Well, that's it. The market has failed in its attempt to go against the Federal Reserve. Investors have tried six times to induce the central bank to make a dovish turn in the current cycle of monetary tightening, but they have failed each time. It seemed that the seventh attempt would be successful; expectations of a Fed rate cut were rising too quickly. And here's another disappointment, both for the stock markets and the EUR/USD pair.

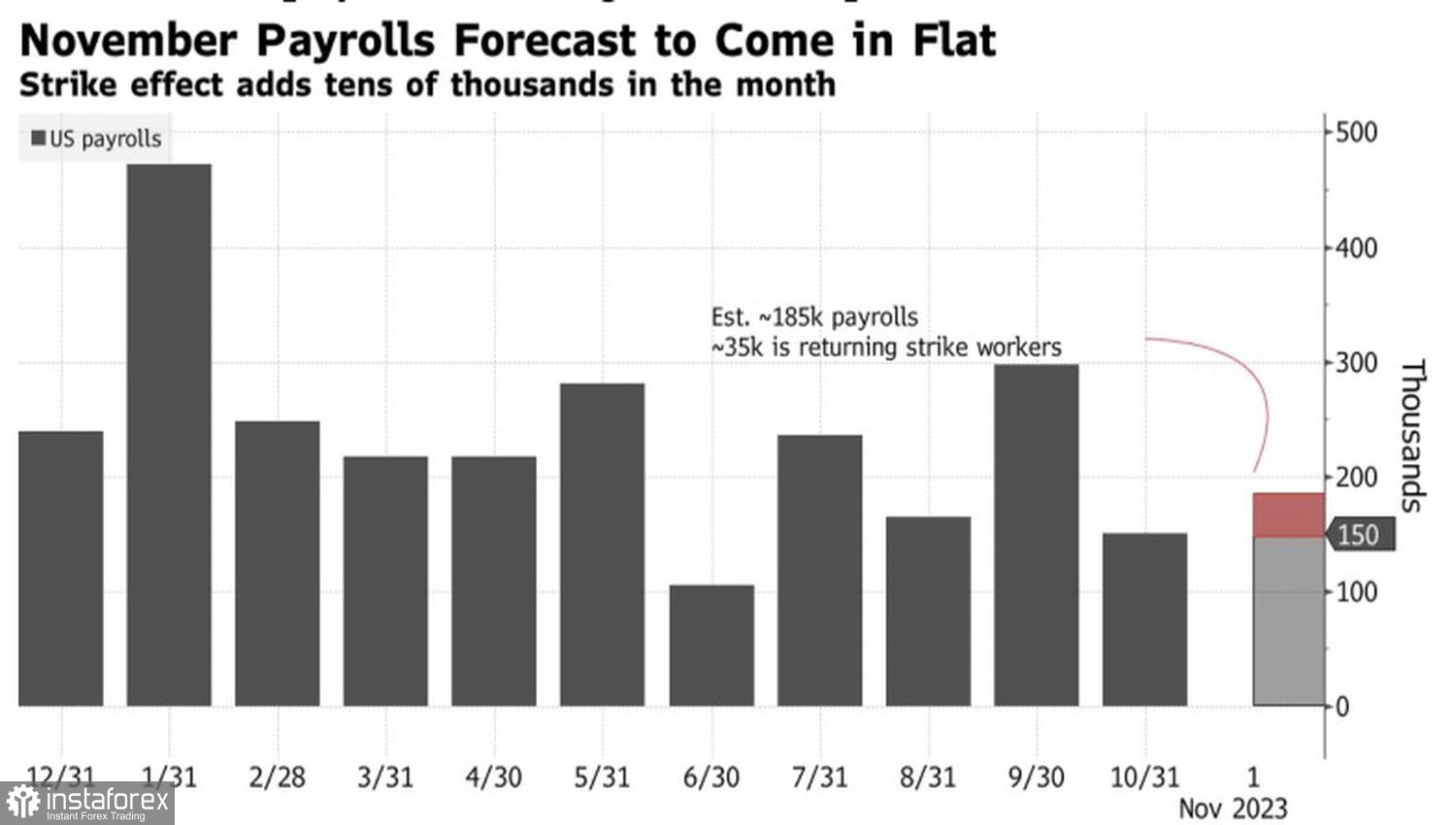

The 199,000 increase in employment turned out to be better than expected by Bloomberg experts. A positive surprise for the U.S. dollar was the decline in the unemployment rate to 3.7% and the acceleration of wages to 0.4% month-on-month. The labor market is far from cooling down. If so, there is no reason to expect a rapid spike in inflation to the 2% target. The Fed will be forced to keep the rate at 5.5% for a long time. Market illusions have once again shattered against reality. For the seventh time in a row.

Dynamics of employment in the Non-Farm Sector of the U.S.

