Since December 2022, EUR/USD has been trading in the range of 1.05-1.10. According to Goldman Sachs, breaking out of this range is problematic. Without divergence in monetary policy or alignment of economic cycles in the U.S. and the Eurozone, it seems unlikely. Both of these events seem improbable, given the substantial disparity in productivity. Additionally, the geopolitical risks associated with the territorial position of the currency bloc are unfavorable. The United States continues to benefit primarily due to its geographical distance.

As winter approached its end, there was an expectation that the bulls for EUR/USD would regain momentum. European PMI data surpassed expectations, China's substantial rate cut brought satisfaction, and statistics from China fueled optimism. Additionally, considering the robustness of the U.S. economy and the euro's success as a pro-cyclical currency, a rally seemed plausible. However, continuous confirmations are essential for the rally's sustained momentum, and unfortunately, they have not materialized.

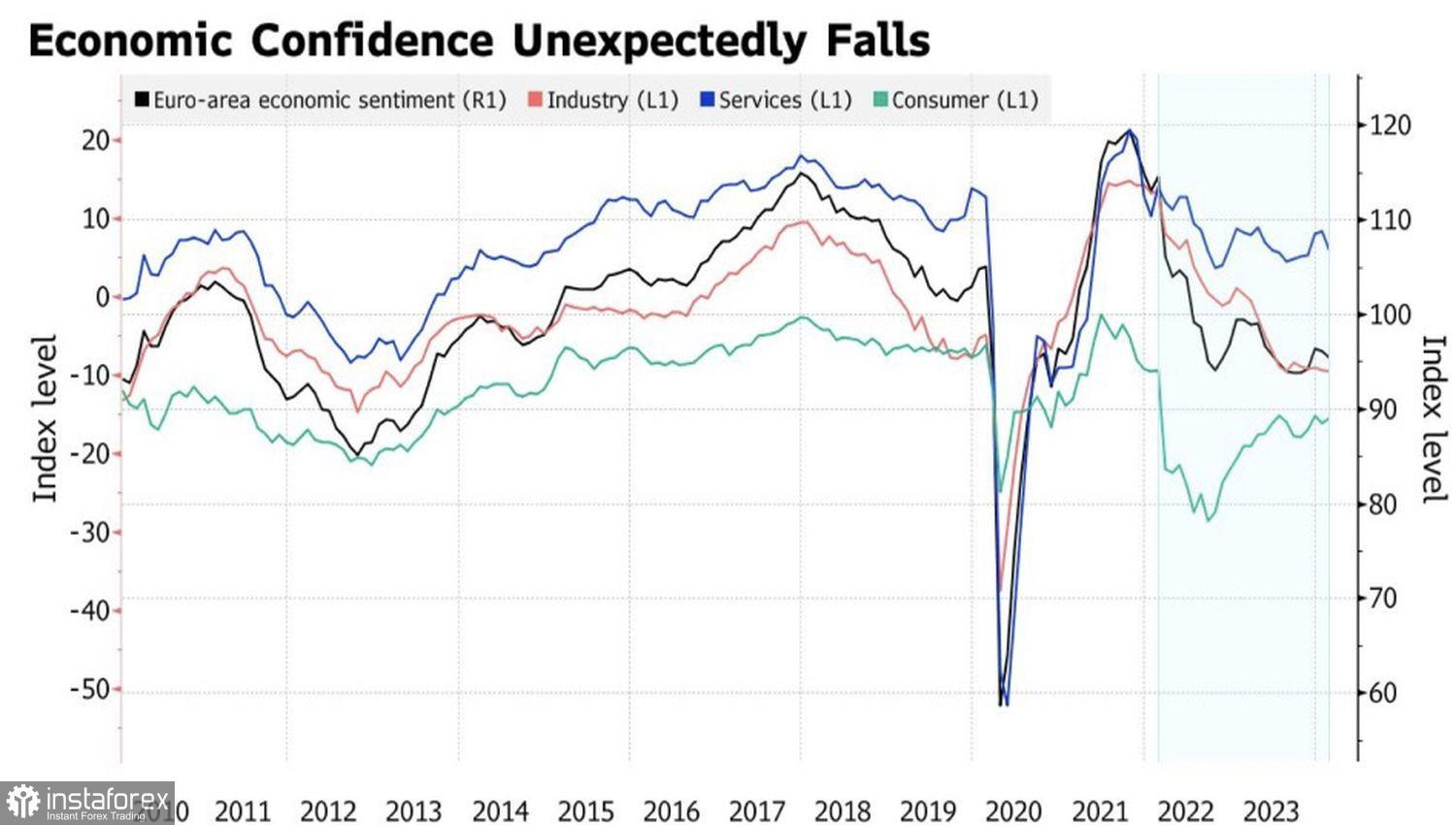

The first decrease in consumer confidence in four months and a sharp drop in orders for durable goods in the U.S. have brought back the topic of slowing U.S. GDP growth to the market. Simultaneously, the peak of economic confidence in the Eurozone to the lowest level in three months indicates that its economy has not yet emerged from the woods. It will continue to balance on the brink of recession and stagflation. Where will the strength come from for the bulls in EUR/USD?

