The Durable Goods Report revealed a significant decrease in new orders for manufactured durable goods, which fell by 5.4% in October, with a 6.7% decline excluding the defense sector. This indicates both a slowdown in demand and overall industrial activity.

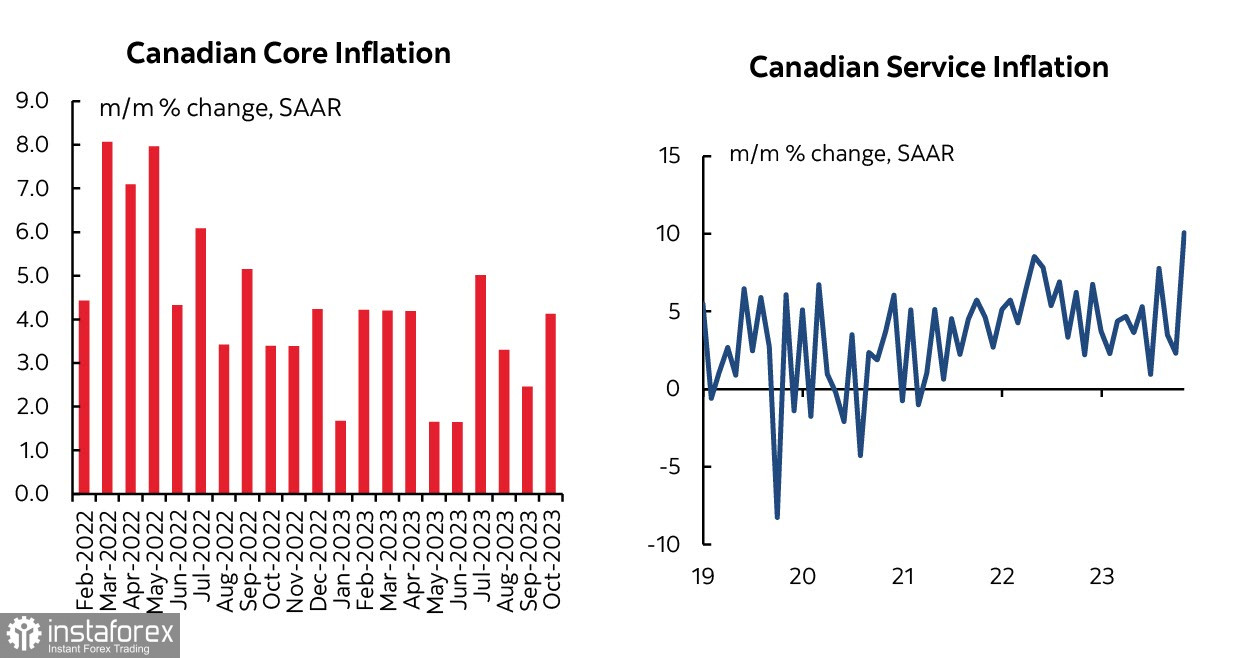

The only thing that is consistently growing is services inflation, as noted by representatives of several central banks in their statements. In particular, European Central Bank President Christine Lagarde not only highlighted the rapid growth in wages and service prices but also expressed the opinion that overall inflation will accelerate again in the near future. Bank of England Governor Andrew Bailey, speaking in Parliament, stated that inflationary risks remain on the rise. In Canada, the inflation report showed a strong increase in service prices in October, and Bank of Canada Governor Tiff Macklem is likely to address this issue in his speech.

On Thursday, banks in the United States will be closed for Thanksgiving, so volatility is expected to be low.

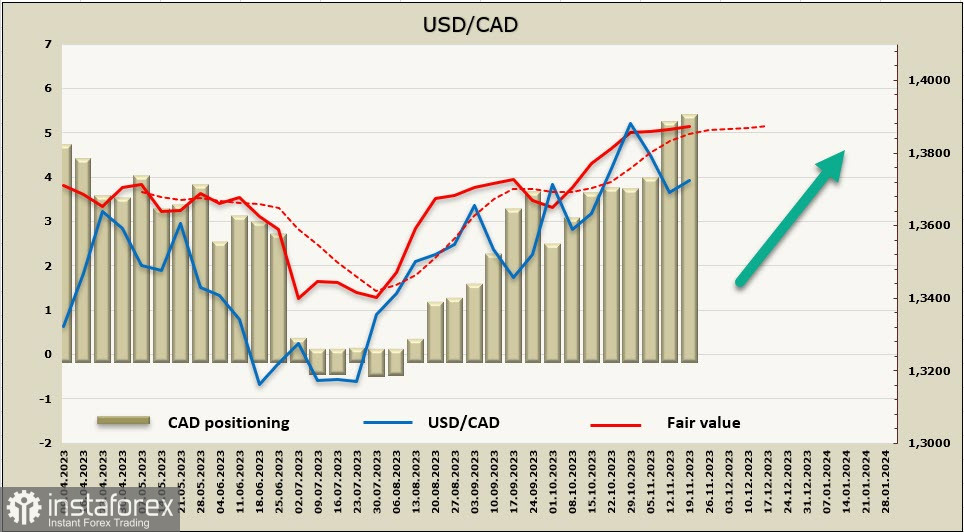

USD/CAD:

Consumer inflation grew by 3.1% on a year-over-year (YoY) basis in October, compared to a 3.8% gain in September, which, at first glance, seems like a positive signal for the Bank of Canada. However, it's not that simple.