Strong employment data for November have reduced the chances of the Fed easing monetary policy in March from 70% to less than 50%. Investors are forced to adjust their expectations for the start of the monetary easing cycle to May. If inflation in November does not slow down, derivatives will return to June-July. That is precisely where the November rally of the S&P 500 began and the Treasury bond yields fell. These processes created a favorable background for EUR/USD bulls. Unfortunately, buyers were unable to take full advantage of it.

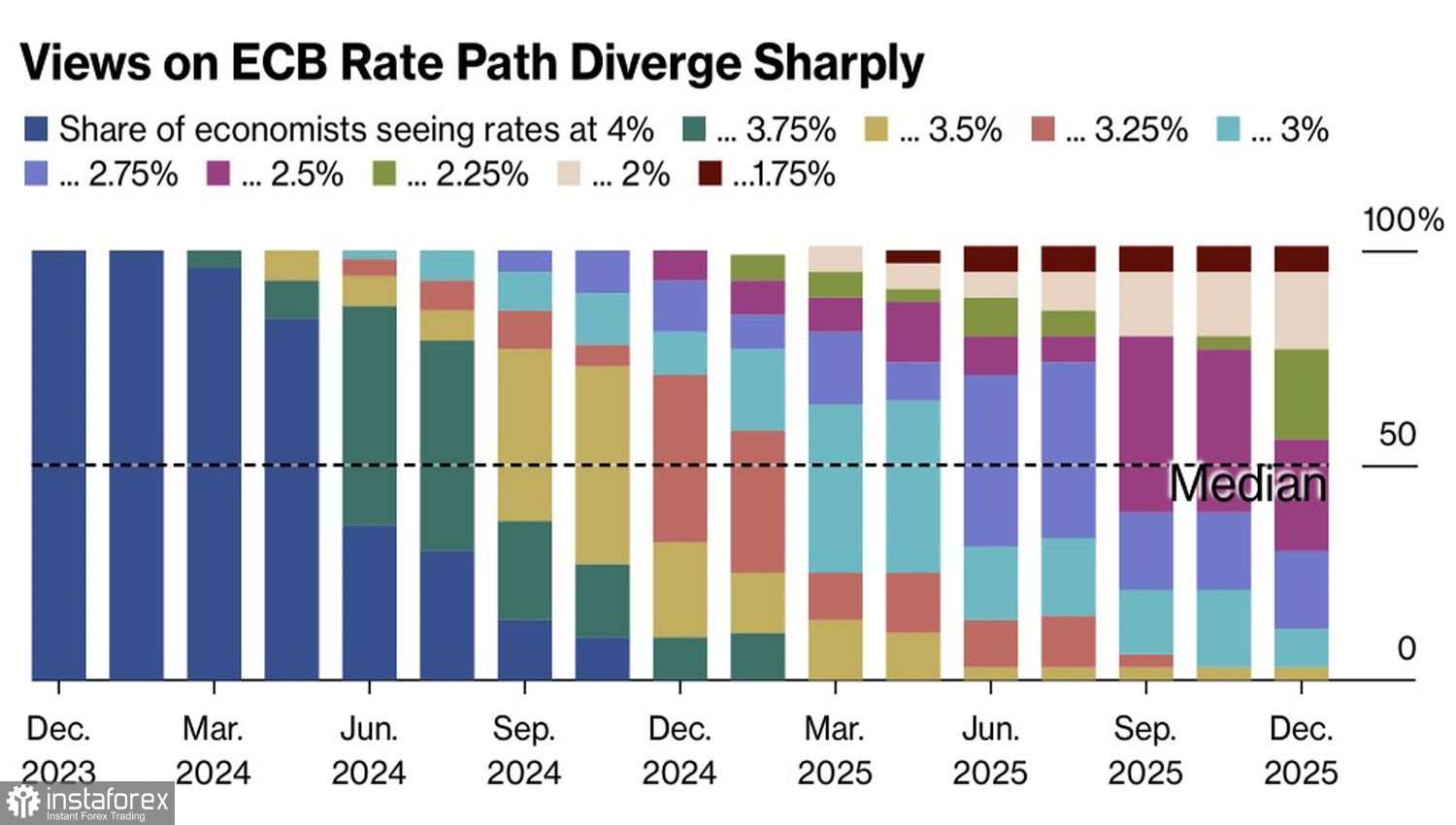

The main reason is investors' faith that the European Central Bank would start trimming rates before the Fed does. The futures market predicts a 150 bps drop in the deposit rate to 2.5% in 2024, and Bank of France Governor Francois Villeroy de Galhau agrees with it. According to the Governing Council official, at some point next year, it will be necessary to consider reducing borrowing costs.

