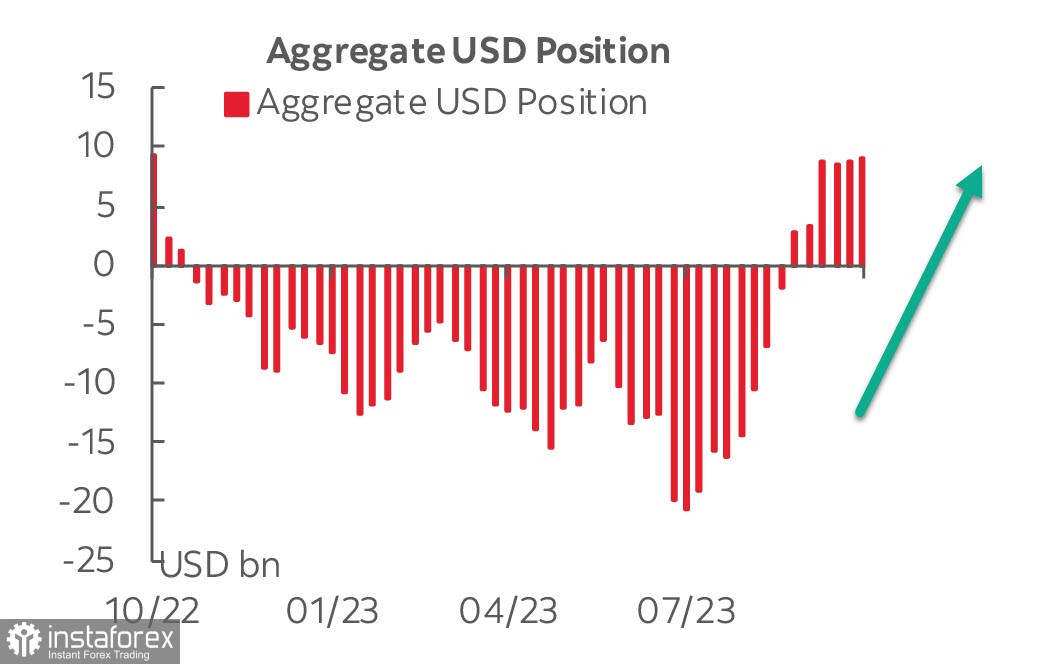

The CFTC report showed minor changes in speculative positioning across major world currencies. The net USD long position has remained stable for the fourth consecutive week and increased by 376 million to 9.084 billion during the reporting period, which is the highest level in a year.

Gold rates have significantly surged. If the net long position grew by 8.4 billion the previous week, it increased by 7.76 billion to 29.4 billion during the reporting week, which implies further price growth. The Swiss franc and the yen also have a slightly bullish bias, indicating increased demand for safe-haven assets.

High yields have remained a key driving force in financial markets for an extended period. The yield on the 10-year US Treasury bonds is trading around 5%, putting pressure on stock markets and the yen, as the contrast with Japan's low-yield regime becomes even more pronounced.

The main event of the week is the US employment report for October. On Wednesday, in addition to the expected FOMC meeting, we can look forward to the ISM report on manufacturing activity. It's quite possible that the report will further increase the contrast between the US and other countries, giving the dollar a new impetus to strengthen.

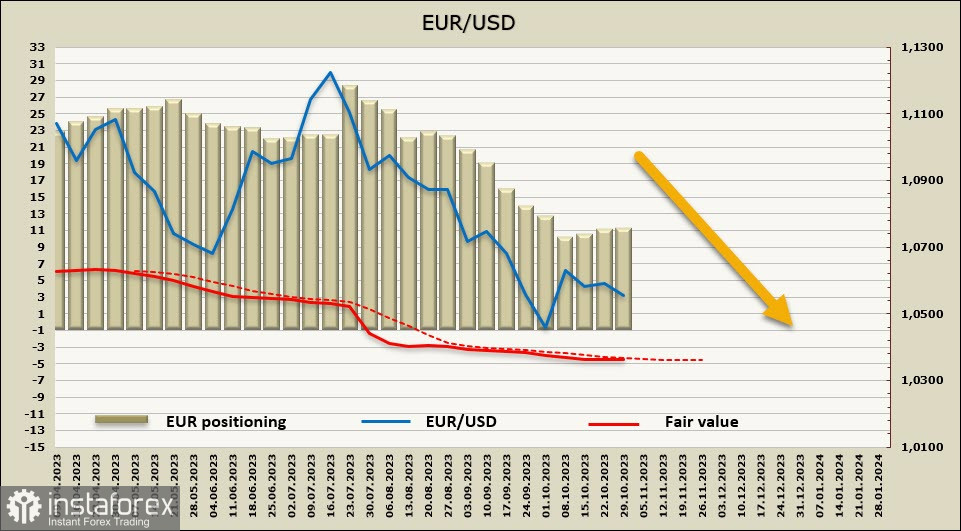

EUR/USD

On Tuesday, Eurostat will publish a flash estimate of inflation data for October, with an expected slowdown in the core inflation rate from 4.5% to 4.2%. If there are no significant deviations from these forecasts, the euro may lose one of the factors that had supported it.

