The US Manufacturing ISM report showed an increase in positivity, with the index rising from 46.3 to 47.1. However, at the same time as the sector's recovery, we should take note that a number of sub-indices favor higher inflation – prices jumped from 49.2 to 53.2, employment increased by 3.3 points, to 50.2, and new orders are still in contraction territory.

After a pause, which optimists declared the end of the banking crisis, another bank went bankrupt - First Republic Bank. After the purchase of FRB, JPMorgan shares rose more than 2%, as JPMorgan acquired $30 billion in assets, while losses were shared with FDIC, i.e., the state. The rescue of another bank has led to the fact that FDIC has virtually exhausted all reserves, a number of small regional banks are in line for rescue, and as the crisis escalates, it will be increasingly difficult.

US Treasury Secretary Yellen warned Congress that, by optimistic estimates, the government will not be able to fulfill its financial obligations by June 1 if Congress does not raise the debt ceiling by then. Republicans have already prepared a bill providing for a $1.5 trillion increase in the debt ceiling, with a simultaneous reduction in spending of more than $4.5 trillion.

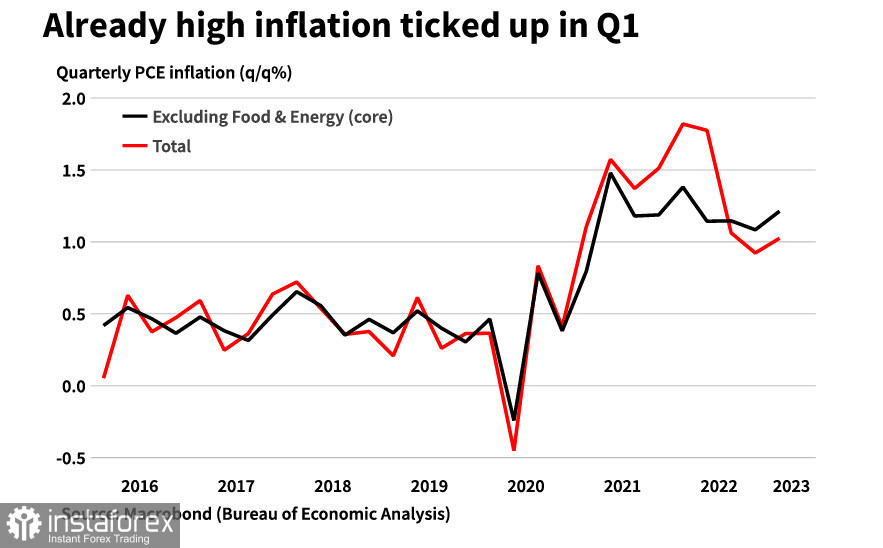

Markets will trade with low volatility until the outcome of the Federal Reserve meeting is announced. The main intrigue lies in whether the Fed will maintain the prospect of another rate hike, as there are clear signs that inflation is ready to resume growth after a pause. Q1 PCE data clearly confirms this.

Against this backdrop, oil prices have fallen again, as have commodity currencies, as the trend towards a slowdown in global inflation is called into question.

