The Bank of England intends to take the 15th step in tightening its monetary policy by raising the repo rate by 25 basis points to 5.5%. This opinion is shared by 64 out of 65 experts polled by Reuters. The futures market also holds the same view, with a 75% probability of an increase in borrowing costs at the BoE meeting on September 21st. However, recent comments from officials suggest otherwise. What will the Central Bank actually do? And how will GBP/USD react to its verdict?

According to Chief Economist Huw Pill, the Bank of England has two options. They can either continue to raise rates and then sharply lower them, as the markets expect, or keep borrowing costs at a plateau for an extended period. Personally, he would prefer the second approach. BoE Governor Andrew Bailey and his deputy, Sir Jon Cunliffe, believe that the repo rate is nearing the peak of the cycle. Bank of England policymaker Swati Dhingra's opinion is that the tightening of monetary policy has been too rapid, so there is a risk that the BoE has overdone it.

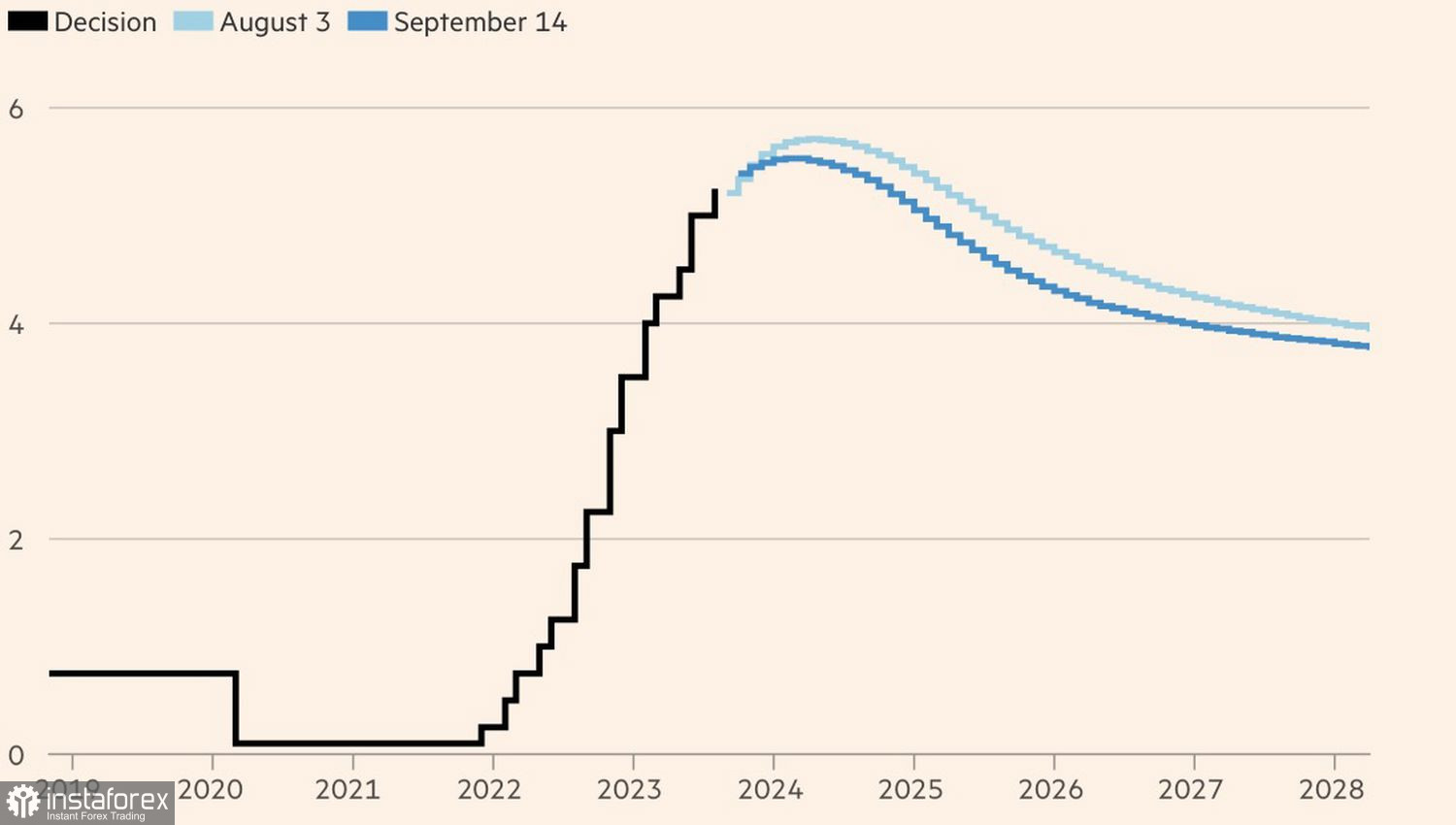

Indeed, the 14 steps taken by the Central Bank make the current cycle of monetary restraint the fourth most aggressive in history. Previous cycles occurred in the 1970s and 1980s and ended in recessions. Given the cooling of the labor market, the GDP contraction in July, and the deterioration of other macroeconomic indicators, everything is heading towards a downturn now. The threat of a recession is what is causing officials at the Bank of England to shift from decisiveness to caution. The change in the BoE's outlook is one of the drivers of the GBP/USD peak.