Dynamics of European Economic Confidence

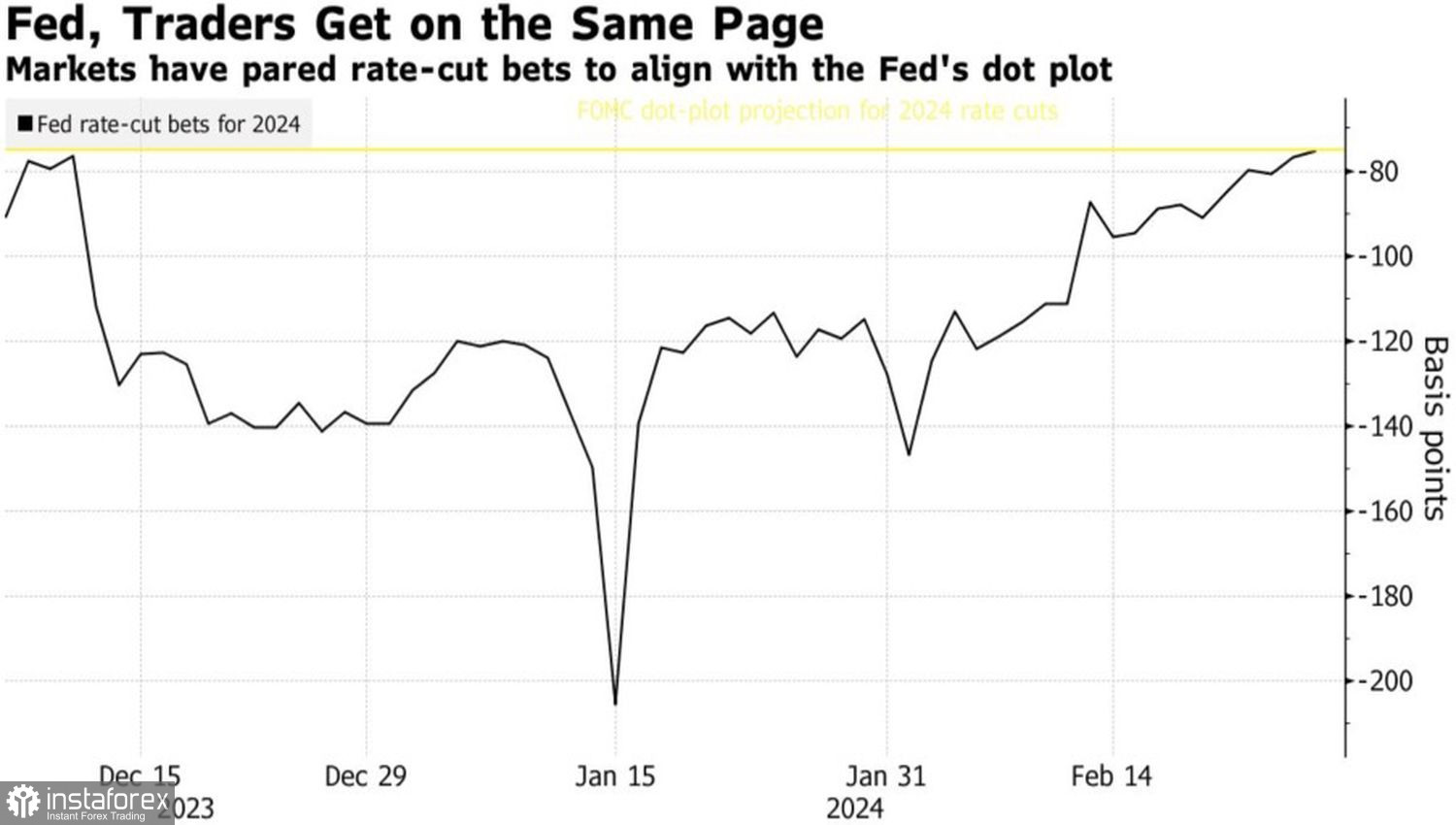

Dollar strength does not negate the fact that the markets have thrown a white flag before the Fed. Initially, by the end of 2023, they anticipated 6-7 monetary expansion acts, but now the expectation has reduced to 3, aligning with the December FOMC forecast. However, the focus is shifting to the start date and speed of monetary policy easing.

Derivatives indicate a 63% probability of the start of the monetary expansion cycle in June. Just a week ago, the indicator was at 80%. I wouldn't be surprised if the hawkish rhetoric of Fed officials drops it below 50%. What remains if Fed Vice Chair Philip Jefferson and the head of the New York Fed, John Williams, state that rates will start to fall at the end of the year?

