This week, several of the largest central banks will start monetary policy deliberations following the recent hawkish surprises from the Reserve Bank of Australia and the Bank of Canada. The Federal Reserve, European Central Bank, Bank of Japan, and the People's Bank of China could trigger significant movements in the currency market.

The Fed will be the first to announce its decision, which will take place on Wednesday evening. It is expected that the FOMC will pause and hold rates steady but maintain the suspense in favor of another rate hike in July, while expectations for the start of a rate-cutting cycle confidently shift towards the end of the year. Overall, the expectations favor the dollar.

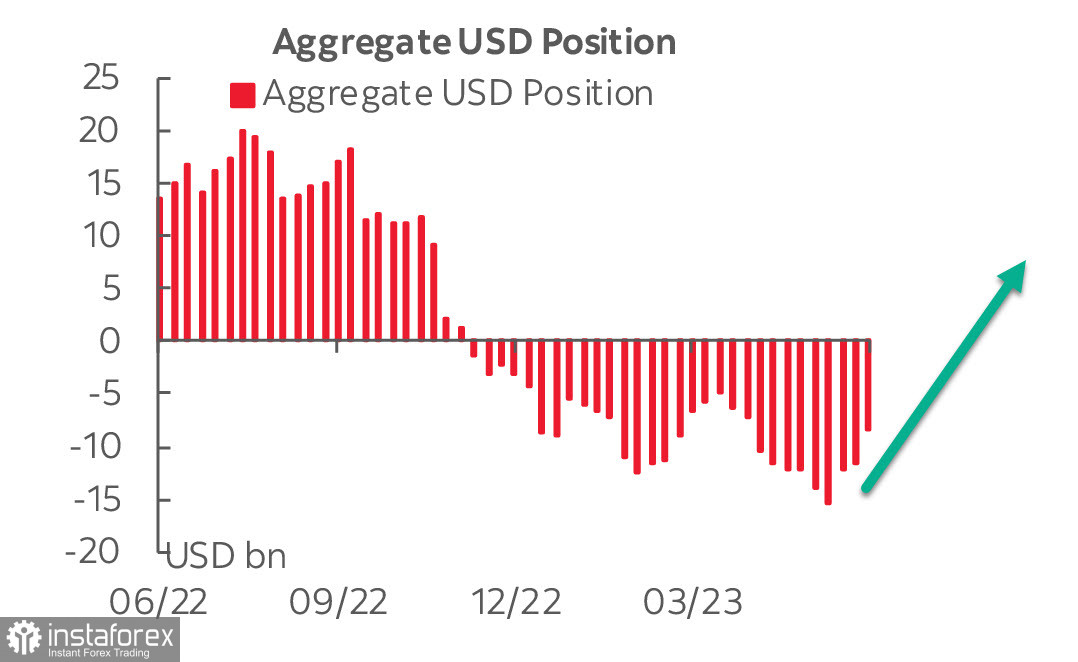

Bearish sentiment towards the US dollar has been declining for the third consecutive week. The aggregate short position has decreased by $3.5 billion to -$8.26 billion, marking the largest single change in favor of the dollar since the beginning of the year.

Take note that all major currencies have adjusted in favor of the dollar without exception. At the same time, the net position in gold has increased by $1.313 billion to $34.487 billion, which indirectly indicates both persistent inflationary expectations and the fact that risks for the global economy sliding into a global recession are still high.

Oil prices are declining, despite overall positive risk sentiment. It appears that Saudi Arabia's decision to reduce production by 1 million barrels per day did not help sustain oil prices at high levels, perhaps markets are now more focused on the ongoing sale of oil reserves.

Simultaneously, concerns about a slowdown in economic growth in China are growing, which could further pressure global demand. Goldman Sachs has revised its oil price forecasts downwards for the third time in six months.

EUR/USD

The ECB will hike its key interest rate by 25 basis points on June 15 (Thursday), which is already fully priced in by the markets. In addition, an announcement will be made regarding the end of reinvestments within the APP program from July. The meeting will also include new staff forecasts and commentary on monetary policy going forward.

As markets are now focused mainly on signs of lower inflation, there could be a strong reaction to a possible dovish signal from the ECB, which would lead to a sell-off in the euro, but a hawkish sounding central bank could be ignored.

At present, the rate forecast implies another 25 bps hike in July, meaning the final rate is expected to be 50 basis points higher than the current level of 3.25%.