Dynamics of market expectations for the repo rate

Market expectations for the repo rate have indeed been falling rapidly since the middle of summer. Back then, the futures market predicted that borrowing costs in Britain could rise above 6%, making the pound the top choice among G10 currencies. However, since then, the chances have been rapidly declining. And now the forecast of a peak repo rate of 5.75% looks highly doubtful. If only the Bank of England had the courage to raise it to 5.5%.

The baseline scenario is the 15th step in the path of monetary restraint with a hint of the end of its cycle. However, the bad example of the ECB, which essentially did the same thing and weakened the euro in the process, could influence Bailey and his colleagues. According to Bloomberg experts, inflation in the United Kingdom accelerated to 7% in August, and the pound's devaluation could further drive up consumer prices, especially since wages continue to rise at record rates despite the cooling labor market.

The Bank of England is facing a challenging situation, and the storm in GBP/USD seems inevitable. Increased volatility in the pair could occur sooner rather than later, especially after the release of fresh inflation figures for August.

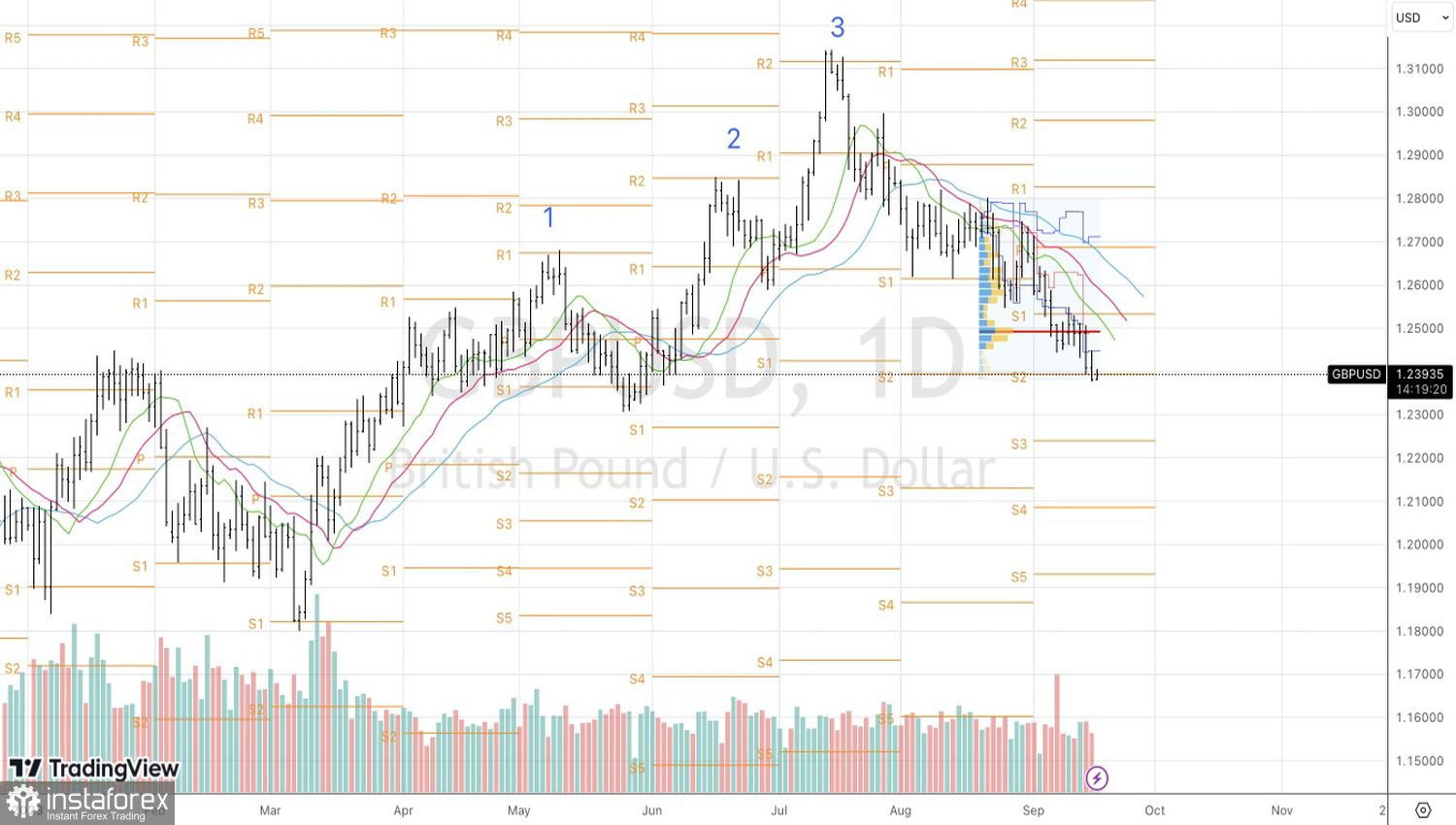

Technically, on the daily chart, GBP/USD is in a stable downward trend, confirmed by its distance from dynamic resistance in the form of moving averages. The inability of the bulls to break through the pivot level at 1.239 will be a sign of their weakness and a reason to sell the pound towards $1.224 and $1.21. Otherwise, we will form shorts on the analyzed pair on rise with subsequent rebounds from resistance at 1.2475 and 1.2500.