The U.S. dollar strengthened against nearly every other major currency as U.S. Treasury Yields rise. Federal Reserve representative Neel Kashkari said that he expects another rate hike this year, which bolstered bullish sentiment for the dollar, and the greenback risks rising even higher.

On Wednesday, the main focus was on the report on durable goods orders in the United States. This is considered an important report as it provides an assessment of both consumer demand and the state of the industrial sector. Regarding the latter, the data is quite contradictory, as regional industrial indices show opposite dynamics. For instance, the Richmond Fed Manufacturing Activity index increased from -7 in August to 5 in September, significantly exceeding forecasts, while the Dallas Fed Index declined from -17.2 to -18.1, and the Philadelphia Fed Index plummeted from +12 to -13.5.

Towards the end of the week, the U.S. will release several important reports so volatility may gradually increase. Market participants will keep an eye on the third revision of Gross Domestic Product for the second quarter, the US weekly Jobless Claims report due on Thursday. On Friday, the Core Personal Consumption Expenditure (PCE) Price Index will be in the spotlight. Market participants will be adjusting their expectations regarding the Fed's interest rate, but in any case, the US dollar is still the market favorite.

USD/CAD

There were two factors behind the Canadian dollar appreciation last week: stronger-than-expected inflation data, increasing the chances of further rate hikes by the Bank of Canada, and rising oil prices, which attracted more investors wanting to buy Canadian stocks and led to higher demand for the loonie.

Currently, money markets see a 93% chance for a quarter point rate hike from the Bank of Canada in January. However, if the upcoming inflation report, to be published on October 17th, shows stable inflation once again, the decision to raise rates could be made at the nearest meeting on October 25th. The market is taking this possibility into account, which is narrowing spreads between Canadian and U.S. bonds, contributing to increased interest in CAD.

Due to this week's light economic calendar, volatility stoking news will come from the United States.

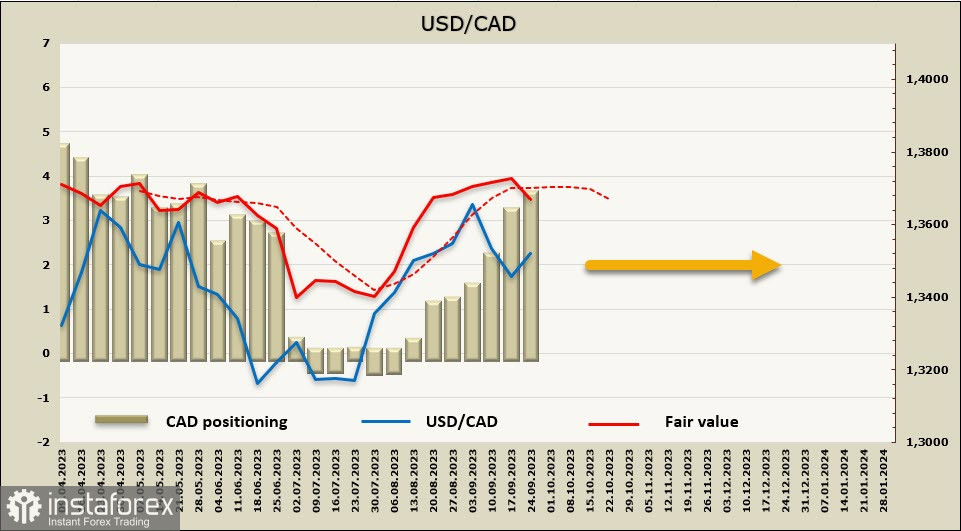

The net short CAD position increased by 481 million to -3.571 billion during the reporting week, indicating firm bearish speculative positioning. The price is trying to turn downwards, as one of the factors, namely the state of the stock markets, has shifted in favor of Canada. There are several reasons for this, but none of them appear to be long-term, so a bearish reversal is not yet an obvious scenario.

