Japan's real GDP grew by 0.3% quarter-on-quarter (1.0% y/y) in the second quarter of 2025, exceeding Bloomberg's market forecast (+0.1% q/q, +0.4% y/y). This marked the fifth consecutive quarter of growth, with first-quarter figures revised upward from negative to positive. Key components of domestic demand, such as private consumption and private investment, made a significant contribution.

Exports also increased, and while the overall outlook remains negative and the Japanese economy has entered a slowdown phase, for now there is little cause for concern. Factors that could have prevented the Bank of Japan from raising rates (and thereby supporting the yen) have weakened in influence.

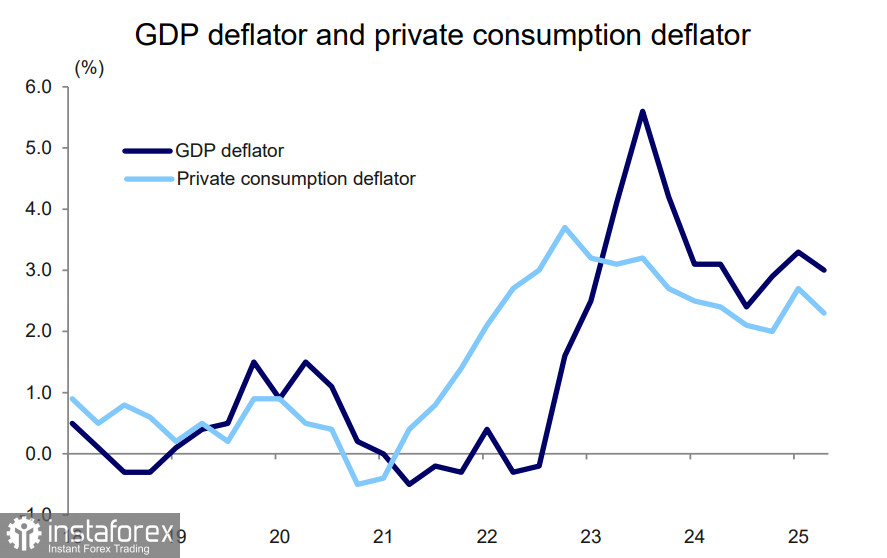

It is also worth noting that wages rose by 0.6% in real terms, pointing to an improvement in household incomes. The GDP deflator, reflecting inflationary pressure, declined slightly but remains strong.

Following the release, the Nikkei 225 index surged by 729 points on the day, setting a new closing high. Government bond yields also rose as expectations for further Bank of Japan rate hikes increased.

However, what is positive for markets may look different when viewed from the perspective of the BoJ's policy objectives. The BoJ has already reviewed regional bank reports, which indicate that the higher tariffs imposed by Trump's administration have not yet had a significant negative impact on macroeconomic indicators. Overall, this suggests that as long as the economy remains within acceptable parameters, the BoJ may avoid rushing into further rate normalization, opting instead to maintain its pause.

Most likely, the BoJ will wait until the economy begins to respond to the new U.S. tariff policy. Since that has not yet happened, the outlook for interest rates remains open. This is probably why the yen showed no reaction to the GDP report.

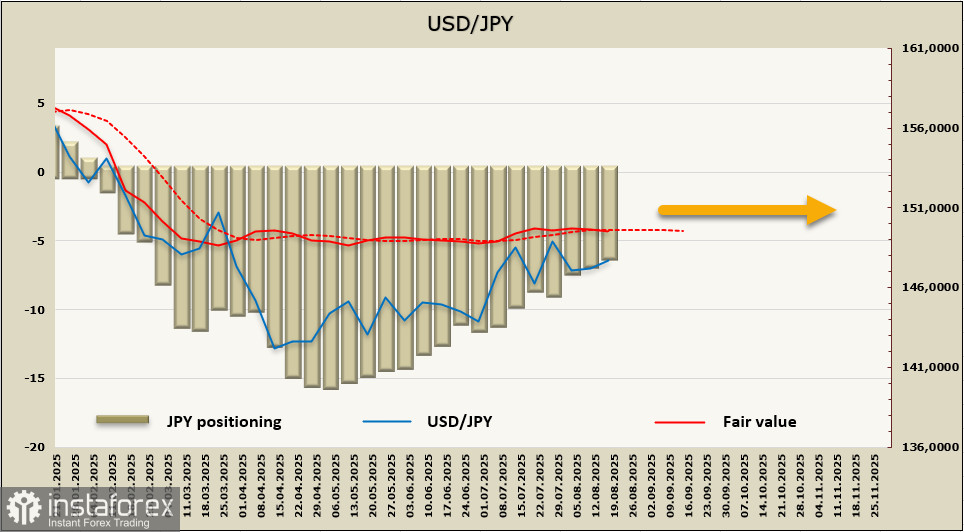

Net long positions on the yen contracted again, decreasing by 667 million over the reporting week to 6.277 billion. The shift in positioning toward the bearish side has continued since May, but the accumulated long bias is still notable. The estimated price has lost all momentum.

The previous week, we expected the yen to weaken on reduced geopolitical tensions, but the market reacted with calm indifference. The yen is trading in a narrow range, and at present there are no signs of movement in either direction. Technically, range trading could persist for some time, at least until the September FOMC meeting. The yen is supported on the downside by the 145.50/70 zone and capped on the upside at 149.10/40. For now, it remains unclear what could drive a breakout from this range in the coming month.