Futures for European and US stocks declined due to uncertainty and the usual pause traders take ahead of key economic data releases. Investors remain cautious as they are waiting for US employment data, which will help determine the future path of interest rates.

Euro Stoxx 50 futures dropped 0.3%, while S&P 500 contracts fell 0.1%. Meanwhile, growth in mainland China pushed Asian stocks to a new high, with the Hang Seng Tech index rising 2.9%.

Markets showed mixed movements as investors waited for US nonfarm payroll data, set to be released today. This report is likely to divert attention from the tariff drama that shook financial markets earlier this week. Weak labor data could strengthen expectations of further Federal Reserve easing, a topic increasingly discussed by Fed officials.

Friday's employment report is expected to show a job gain of 175,000. A separate labor report released yesterday revealed an increase in initial jobless claims, while labor productivity slightly missed economists' forecasts. In addition to employment figures, Wall Street will closely watch the unemployment rate today. All of this is creating tension in financial markets, where investors anticipate potential changes in monetary policy.

If job growth continues to slacken, the Fed may reconsider its current strategy. The employment report is also crucial in the context of inflation, which remains elevated. The unemployment rate, expected at 4.1%, will serve as an additional indicator of economic resilience. Many analysts believe that if unemployment rises, it could trigger new economic stimulus measures.

Fed Chair Jerome Powell stated last week that officials want to see more progress in fighting inflation and will rely on a sustained decline in price pressures. For now, traders still expect the Fed's next move to be a rate cut, though likely not before mid-year. Treasury yields hit their lowest levels of 2025 this week.

As for the Asian market, excitement around DeepSeek remains strong. Xiaomi shares hit a new record high thanks to a subsidy program, while automaker BYD surged 20% as traders awaited updates on its autopilot technology.

The yen weakened against the US dollar on Friday ahead of a meeting between Japanese Prime Minister Shigeru Ishiba and US President Donald Trump.

Gold rose after retreating from a record high on Thursday. Oil also rebounded following Thursday's decline, as Trump's renewed pledge to lower crude prices overshadowed his push for tougher sanctions against Iran.

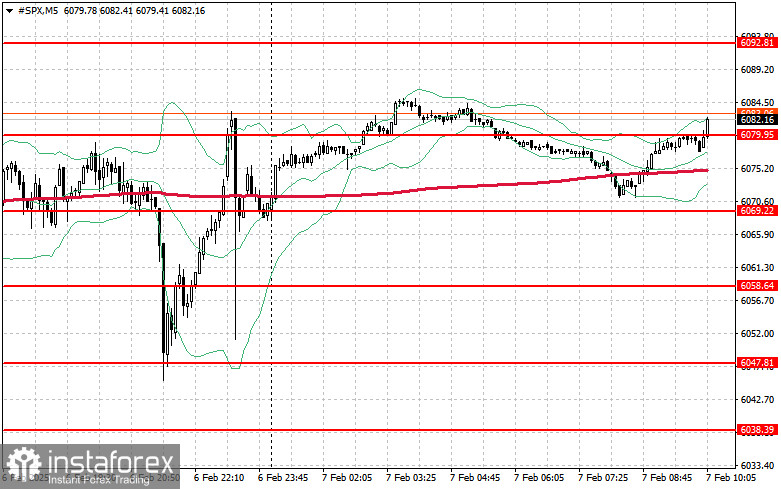

Demand for the S&P 500 remains high. Today, buyers' main goal is to break the nearest resistance at $6,079, which would allow the uptrend to continue and open the way to $6,092. Holding above $6,107 will further strengthen buyers' positions.

If risk appetite declines, buyers may step in around $6,069. A break below this level would quickly push the index back to $6,058, thus paving the way to $6,047.