As noted in the European Central Bank's Economic Bulletin published on Thursday, prospects for economic growth and inflation remain extremely uncertain in the Eurozone.

Among other key points, the following can be highlighted:

- Inflation continues to decline, but is expected to remain too high for a long time; and

- The Eurozone's near-term economic outlook has deteriorated, mainly due to weakening domestic demand.

From this report, it's evident that the ECB recognizes the complexity of the current economic situation, considering its slowdown, while "upward risks to inflation" persist, including "the potential resurgence of energy and food prices."

Earlier, ECB President Christine Lagarde also stated that the economic prospects of the Eurozone have worsened due to weakening domestic demand and high inflation.

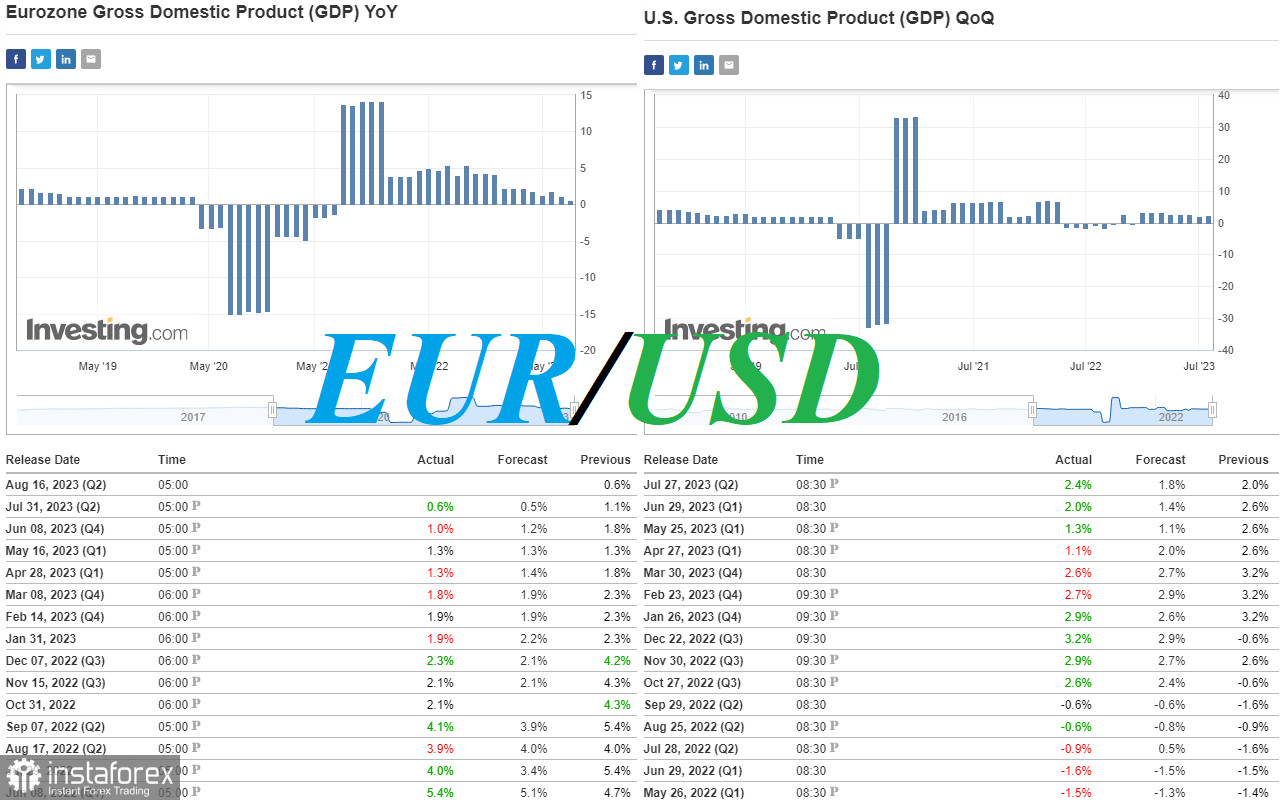

Next week, Eurostat will present a report with updated GDP data for the Eurozone for the 2nd quarter of 2023, as well as industrial production and inflation data for July.

GDP data, along with labor market and inflation figures, are key for a country's central bank in determining monetary policy parameters.

GDP growth indicates improved economic conditions, which, given corresponding inflation growth, can lead to monetary policy tightening. This, in turn, usually positively reflects on the quotes of the national currency.

The preliminary estimate of the Eurozone's GDP for the 2nd quarter was +0.3% (+0.6% year-on-year) after zero growth in the 4th quarter of 2022 and a decline of -0.1% in the 1st quarter of 2023.

