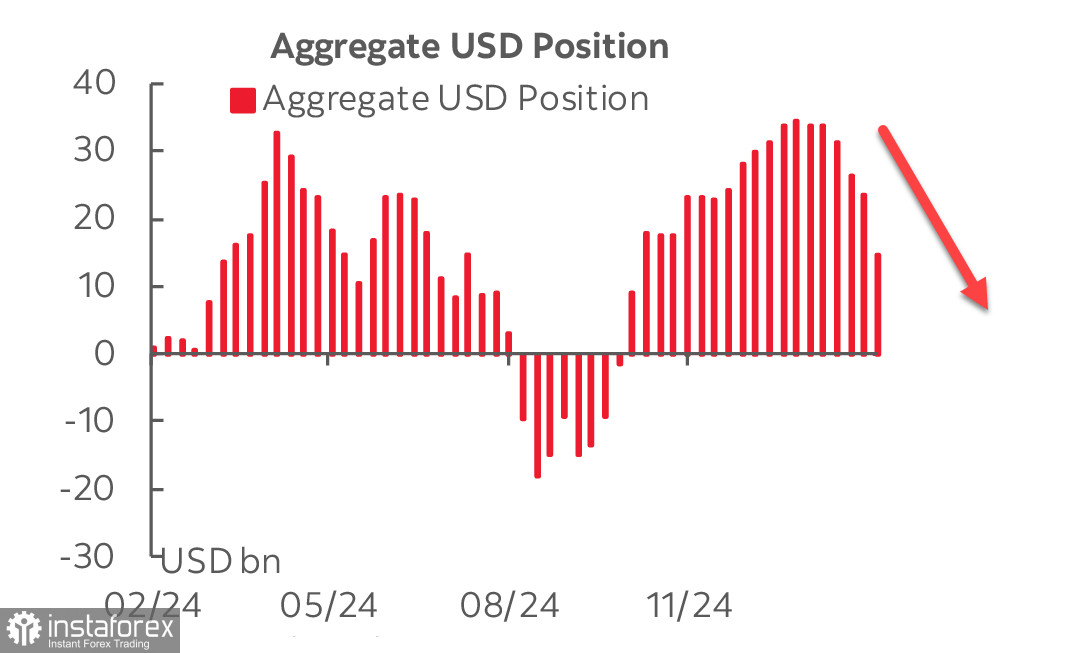

The CFTC report published on Friday revealed an unexpectedly strong impulse toward dollar sell-offs, with the total speculative long position on USD against major currencies shrinking by $8.2 billion to $15.4 billion.

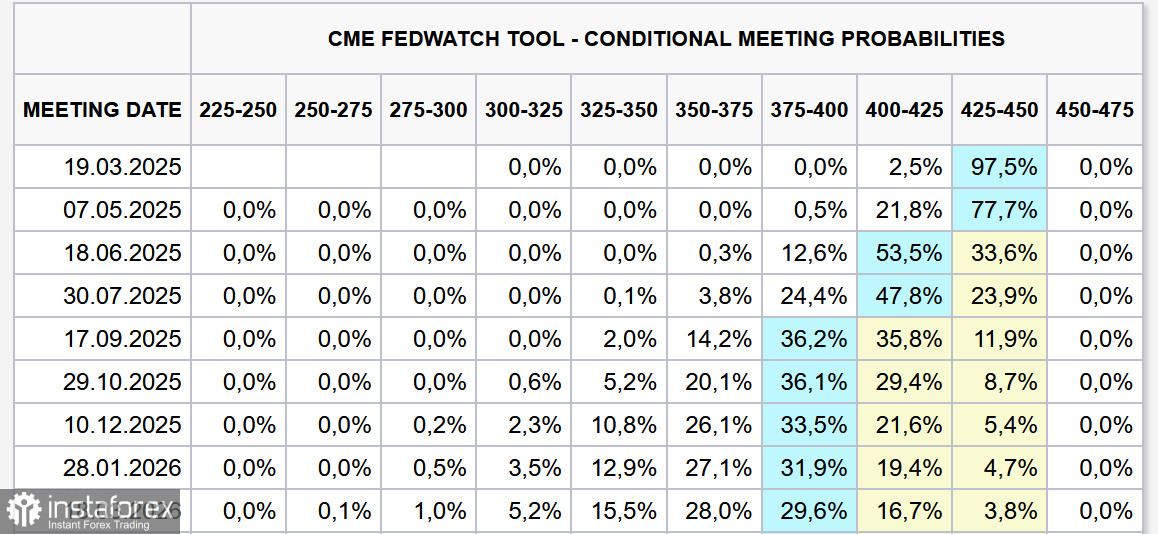

The market's response to Trump's initial policy moves has been somewhat unexpected. Instead of focusing on the risk of rising inflation—a widely discussed consequence of Trump's pro-inflationary economic policies—investors have suddenly shifted attention to the possibility of economic slowdown and an impending recession. As a result, expectations for Fed rate cuts have become more aggressive, suggesting that the market perceives inflationary risks as weakening rather than strengthening.

