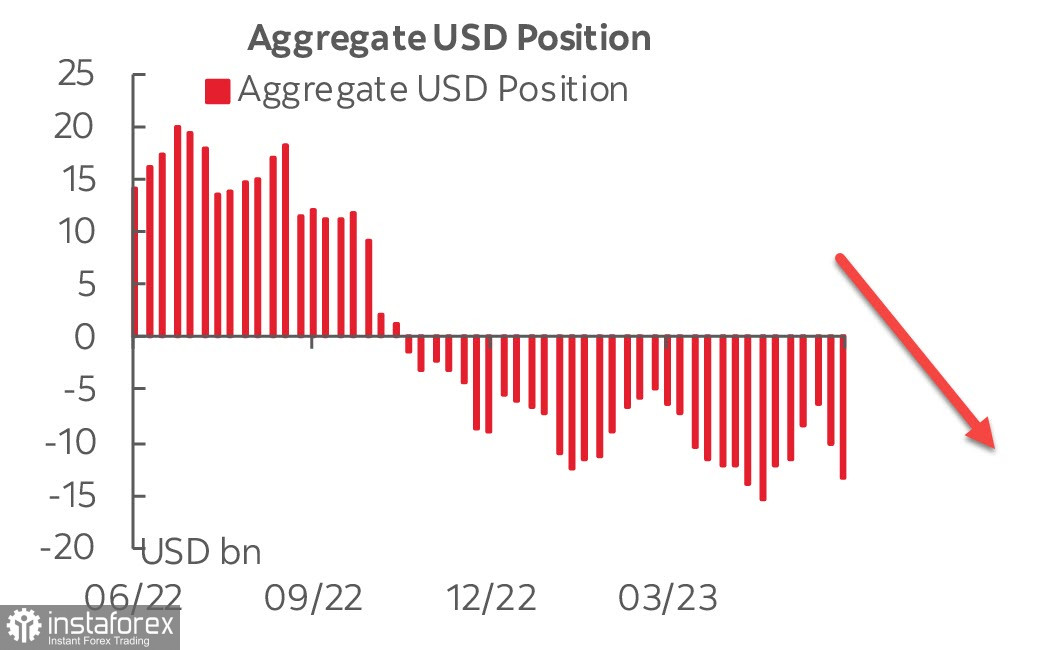

For the reporting week, the short position on the USD grew by $3.3 billion to -$13.5 billion. The growing demand for the dollar over the past two weeks has completely offset the net short position by a significant margin.

Most of the change in sentiment is reflected in the sharp decline in speculative traders' net short positions in the CAD (+$2.3 billion). Speculative accounts kept a bearish view on CAD for several weeks, but positioning finally acknowledged the recent improvement in the loonie's positions against the USD, with the weekly movement being the largest since 2017.

A week earlier, the pound had shown a similar sharp growth, now the Canadian dollar, and positioning for other currencies is close to last week's levels. It is also worth noting that all commodity currencies have turned positive, while the yen and gold have been sold off, suggesting an increase in risk appetite.

Data released on Friday showed a decrease in consumer spending in the US and a decline in inflation figures for May. Consumer spending fell to 0.1% m/m in May compared to 0.6% in April, with inflation-adjusted spending in May remaining unchanged. A downward revision for April and a weak May suggest that consumption in the US will slow significantly in the second quarter.

The overall PCE deflator only increased by 0.1% compared to 0.4% in April, which resulted in a fall in the annual rate to 3.8% compared to 4.3% previously. The annual figure for May was the first below 4% since the beginning of 2021. The core PCE was 0.32% m/m compared to 0.4% previously, leading to an annual rate of 4.6% compared to the expected 4.7%.

On Monday, the main focus was on the ISM Manufacturing Index. The main ISM data is expected to show a slight increase, to 47.2p from 46.9, extending the contraction of manufacturing activity in the US to eight months. The dollar looks weaker than in the middle of last week and is unlikely to strengthen before the holiday on Tuesday, so we should brace ourselves for another low-volatility day.

EUR/USD

Core inflation in the eurozone accelerated again in June, the consumer price index in the eurozone looks mixed: the overall index fell from 6.1% y/y to 5.5%, but the core index rose from 5.3% y/y to 5.4% (expected 5.5%). Bets on the European Central Bank's peak interest rate have barely changed at ~4%.

Expectations on the ECB rate have barely changed - two more quarter point hikes are expected, while the peak rate is about 4%. This is lower than the Federal Reserve's rate, plus industrial production in Europe is on a contraction trajectory, capital outflows across the ocean are growing, but the euro rate, contrary to many forecasts, remains quite high.

