The U.S. Dollar Index, which tracks the value of the U.S. dollar relative to a basket of currencies, is trying to build on its gains from the past two days.

At the moment, judging by the RSI (Relative Strength Index) oscillator, the U.S. Dollar Index has paused its strong recovery, as the oscillator has yet to move into positive territory.

Nevertheless, the fundamental backdrop calls for caution among bearish traders. Earlier this week, Federal Reserve Chairman Jerome Powell took a more hawkish tone. He stated that he expects two additional 25-basis-point rate cuts by the end of this year, provided the economy remains predictable. In addition, the U.S. Bureau of Labor Statistics (BLS) released the Job Openings and Labor Turnover Survey (JOLTS), which unexpectedly showed an increase in job openings after two consecutive months of declines. This data pointed to a resilient U.S. labor market and prompted investors to lower their expectations of more aggressive monetary easing by the Federal Reserve.

Alongside the continued escalation of geopolitical tensions in the Middle East, this acts as another factor supporting the safe-haven U.S. dollar.

On Tuesday, in response to a campaign against Hezbollah allies in Lebanon, Iran launched more than 200 ballistic missiles at Israel. Additionally, Israeli Prime Minister Benjamin Netanyahu vowed that Iran would pay for its missile attack. Iran, in turn, declared that any retaliatory strike would be met with massive destruction. This increases the risk of a larger-scale conflict in the region, which dampens investors' appetite for riskier assets. As a result, flows are shifting toward traditional safe-haven assets like gold and U.S. Treasuries.

In light of these events, markets are still anticipating more than a 35% probability that the Federal Reserve will cut borrowing costs by another 50 basis points in November. This is seen as a limiting factor for the U.S. Dollar Index and calls for caution among bearish traders.

For short-term trading opportunities today, it's worth paying attention to the U.S. ADP private-sector employment report. This could provide new momentum at the start of the North American session.

However, the main focus should be on the U.S. monthly employment data — the Nonfarm Payrolls (NFP) report, which will be released on Friday. This report will play a crucial role in determining the next move for the U.S. dollar.

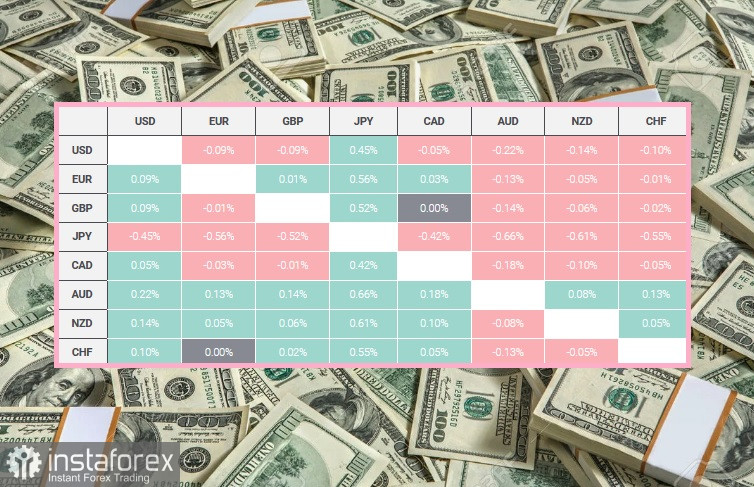

The table below shows the percentage change in the U.S. dollar against the listed major currencies today.

The U.S. dollar has gained the most against the Japanese yen.