The main market news was the increase in United States Treasury (UST) yields, caused by the government's announcement of its intention to increase borrowings in Q3 to $1 trillion compared to the estimate of $733 billion three months ago. As Reuters notes, the U.S. Treasury expects that by the end of 2023, the balances in the Treasury General Account (TGA) will reach $750 billion, which is more than $100 billion higher than the consensus forecast, suggesting that the agency must plan for a deficit far exceeding the CBO estimate of $1.54 trillion.

This news led to the rise in UST yields, which in turn resulted in an increase in yields for most global bonds.

The ISM Manufacturing Index in the U.S. hardly changed, rising from 46 to 46.4 compared to the consensus forecast of 46.9. In July, the index decreased for the ninth consecutive month, indicating a further sharp decline in manufacturing activity. The employment subindex recorded the largest decrease among subindices, falling by 3.7 points to 44.4, the lowest level since July 2020. Manufacturing industry accounts for only about 9% of total wages, so this indicator will have a minor impact on overall employment, but the trend is clearly negative.

The rise in UST yields contributed to the strengthening of the dollar, and this situation is likely to continue until the end of the week.

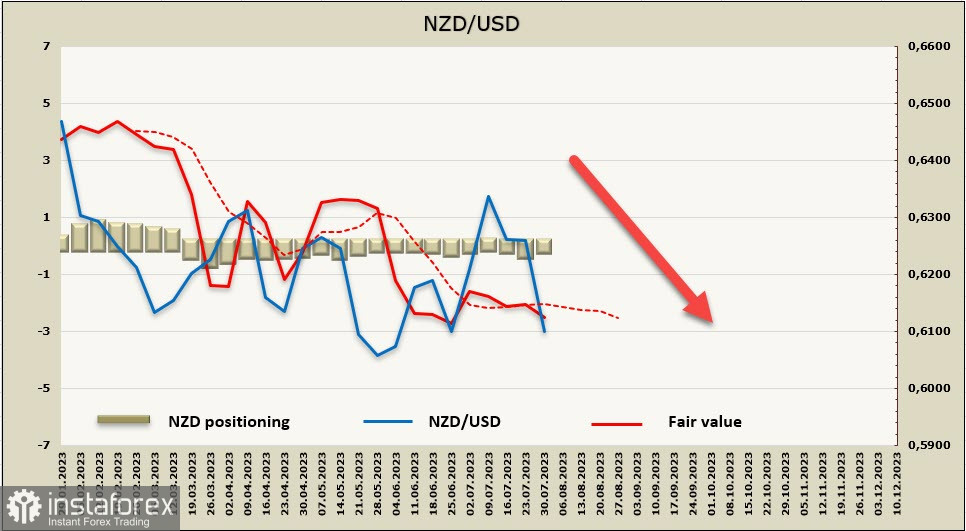

NZD/USD

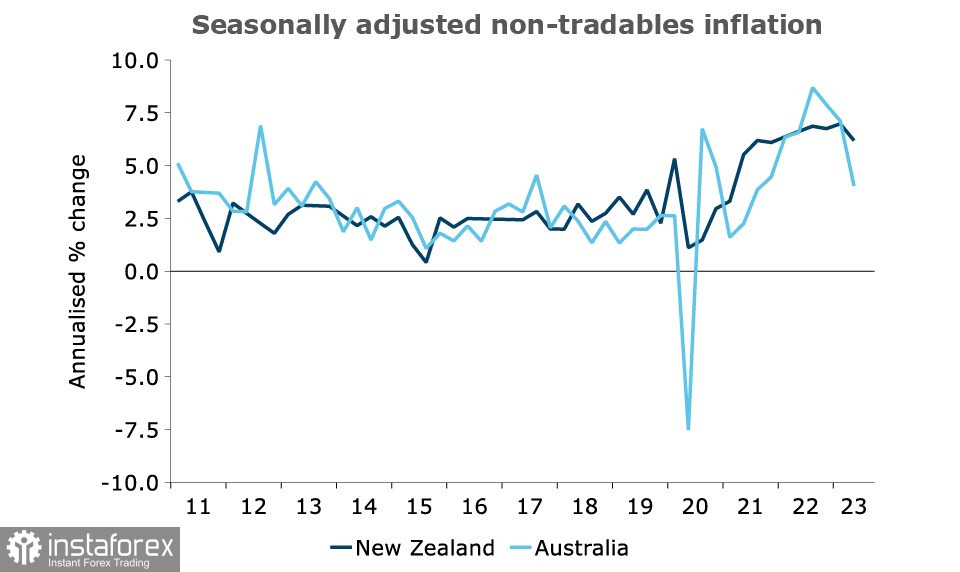

The quarterly growth of inflation for non-tradable goods in New Zealand remains at over 6.1% on an annual basis, taking into account seasonal factors. In Australia, this indicator has decreased to 4%, despite a much lower policy rate. Although at first glance, Australia's policy rate is much lower than New Zealand's, for inflation, what matters is how restrictive the interest rates are, and as practice shows, the task of slowing down inflation for the RBNZ appears to be much more challenging than for the RBA.