CFTC reports indicate that investors have turned increasingly bearish on the CAD, which is a long-term factor, while the current market conditions favor longs in the CAD in the short term. It remains unclear as to which of these trends will prevail as the market needs new data. For now, it is best to assume that the lower band at 1.3320/40 could be tested if short-term factors continue to develop. The upper band of the range is at 1.3660/90, and there is currently a low chance of breaking out of this range.

USD/JPY

The Bank of Japan kept its yield curve control unchanged, as widely expected. The policy interest rate is held at -0.1%, and the 10-year JGB yield was kept at around 0%. It is allowed to fluctuate in a range of around plus and minus 0.50% and an upper limit at 1.0%.

The USD/JPY pair rose after Bank of Japan Governor Kazuo Ueda's press conference. Ueda did not say anything to support the idea that policy changes might occur at the next meeting on October 31st. He mentioned that Japan is not in a situation where the central bank can see the country reaching its inflation target, and the distance to ending negative rates hasn't changed significantly. He reiterated that the BOJ is prioritizing the risk of taking premature measures.

The market drew an obvious conclusion from Ueda's words - as long as everything is working, the Bank won't make any changes. While there are factors in favor of exiting Yield Curve Control (YCC), the greater concern is ruining something with premature steps.

The minutes of the BOJ's July meeting showed that many members agreed the central bank must keep interest rates ultra-low for now, while one member thinks an assessment of reaching the target can be made in the first quarter of 2024. In other words, the first quarter will only involve an assessment of the target, with no mention of any concrete steps.

Therefore, it should be assumed that the BoJ will not take any action in the foreseeable future. This is clearly a dovish stance that negates hints that were made earlier, and as a result, the situation reverts to what it was before - the yen is under pressure and gradually weakening in anticipation of new data.

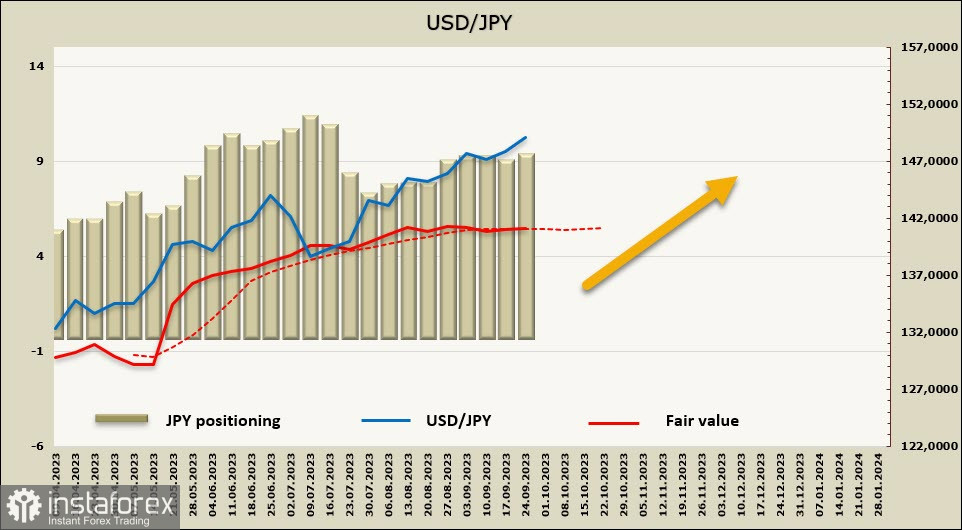

The net short JPY position increased by another 201 million to -8.59 billion during the reporting week. Speculative positioning remains bearish, but the price has lost momentum and currently lacks direction.

The weak movement is due to the dollar's dominance in this pair, which is overshadowed by the stability of the Japanese stock market, which looks much better than the U.S. stock market. However, this situation may not last long. At the moment, the pair is trading near the upper band of the bullish channel, and the chances of further rising towards the 151.91 peak still appear higher than a deep correction. Unless the BOJ clearly signals readiness for active measures, the pair is unlikely to experience a significant downward move, except perhaps through currency interventions.