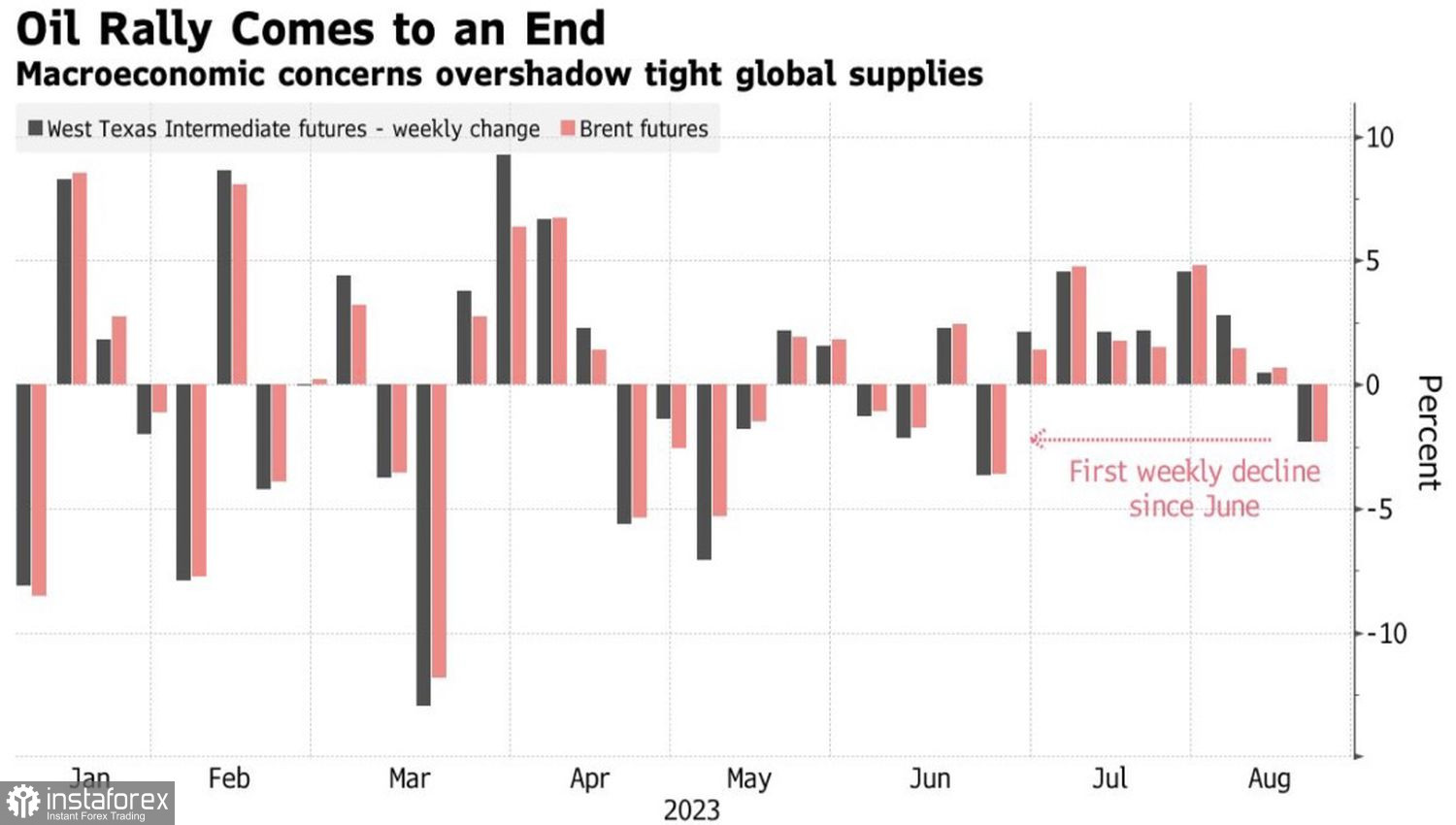

It is impossible to grow indefinitely. After a 7-week rally, oil prices finally took a step back. Waning demand again took its toll on the oil market as its slowdown spoked off the bulls. A series of disappointing macroeconomic data from China assured the central bank to cut interest rates. However, rate cuts were not as aggressive as investors had expected. Beijing is worried about the weakening of the yuan, the market is concerned about insufficient monetary stimulus. As a result, Brent goes into a pullback.

Weely dynamic of benchmark oil grades

The desire of Saudi Arabia and Russia to raise prices by reducing oil output rates and exports encouraged a rapid rally in the North Sea benchmark grade in July-August. However, as the summer is coming to an end, investors realize that this bullish driver was largely priced in futures. At the same time, Tehran's intention to resume oil exports by 450,000 barrels per day through the northern Turkish-Iraqi pipeline smooths out the decline in OPEC+ oil production.

