The European Central Bank will hold its meeting on Thursday, July 27. The Bank is set to raise interest rates by 25 basis points. There are no doubts about this, as ECB President Christine Lagarde announced additional tightening of monetary policy parameters last month. Therefore, the main focus will be on the ECB's stance. The key points of interest will be the wordings in the accompanying statement and verbal signals from the head of the ECB. The fact that there is a rate hike will likely be ignored by the market.

In recent weeks, ECB officials have expressed conflicting rhetoric. For instance, Lagarde has shifted the emphasis in her speeches several times, alternating between a hawkish and dovish tone. While she never questioned the July rate hike, her stance on the prospects of monetary tightening has varied. In one of her speeches, Lagarde stated that subsequent rate hikes are still uncertain. However, in her latest speech, her rhetoric has become somewhat stricter, stating that the ECB has "a lot of work ahead" to contain inflation, which remains at a persistently high level.

The other members of the ECB are divided into two camps: the hawkish and the dovish. For example, the head of Slovenia's central bank, Bostjan Vasle, stated that core inflation "remains high and persistent," thus monetary authorities "must continue tightening policy." Francois Villeroy de Galhau, the head of the Bank of France, also expressed concern about the high level of inflation, supporting further monetary tightening. His colleague from Germany, Joachim Nagel, stated that interest rates "must continue to rise," but added that it is "too early to say to what extent."

The hawkish scenario is supported by the minutes of the June ECB meeting. The text of the document suggests that the July rate hike (the ninth since last summer) will likely not be the last. The minutes indicate that the Governing Council may consider the possibility of raising interest rates "after July" if necessary.

The entire intrigue of the July meeting lies in the answer to one single question – is further monetary tightening necessary?

There is no unanimous opinion on this matter. On one hand, the case for further rate hikes is supported by core inflation, which remains at a high level (unlike overall inflation, which is slowing down at an active pace). It is worth noting that just last week, the core consumer price index for June was revised upwards. According to the initial estimate, the core CPI rose by 5.4% last month. However, according to the final calculations, the indicator was revised to 5.5%. ECB officials are particularly concerned with core inflation, hence this result is clearly in favor of the euro.

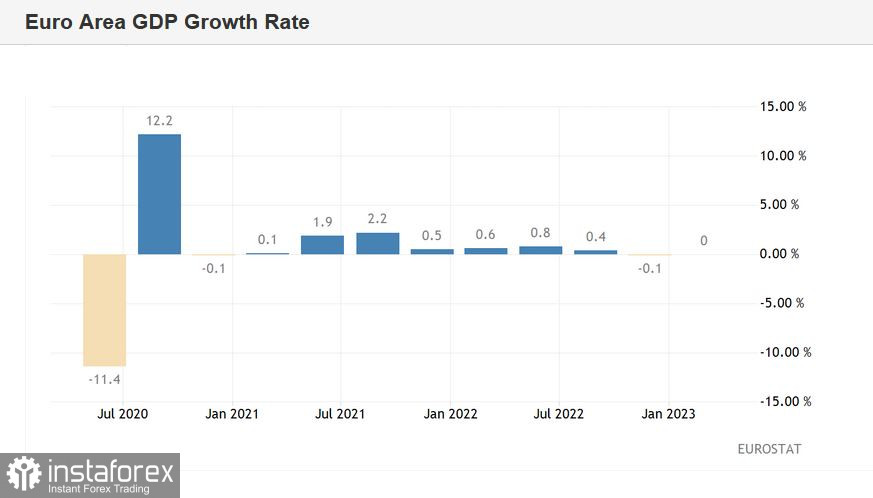

On the other hand, there is weak economic growth in the euro area. As a reminder, according to updated data, eurozone GDP remained unchanged in the first quarter compared to the previous three months. Although a technical recession was not confirmed (it was reported in June that the region's economy declined by 0.1% in the first quarter of 2023, the same as in the fourth quarter of 2022), such weak results do not contribute to a stronger aggressive stance.

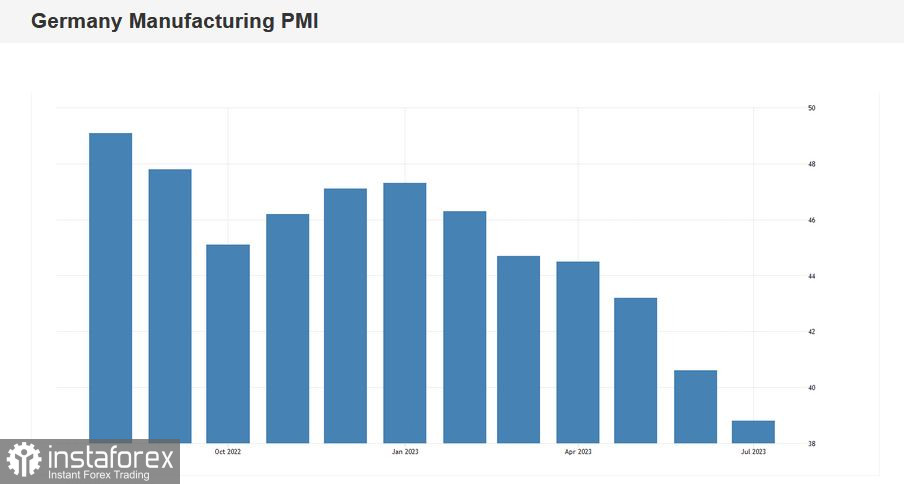

Disappointing data on PMI and IFO indices were published this week. In particular, Germany's manufacturing PMI plummeted to 38.8 points, the weakest result since May 2020 when the world was grappling with the coronavirus crisis. The index has remained below the key 50-point mark for 13 consecutive months and has been declining actively for the last three months. Meanwhile, the overall IFO business climate index in Germany dropped to 87.3 points this month (the weakest reading since October 2022) against the forecast of 88.0 (in June, the index was at 88.6). The index has been declining for the third consecutive month.

Such weak results could have an impact on the ECB's rhetoric, especially since not all members of the ECB have shown a hawkish stance lately. For example, the head of the Bank of Greece, Yannis Stournaras, recently stated that inflation is de facto declining, and further monetary tightening (after the July rate hike) "may harm the economy." His colleague, the head of the Bank of Italy, Ignazio Visco, voiced a similar position, adding that inflation may decrease "faster than projected," so "there is no need to push the situation into a recession" (by further raising rates).

Interestingly, even some former hawks have started to voice dovish signals. One such example is Klaas Knot, who surprised market participants with his recent stance. According to him, the rate hike after July "is not a final decision but a subject of discussion."

As we can see, there is no unanimous opinion among the ECB members regarding further prospects for monetary tightening. However, no one doubts that the central bank will raise rates by 25 basis points. As for the subsequent rhetoric, the intrigue remains.

In my subjective view, the ECB will leave the door open for further rate hikes but will emphasize that the current tightening cycle is nearing its end, and the next (possible) rate hike will be of an "extraordinary" nature – only if core inflation remains at its current level or accelerates. Such a thing will likely put pressure on the euro, as previously, Lagarde hinted quite transparently at maintaining a hawkish course even after the July meeting.