Meanwhile, despite the emerging trend of decline, inflation in the region still remains significantly above the ECB's target level of 2% (previous annual CPI values: +5.3%, +5.5%, +6.1%, +6.1%, +7.0%, +6.9%, +8.5%, +8.6%, +9.2%, +10.1%, +10.6% in October 2022).

Many economists forecast a worsening of the negative dynamics of the European economy and a decrease in the Eurozone's GDP by 5.0% next year due to a prolonged course of tightening monetary conditions and rising energy costs.

Comparing with the corresponding U.S. GDP and inflation indicators, there's a clear advantage for the US. According to the latest data, in the 2nd quarter, the U.S. recorded an annual GDP growth of +2.4% (compared to a forecast of +1.8% growth after a +2.0% increase in the 1st quarter).

The economic slowdown and labor market cooling amid decelerating inflation might prompt the Fed leaders to start halting the cycle of monetary policy tightening.

However, not only did the GDP data confirm the reduced risks of the national economy entering a recession, but GDP growth might also provide the Fed with more time to maintain high interest rates, which will continue to exert downward pressure on inflation.

Today (at 12:30 GMT), fresh inflation data for the U.S. will be published .

We also discussed this in our previous reviews of EUR/USD: the growth of the U.S. economy is stronger than Europe's, and S&P500: correction or trend break?

The data suggests a slight increase in consumer price indices for July: an acceleration of the annual CPI from 3.0% to 3.3%, while the annual core CPI is expected to remain unchanged at 4.8%.

A resurgence of inflation in the U.S. could impact the Fed's decisions regarding monetary policy. After a July rate hike of 25 basis points, Fed leaders did not rule out the possibility of further monetary policy tightening this year.

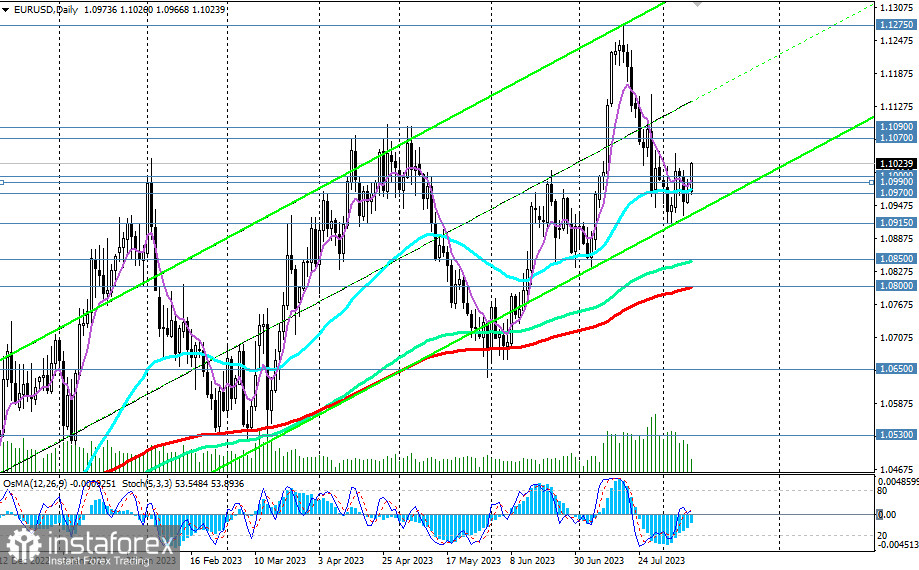

At the moment, the EUR/USD pair is showing an upward medium-term dynamic, having attempted to break through the long-term bullish market zone last month.

Meanwhile, economists believe that if economic data from the Eurozone doesn't begin to support the euro,, and relative expectations regarding the policies of the Fed and ECB do not change in favor of the euro this month, then a reversal and return of the EUR/USD to a downward trend can be expected by September.

From a technical perspective, this will appear as a breakout of the key medium-term support levels at 1.0850 and 1.0800.

In any case, today at 12:30 (GMT), a sharp increase in volatility is expected in the dollar quotes and, consequently, in the EUR/USD pair. But that won't be the end of it: on Friday at 12:30 (GMT), the U.S. Bureau of Labor Statistics will release new input on inflation. At this time, data on producer inflation will be presented. Previous Producer Price Index (PPI) values: +0.1% (+0.1% YoY), -0.3% (+1.1% YoY), +0.2% (+2.3% YoY), -0.5% (+2.7% YoY), -0.1% (+4.6% YoY), +0.7% (+6.0% YoY), -0.5% (+6.2% YoY), +0.3% (+7.4% YoY).

The data indicates a weakening of inflation pressure, which will impact the Federal Reserve's subsequent decisions regarding monetary policy tightening.

For July, a new increase in indicators is expected (+0.2% and +0.7% in annual terms). If the data is confirmed or turns out to be above forecasted values, the dollar is likely to strengthen again, including against the euro.