At the same time, concerns about Asian demand are growing. It's not just China that is causing fear. Imports of Russian oil to India fell in July for the first time in 9 months, while supplies from Saudi Arabia collapsed to the lowest level in the last 2.5 years. Such dynamics of oil shipments accompanied by economic woes in China raise doubts about the feasibility of the recent IEA forecast of record global demand for crude oil in 2023.

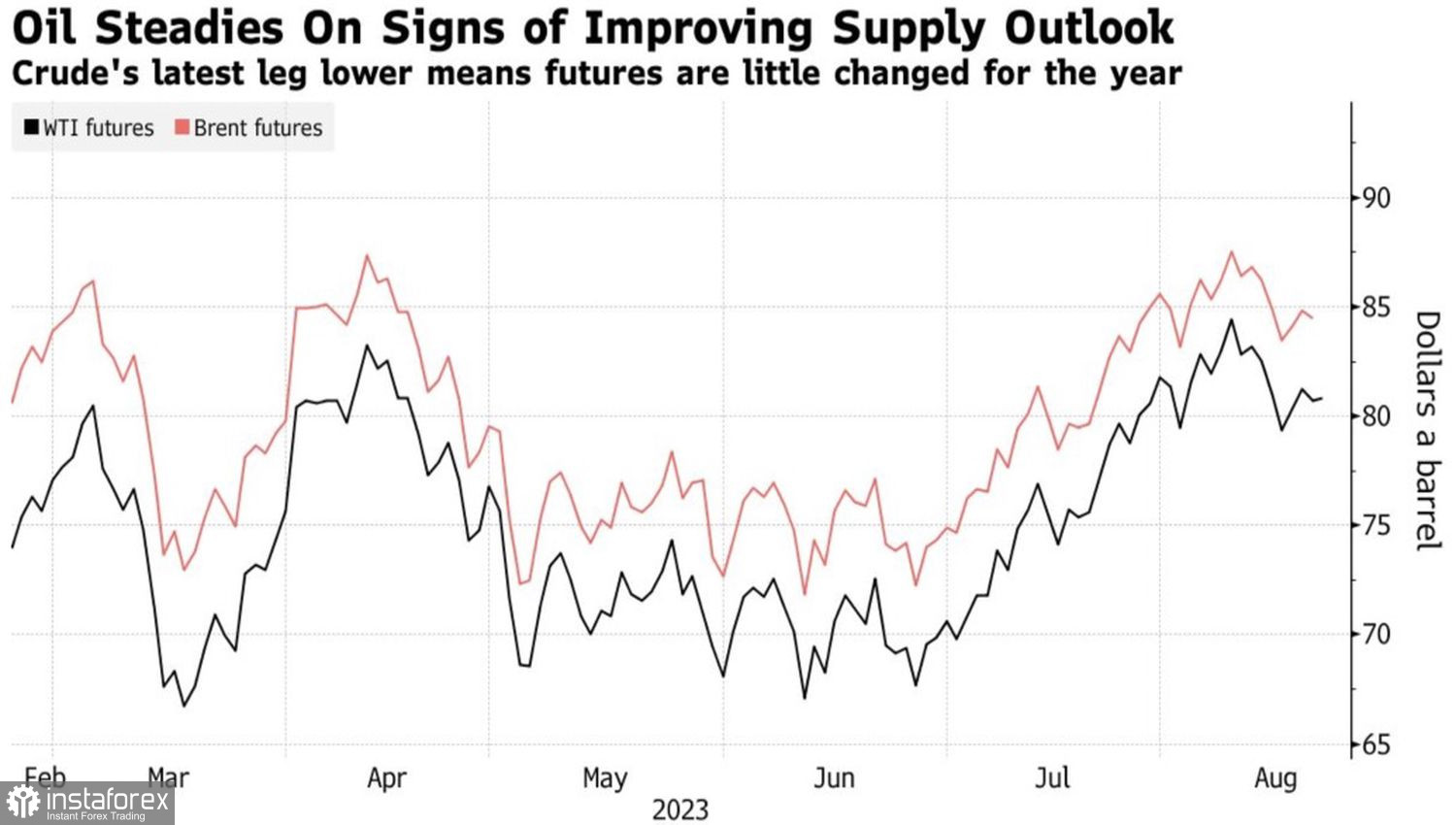

Brent and WTI dynamics

No less disturbing news comes from the US where the Federal Reserve intends to keep the federal funds rate at a plateau of 5.5%, at least until March 2024, or even raise it even higher. Treasury yields are skyrocketing and hit their highest levels in more than 10 years. The US dollar is also on a strong footing. If investors raise concerns not only about the Chinese-Indian, but also the American demand for crude oil, this will be certainly bearish for oil prices. Brent crude risks going into a downward spiral.