On the surface, the tariff war should benefit the U.S. economy. Treasury Secretary Scott Bessent, following Ukraine's delegation's visit to Washington, stated that tariffs are expected to generate substantial revenue for the U.S. budget, which is critical given the federal deficit projections. According to the Congressional Budget Committee, the 2025 federal deficit is projected at $1.9 trillion, potentially expanding to $2.7 trillion by 2035. Addressing this shortfall requires new borrowing, but rising national debt amid high interest rates only worsens the fiscal imbalance.

The new Trump administration aims to break this cycle by:

- Cutting spending, primarily in the military sector

- Increasing revenue through higher tariffs

- Creating favorable conditions for business growth to boost corporate valuations and increase tax revenues

This strategy aligns with the rally in stock indices, which reflects confidence in the new economic policies.

The biggest threat to the U.S. dollar stems from reduced global tensions, which diminish demand for the dollar as a safe-haven asset, while simultaneously boosting risk appetite for equities and high-yield assets. These conditions favor a weaker dollar, making investors' reactions understandable. However, if the tariff war fails to deliver its intended economic benefits, other risks—such as rising inflation and economic stagnation—will become more pressing concerns. In this scenario, the stock market could also come under pressure, though it is too early to draw definitive conclusions.

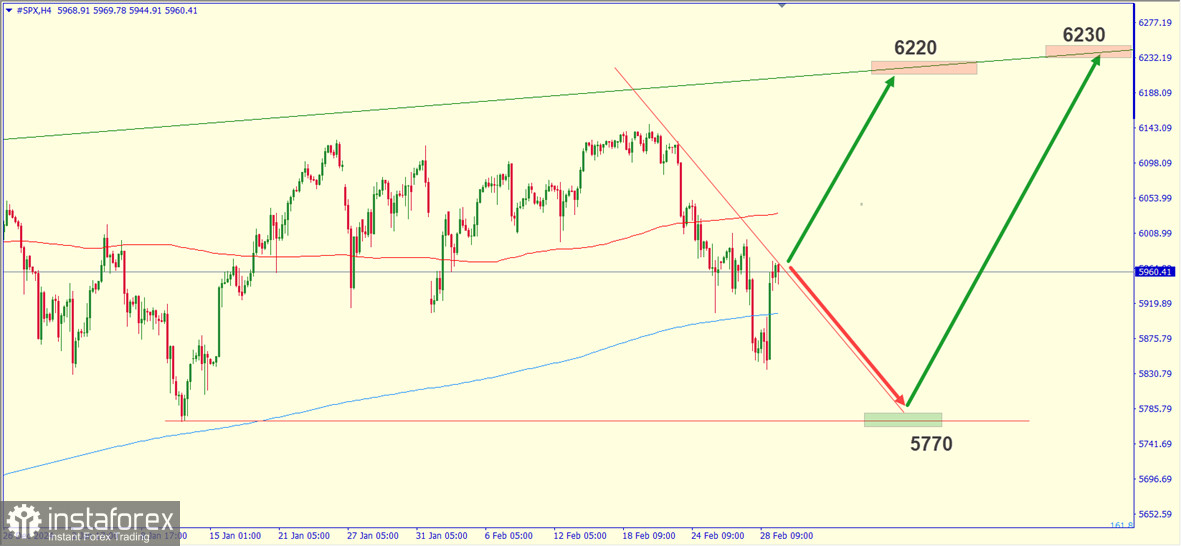

Outlook for the S&P 500 and U.S. Economy

We maintain a bullish outlook on the S&P 500. While the dollar may weaken due to easing geopolitical tensions and renewed euro optimism, U.S. equity markets remain well-positioned for further gains. Historically, a weaker dollar supports stock market growth, a trend that has long been well-documented and fundamentally sound.

The risk of a U.S. recession has increased, but negative trends will only accelerate if economic weakness worsens rather than stabilizes. The Trump administration's approach focuses on creating an optimal business environment and revitalizing the U.S. industrial base, which should, in theory, support stock indices over time.

Last week, support for the S&P 500 was observed near the 5900 level, with the index briefly dipping below but remaining above the key technical threshold of 5760. We expect the rally to resume, with targets at 6200/6300, which remain the primary objectives for the near term.