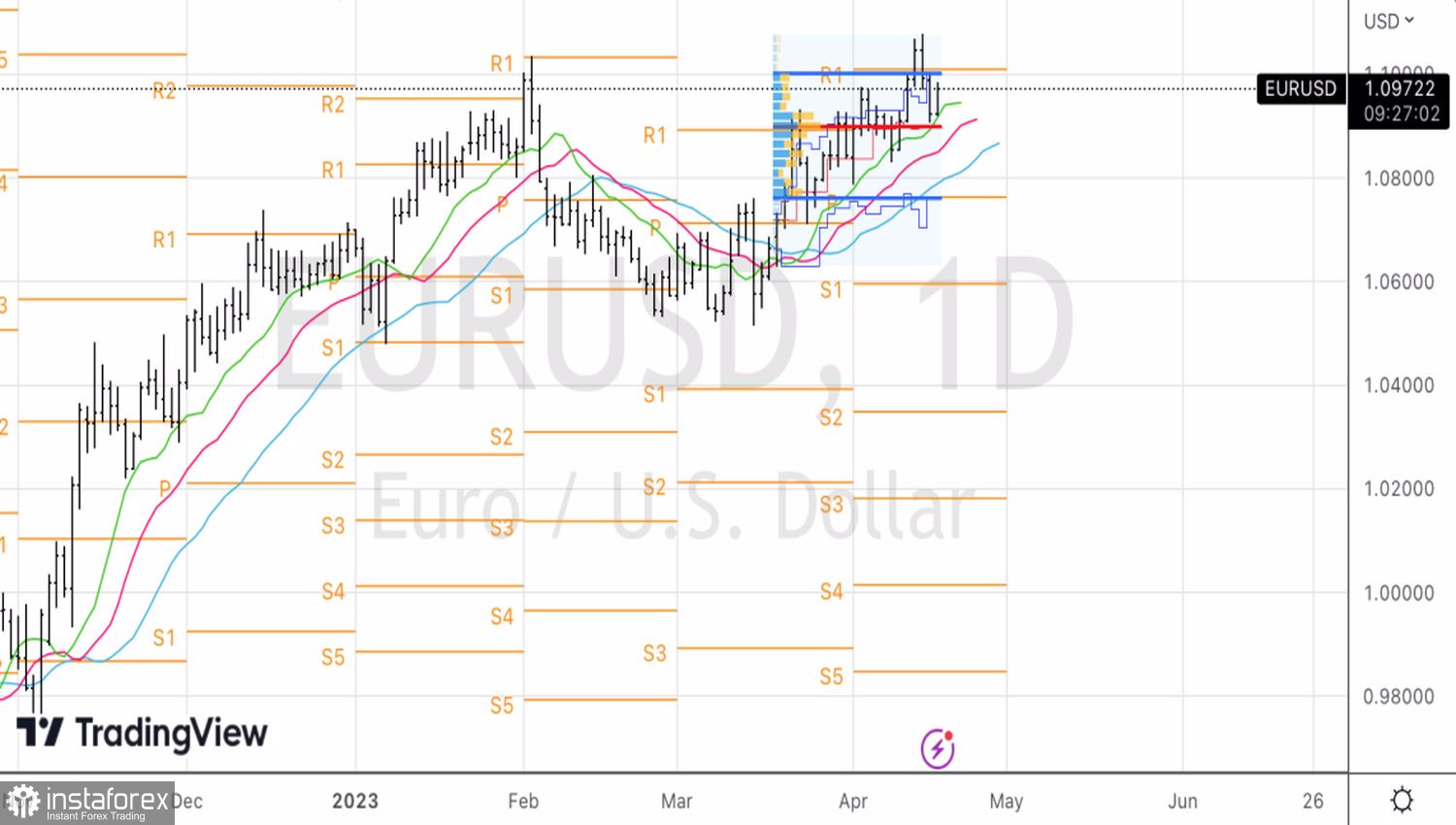

Technically, on the daily chart, EURUSD is trading within the upper part of the fair value range. A rebound from resistance at 1.1005–1.101 should be used for forming shorts. Conversely, a confident breakthrough of this level will be the basis for buying the euro.