Yet, in my opinion, it is premature to predict a change in the uptrend for the North Sea benchmark. A forward-looking indicator from the Atlanta Fed signals that US GDP will grow by 5.8% in the third quarter. This would be the best result in the last 20 years, with the exception of the recovery period after the pandemic. The US economy remains firmly on a sound footing. With a slowdown in inflation from 9.1% to 3.2%, this revives the risk-on mood for US stocks. The growth of stock indices will be perceived as an improvement in global risk appetite, which will support oil prices.

I suppose that Beijing's stimulus measures will sooner or later bear fruit. The European economy has proven its ability to avoid a recession. Therefore, the bulls are betting on the uptrend in oil prices.

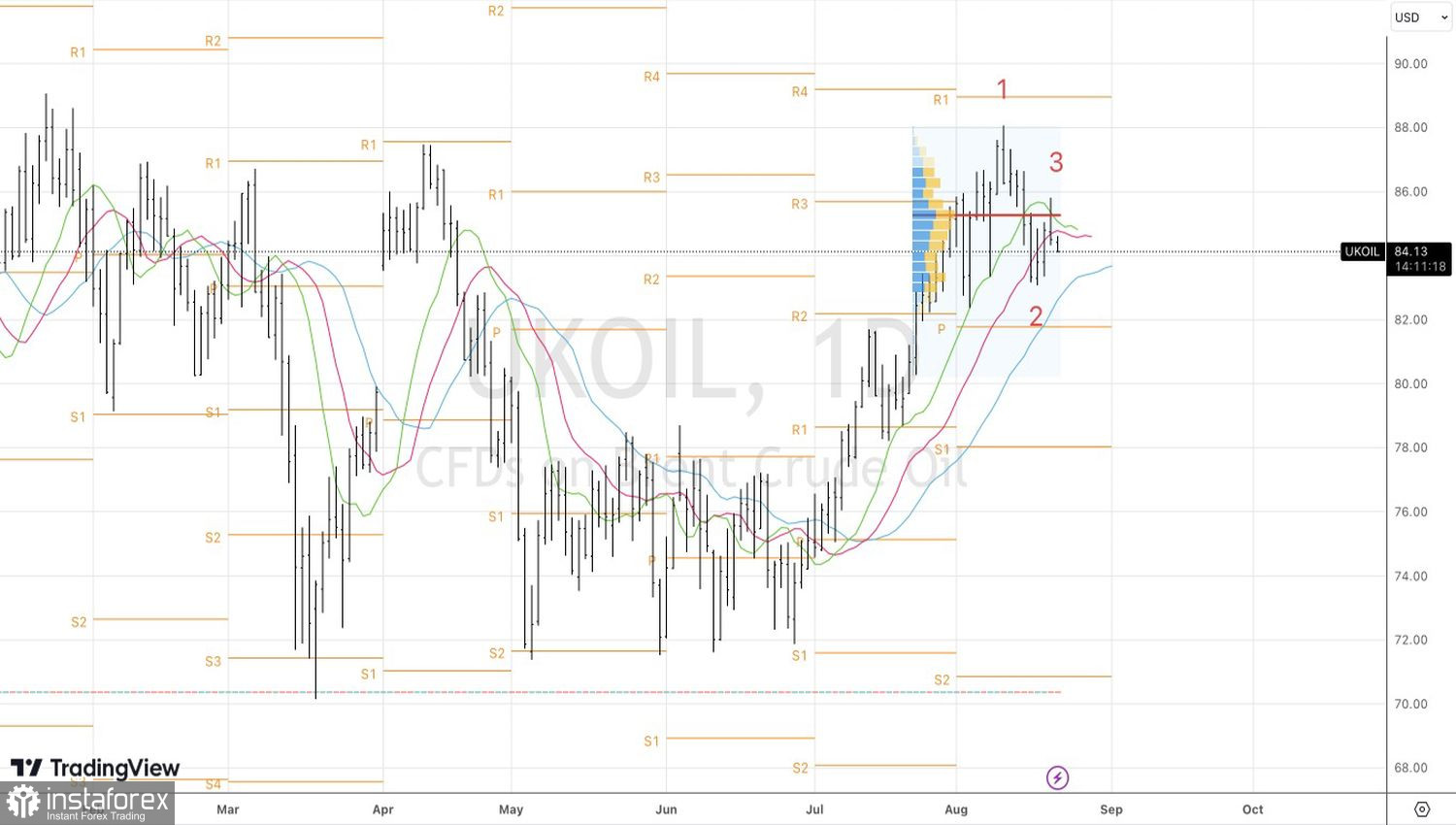

Technically, a downside pullback on the Brent daily chart started due to the implementation of the ABC pattern and the pin bar. We focus on short-term sell positions with downward targets at $84, $83.1, and $82.1 per barrel. The downward move will be followed by a reversal on the rebound from these pivot levels. Later on, traders will open medium-term buy positions.