Dynamics of forecasts for the Fed rate

The situation may change if the Personal Consumption Expenditures (PCE) index for January confirms a downward trend. However, Bloomberg experts predict an acceleration to 0.4% MoM, which implies that the 6-month PCE will return above the Federal Reserve's 2% target. Given the prevailing risks of inflation divergence, including a robust labor market, enhanced financial conditions, and disruptions in supply chains, these factors empower the U.S. dollar with a sense of confidence.

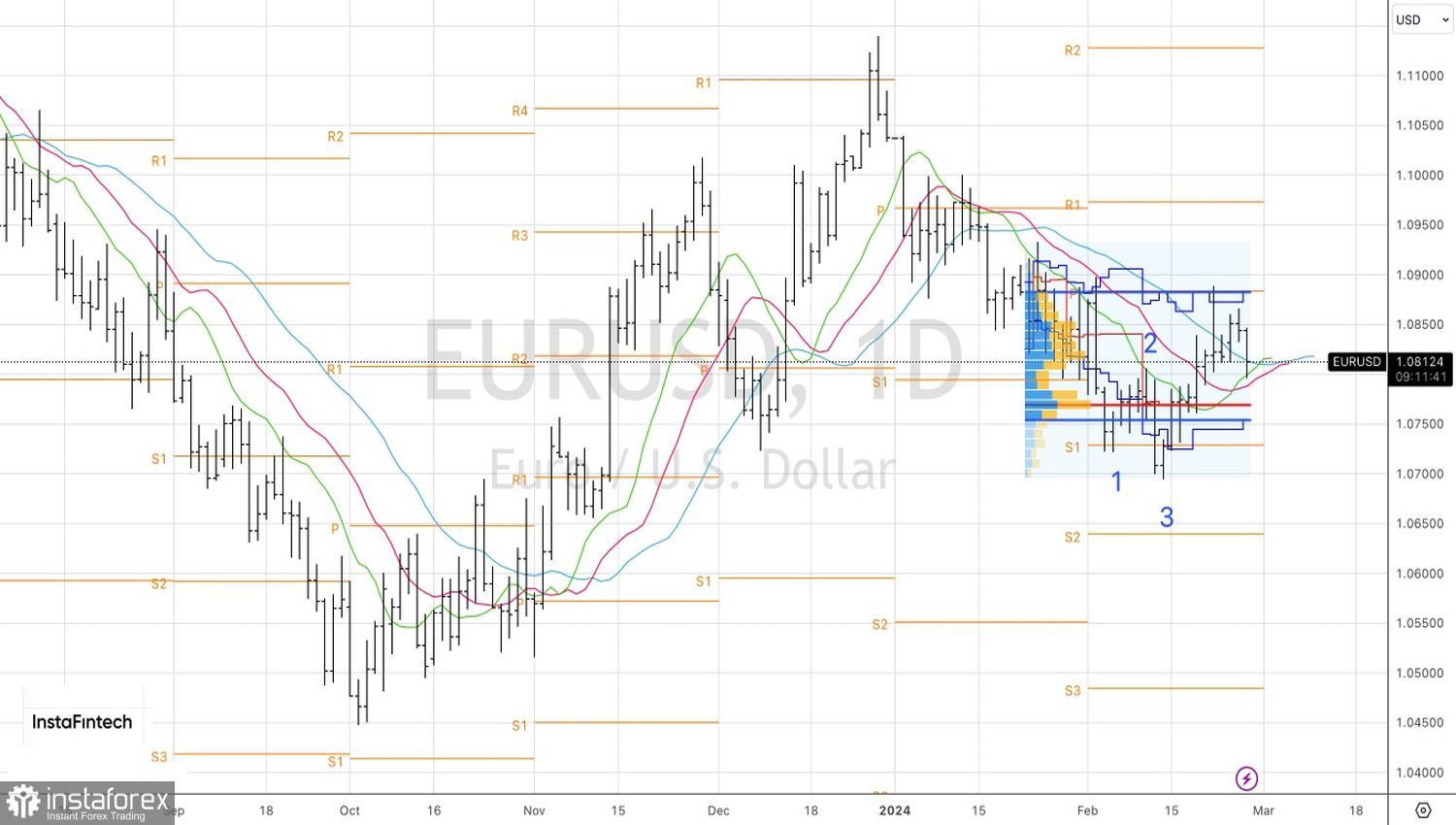

On the daily chart of EUR/USD, the selling strategy towards 1.0815 was executed precisely. The target was reached, allowing for partial profit-taking on shorts. Furthermore, a drop in quotes below the moving averages near the 1.0795 mark will increase the risks of a recovery in the downward trend and provide a basis for increasing short positions.