Bloomberg experts believe that the string of rate cuts will not be as fast as the markets expect. They see only three rate cuts for the deposit rate in 2024, each by 25 bps: in June, September, and December. In theory, this is good news for the euro. However, if central banks, led by the Fed and the ECB, do not aggressively ease monetary policy, stock markets will fall, global risk appetite will decrease, and EUR/USD will go down.

Forecasts for changes in the ECB deposit rate

The euro's stability in response to strong US employment data for November is nothing more than the market's reluctance to give way to fear. However, ahead in the economic calendar are the scheduled releases of US inflation data and the Fed's meeting, and the central bank will find reasons to trigger a correction in the S&P 500 and accelerate the euro's decline.

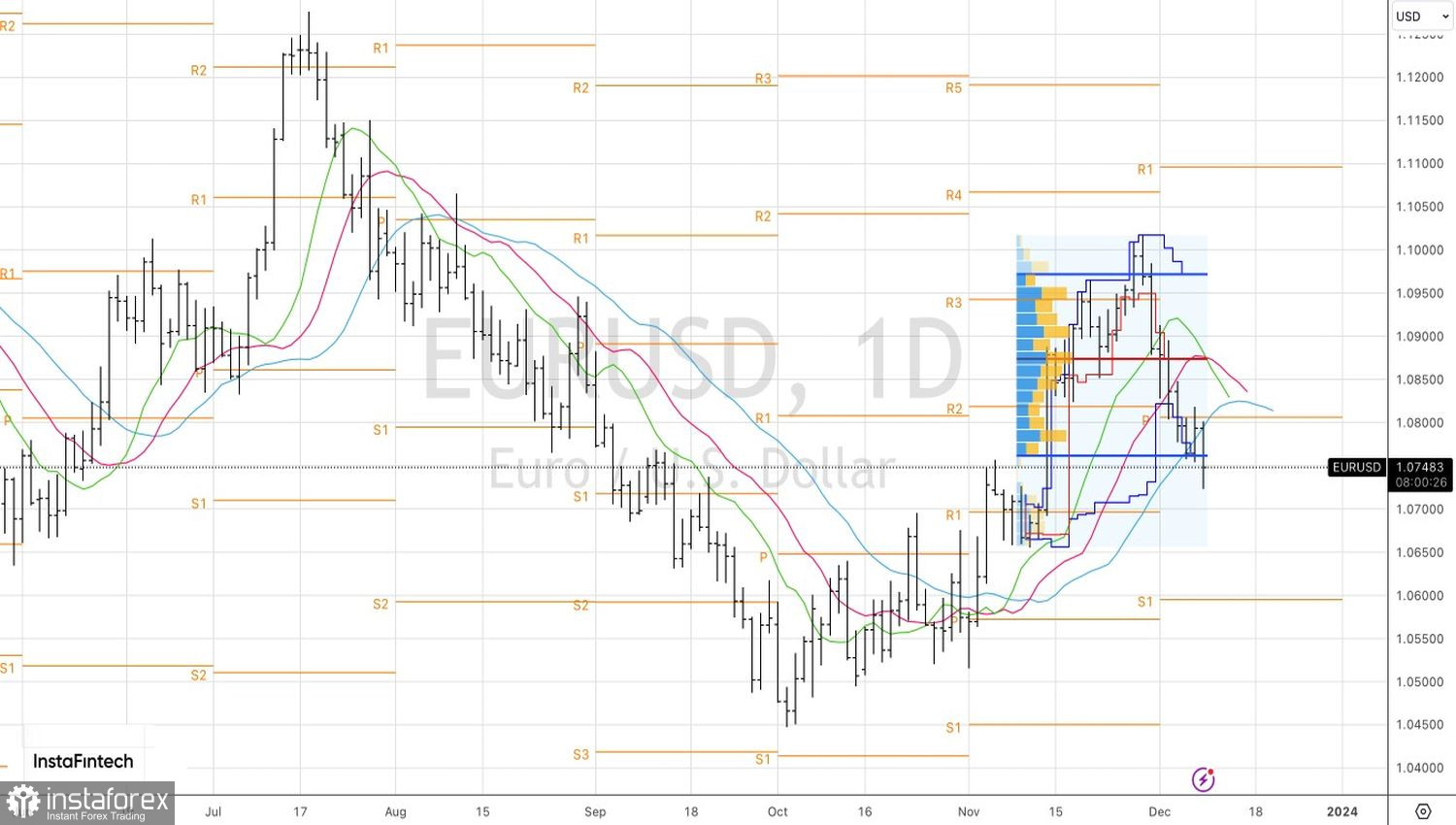

Technically, the fate of EUR/USD will depend on the weekly close. The inability to return to the fair value range of 1.076-1.097 is a clear sign of bull weakness and a reason to build up shorts formed from 1.094. The targets are set at 1.07 and 1.065.