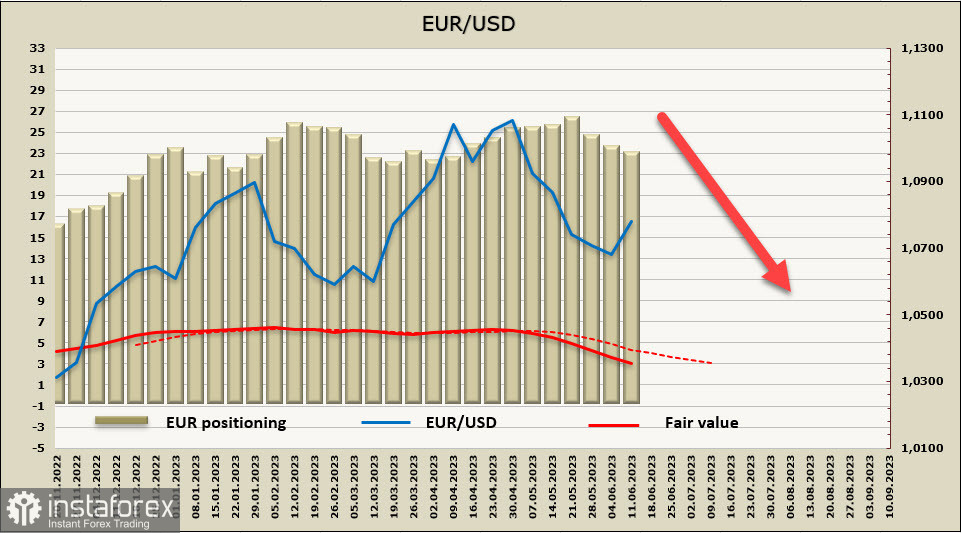

The net long position in EUR has decreased by $1.063 billion to $21.175 billion over the reporting week. The bullish bias is still high, but a reduction has been observed for the third consecutive week, with the calculated price moving further downward.

A week ago, we saw a high probability of further decline in EUR/USD. This forecast remains valid, and the recent local high at 1.0797 is considered a correction. We expect that bulls will encounter resistance near the technical level of 1.0810. If the ECB confirms its hawkish stance on Thursday, the corrective rally may generate another upward trajectory towards the resistance at 1.0865. However, take note that the long-term trend is bearish, and once bullish attempts have ended, a reversal to the downside is expected. The long-term target is still seen in the support zone of 1.0480/0520.

GBP/USD

The Bank of England will hold its next meeting next week, and the upcoming macroeconomic data in the following days can be crucial for its position.

The labor market report was just released, and despite the decline in the unemployment rate, the growth in average wages continues, at a higher pace than expected. The growth in average wages for the three months up to April reached 7.2% compared to the previous month's 6.8% (forecast 6.9%). The growth including bonuses also accelerated from 6.1% to 6.5%.

The report strengthens inflation expectations and increases the chances of a hawkish sounding BoE, which may be reflected in the Bank's inflation forecast to be published on Friday. Comments from BoE officials appear hawkish - Haskell supports further rate hikes, and Mann notes the persistent upward pressure on inflation. These comments have increased the yield of British bonds and reinforced expectations of further rate hikes. The futures market now sees the peak of the BoE's rate at 5.50% by the end of the year.

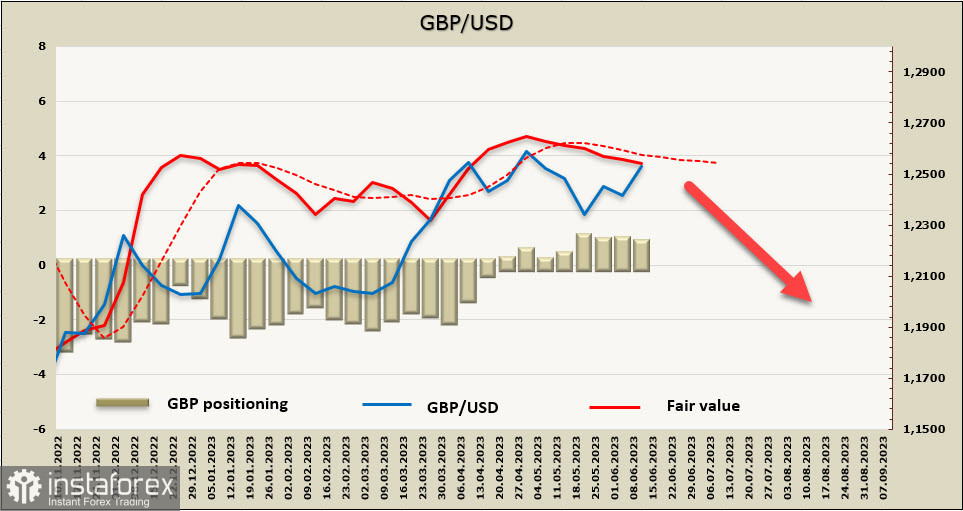

Thus, in the short-term perspective, the pound has the potential to strengthen slightly. However, investors are not rushing to make bets on the pound in the long run. The net long position in GBP has slightly decreased by £57 million to £969 million over the reporting week. The positioning is bullish, but the excess is insignificant. The calculated price is below the long-term average and is downward-directed.

Based on this, we continue to prioritize the bearish momentum, despite the pound's attempts to correct higher. We expect that the corrective rally will end below the local high of 1.2678, and any attempt to test it will be unsuccessful, leading to a reversal of GBP/USD to the downside. The nearest target is 1.2305, followed by 1.2240 and 1.2134.