On Tuesday evening, labor market data for Q2 was published. Despite the fact that the labor cost index slowed down from 4.5% to 4.3% YoY, it still remains a very strong factor supporting internal inflation growth. In May, the RBNZ predicted that the unemployment rate would rise as quickly as during the global financial crisis, but in the 2nd quarter, it increased from 3.4% to 3.6% (forecasted at 3.5%), and the labor market as a whole still weakly responds to the measures taken by the RBNZ.

However, the labor market data does not support the view of a higher RBNZ rate, so the kiwi did not receive a driver for strengthening, and its decline may intensify.

The weekly change for NZD was +168 million, the overall imbalance is -59 million. The positioning remains neutral, the calculated price is below the long-term average and directed downwards.

In the previous review, we saw the target as the support zone 0.6110/30, and this target has been reached, with all indications for the kiwi to continue its decline. The nearest support is 0.6044, and the main target is 0.5870/5900.

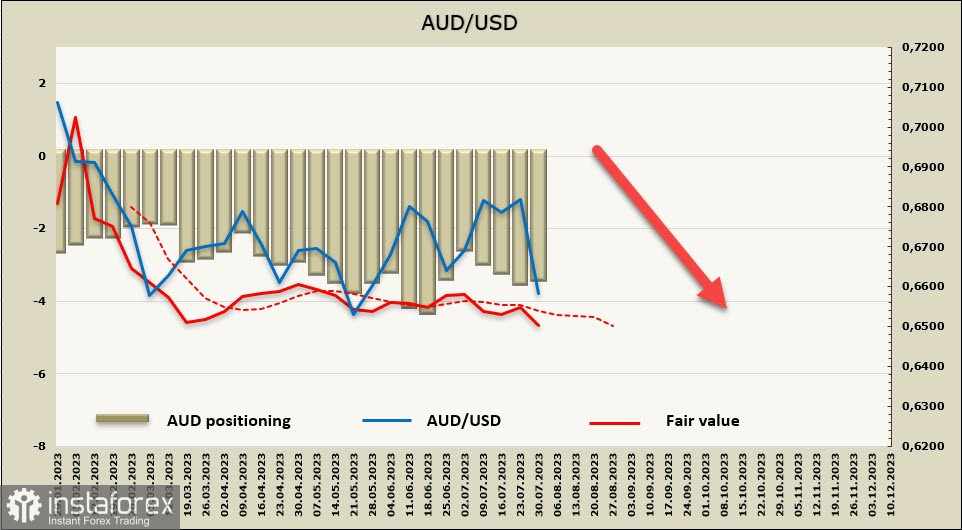

AUD/USD

The Australian dollar has experienced three significant blows this week, leading to massive sell-offs.

The Reserve Bank of Australia (RBA) kept the interest rate at 4.1%, while just last week, the markets were leaning towards another quarter-point increase. Expectations for the peak interest rate have decreased from 4.6% to 4.35%, meaning that the yield spread is not favoring the Aussie anymore, and now the markets anticipate only one more increase in the current cycle (presumably in November).

One of the reasons for the RBA's pause in the rate hike cycle is the slowdown in inflation. The index decreased from 7% to 6% in the second quarter, and the inflation forecast indicates a range of 2–3% by the end of 2025.

The fall of the Australian dollar was also influenced by the stronger U.S. dollar, which is strengthening across the entire currency market spectrum, as well as weaker-than-expected data from China. The Caixin manufacturing activity index dropped to a six-month low of 49.2 last month, indicating contraction in the sector due to a sharp decline in export demand. Housing sales in July also fell by 33.1%, marking the largest drop in a year. Yesterday, there was also a new round of promises from Chinese officials to support the economy, but the absence of commitments to budget spending makes the markets cautious: yesterday, the Chinese CSI 300 index fell by 0.4%, and the Chinese yuan declined by -0.49%.

The net short position on AUD increased by 45 million during the reporting week, reaching -3.478 billion. The positioning remains bearish, the calculated price is below the long-term average and is pointing downwards.

AUD/USD continues its decline, and the support at 0.6620/30, previously indicated as the target, has been reached. The probability of a further downward impulse appears high, with the target being the local low at 0.6460. For a more pronounced decline, an additional factor is needed, and if it appears, the next target will be the lower boundary of the channel at 0.6350/70.