The European Central Bank kept interest rates unchanged for the first time since June of last year and indicated that they will put an end to additional rate hikes. ECB President Christine Lagarde suggested that the recent meeting was more about summarizing what had been done previously rather than revising future plans.

The net long EUR position slightly increased, adding 390 million in the past week to reach 11.285 billion. It's worth noting that the euro sell-off has stopped, and the price is at a standstill.

EUR/USD continues to be in a corrective mode after the significant decline in July-September. The downward momentum has weakened, and there's a good chance of a more pronounced correction. The ECB has already signaled that there will be no further interest rate hikes, and unless the situation with energy commodities significantly deteriorates, the corrective phase could soon come to an end. A rebound above the local high of 1.0695 does not have a high probability, and the pair could still move towards the technical level of 1.0760 (38% retracement from the drop), but the chances of this happening has not sharply increased either. Meanwhile, the bearish bias remains intact, and once the corrective phase ends, if the level at 1.0695 holds, another significant bearish wave is possible.

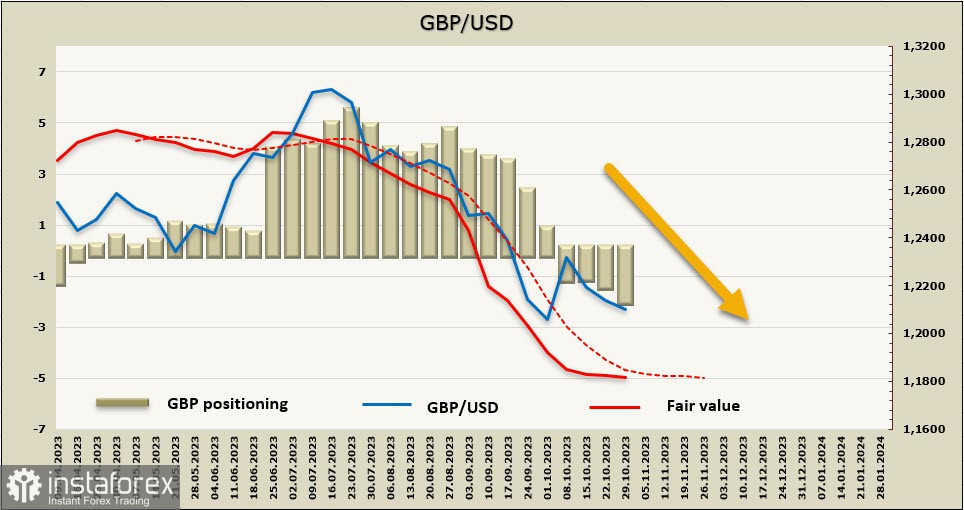

GBP/USD

On Thursday, November 2, the Bank of England will hold its monetary policy meeting. It is expected that the key interest rate will remain unchanged at 5.25%, but the decision may not be unanimous.

There are few reasons for the BoE to reconsider its position. Wage growth in August was weaker than expected and generally showed signs of slowing down, which aligns with the REC and KPMG report, which, as noted by the BoE, "tends to lead to changes in official annual wage growth figures."

Although the monthly GDP for August largely met expectations at 0.2% m/m and 0.3% in the three-month average, growth is likely to be below the BoE's third-quarter forecast. Similarly, retail sales in September remain weak, excluding automotive fuel, they are at -1.0% m/m (-1.2% y/y). September inflation in the UK was slightly higher than expected. PMIs in September and October remain in contraction territory, all below 50, signaling grim growth prospects.

Since inflation in the third quarter averaged 6.7%, which is slightly below the BoE's forecast of 6.9%, in the context of very weak economic growth, the probability of a rate hike has become even lower in the past month. As a result, the bulls have no grounds to expect the pound to strengthen against the dollar.

The net short GBP position increased by 563 million to -1.416 billion during the reporting week, indicating a bearish bias. The price is below the long-term average, but the momentum for further decline is weak.

The pound cannot find a strong reason for a full correction, and from a technical perspective, after completing the consolidation, a breakdown of the support level at 1.2029 appears more likely than an upward movement to the upper band of the sideways range at 1.2337. It is expected that another upward retracement will not exceed the resistance zone of 1.2190/2210, followed by another attempt to break below the support level at 1.2029 and a move towards the target of 1.1800. The pound appears weaker than the euro, so the EUR/GBP cross is likely to continue rising.