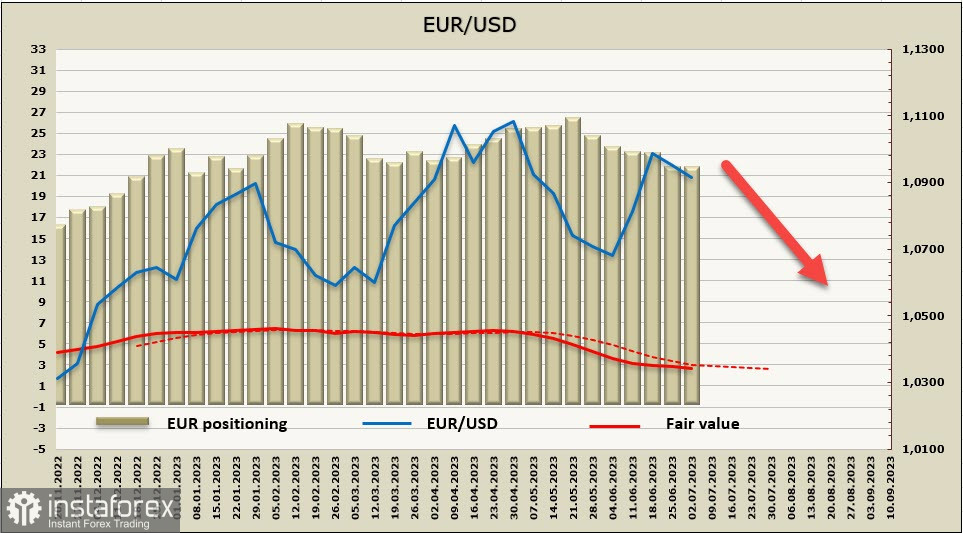

The net long position on the euro increased by $130 million for the reporting week, a small change, while positioning remains bullish. Nevertheless, the decline in the volume of long positions on the euro over the previous 5 weeks does not provide grounds to assume that the euro is in demand again. The calculated price is below the long-term average, a reversal has not yet formed.

As we mentioned in the previous review, trading is going sideways with a gradual shift to the downside. We expect this trend to continue, on track to 1.0700/20.

GBP/USD

Final UK GDP data for Q1 came out unchanged, showing +0.1% growth. Private consumption remained unchanged, government spending was revised downwards, which was offset by a revision of investments upwards. The total volume of business investments was revised upward for the quarter - from +0.7% to +3.3%.

The Manufacturing PMI in June was 46.5p, which is slightly better than in May, but manufacturing is still in contraction territory. There are no important macroeconomic news scheduled until the end of the week. The Bank of England rate forecast remains unchanged - a quarter point rate hike is expected at the meeting on August 3, which is fully factored into the current pound rate.

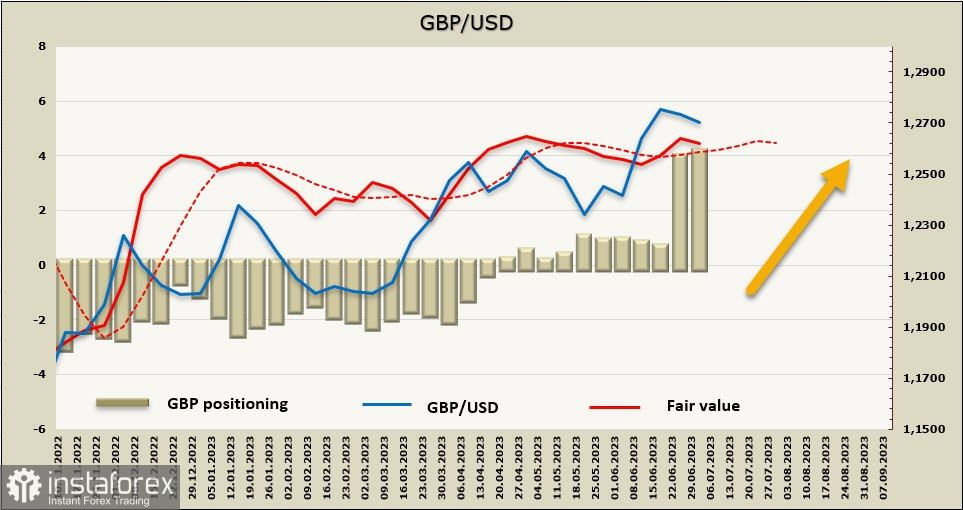

After last week's rapid growth of the net long position, the pound added $425 million, and the total long position reached $4.143 billion. The positioning is bullish, however, the estimated price has lost momentum, which may be a reason to believe that the main movement has already occurred and its strengthening in the coming week is unlikely.

The pound still tested the support level of 1.2678, and although it failed, the chances of climbing to 1.30 have become noticeably lower. There's a high probability of falling to the 1.2580/2620 range, but for now, we assume that this is a corrective decline and the pound will resume growth after a pause.