The slowdown in inflation is largely due to a decrease in gasoline prices (-7.8%), driven not so much by cheaper gasoline but by base effects – a year ago, gasoline prices sharply increased by 9.2% after OPEC+ announced production cuts. Without this factor, inflation in October would have been 3.6%, not much different from September.

It's also worth noting that alongside the decline in goods prices, service prices are rising at an accelerating pace (+4.6% in October compared to +3.9% in September). Monthly growth was +10.1%, the highest since July 2018. The rise in service prices is explained by the rapid increase in average wages amid declining labor productivity. Basic inflation in October is higher than a year ago.

The Bank of Canada is still dealing with persistent problems, as the economy is clearly slowing at a rapid pace, and inflation targets are still far away. The rate in October remained unchanged at 5%, with the next meeting on December 6. Given the recent changes, the likelihood of another quarter point rate hike has increased. In this case, the loonie could either stay at its current levels or strengthen against the greenback, but in the long term, it is unlikely to benefit from forecasts shifting in a hawkish direction, as the Canadian economy is slowing noticeably faster than the U.S. economy.

The net short CAD position increased by 222 million to -5.142 million over the reporting week, with positioning confidently bearish. The price is above the long-term average, the momentum is weak, but it is upward.

USD/CAD is consolidating, and it will most likely break above the range. The nearest resistance is at 1.3780/3800, then 1.3840/50, with the main target at 1.3897, a breakthrough of which could accelerate the movement. Support is provided by the trendline at 1.3680/90, and traders could consider long positions if the price declines to this area.

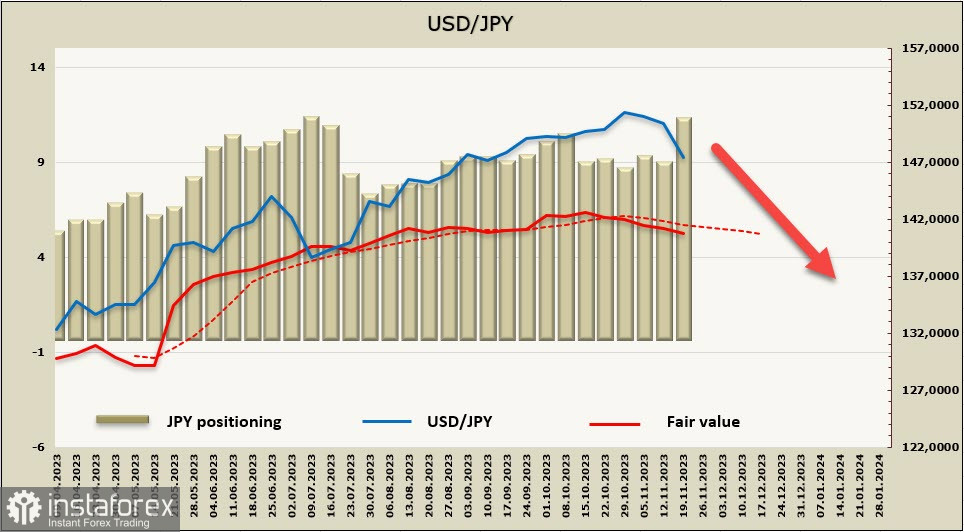

USD/JPY:

The first preliminary estimates of Japan's GDP for July-September, published last week, showed an unexpectedly sharp contraction: real GDP fell by 0.5% on a quarterly basis (2.1% YoY), marking the first decline in three quarters. Some government officials commented on the figures, noting that domestic demand, both in terms of business investments and consumer spending, is decreasing or even "in free fall."

The decline in demand breeds pessimism regarding expectations that the Bank of Japan will start to exit its negative interest rate policy. If such pessimism solidifies, the yen is likely to start falling again.

Analysts at Mizuho Bank do not share this stance, and their arguments are as follows. Firstly, the government will reduce income taxes across the board and carry out cash giveaways as part of its new stimulus package. Secondly, wage negotiations are expected to lead to an increase in wages. Both of these factors will support both demand and internal inflation in one way or another. Therefore, the BOJ may well begin to adjust its credit and monetary policy without fearing long-term consequences. If the market is confident that the BOJ will stick to its chosen strategy, it will perceive the slowdown in demand as a temporary phenomenon. Thus, the yen may continue to strengthen against the backdrop of narrowing negative yield differentials.

The net short JPY position sharply increased by 2.18 billion to -10.827 billion. However, the price is still below the long-term average and is pointing downward.

A week earlier, we saw an increasing probability of a bearish pullback, and this trend is confirmed. The previously indicated target of 146.10/40 remains relevant. Under current conditions, the pair is unlikely to rise towards the local peak of 151.96.