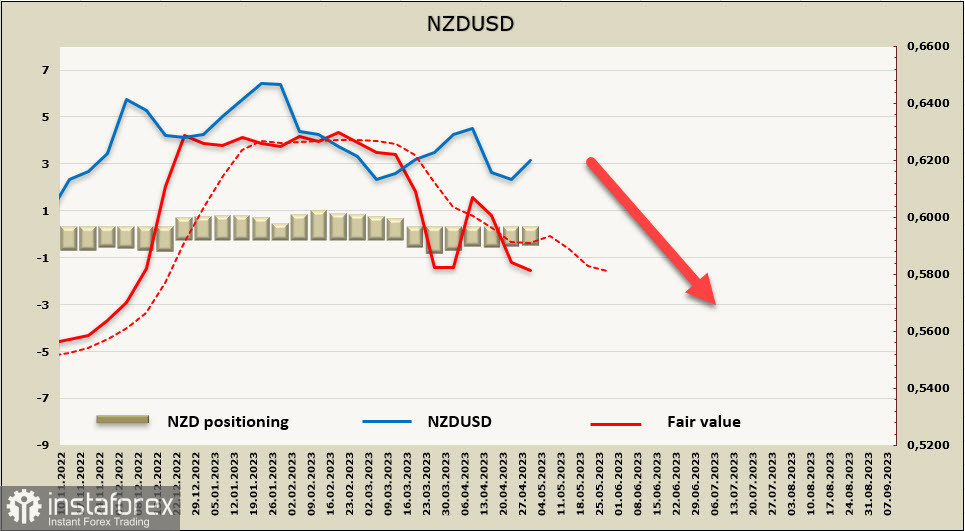

NZDUSD

The focus is on the Q1 labor market report overnight on Wednesday, with expectations moderately positive. In February, the Reserve Bank of New Zealand forecasted an increase in the unemployment rate from 3.5% in Q1 to 4.8% by the end of the year, but at the same time, a sharp increase in wages. The RBNZ expects annual growth from 4.3% at the end of 2022 to 4.9% in Q2, which will strengthen inflation expectations.

There is also another unexpected news - from June 1, the RBNZ plans to ease lending conditions. Such a decision may require a higher rate to curb inflation growth, but so far, the market has not reacted, expectations for the RBNZ's May meeting remain stable, the bank will raise the rate by 0.25%, this outcome is already priced in and will not have a significant impact on the Kiwi rate.

The net long position in NZD decreased by $43 million for the reporting week to -$200 million, with a slight bearish bias. The calculated price goes down, signaling a strengthening of bearish sentiment.

NZDUSD did not reach the support level of 0.6079, but the upward retracement is unlikely to be strong. The nearest resistance is at 0.6240/50, where we expect the growth to end and the downward reversal to follow. The next support is the mid-channel area, coinciding with the local low of 0.6105, followed by 0.6020.

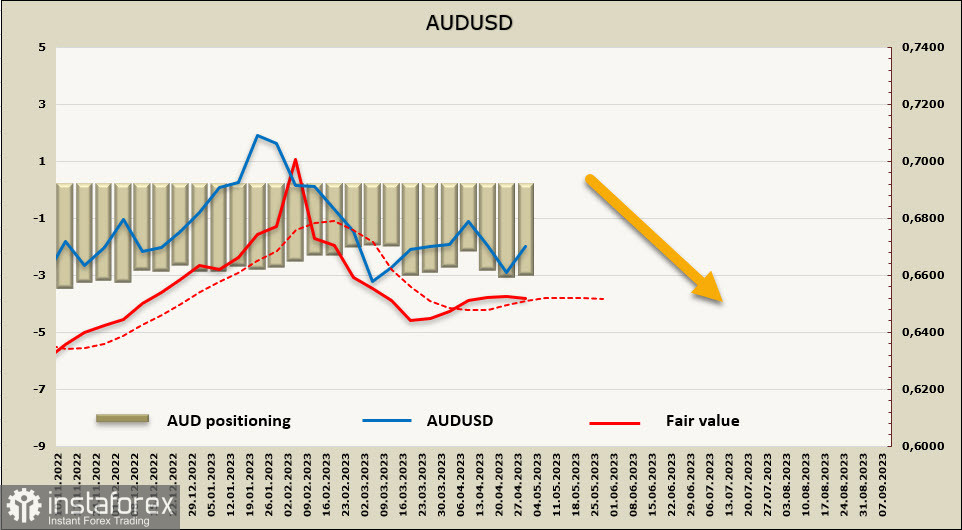

AUDUSD

The Reserve Bank of Australia surprised the markets considerably, not only did it raise the rate by a quarter point to 3.85%, but it also significantly changed the tone of the accompanying statement compared to that of April's. The statement reiterates the thesis that "some further tightening of monetary policy may be required," but emphasizes that the RBA wants to achieve this in "a reasonable timeframe," this thesis is repeated twice, unlike the previous forecast of inflation normalization in 2025. It paid more attention to wage growth.

The results of the RBA meeting are undoubtedly a bullish factor for the Aussie. Futures reacted with an increase in the probability of another 25 bps hike, and the Australian dollar became the leader in daily growth, pulling the NZD along with it.

Apparently, the RBA sees a threat of higher inflation or at least a more prolonged one, and the threat is real.

The net short position in AUD decreased by $234 million to -$2.615 billion, with bearish positioning. The calculated price lost momentum and shows signs of turning south, the forecast is neutral.

AUDUSD continues to trade in a horizontal channel, the decline expected a week ago turned out to be slightly deeper, but the subsequent bullish momentum on the background of the unexpected RBA decision quickly lost momentum. We suppose that till the end of the Fed meeting, trading will be in a narrow range, and further direction will be chosen based on the presence or absence of hawkish wording in the final statement of the Fed. By the end of the week, I expect the pair to fall to the border of the range at 0.6565.