The British pound fell sharply on Tuesday due to a spike in 30-year bond yields, which reached 5.69%—the highest level since March 1998.

This jump in yields followed UK Chancellor Reeves's decision to increase government borrowing, which automatically led to a rise in risk premiums. Without additional debt, the budget cannot be balanced—even though economic growth in the first half of the year exceeded forecasts (0.7% QoQ in the first quarter and 0.3% QoQ in the second quarter), it was mainly driven by government spending, as business investment declined and private consumption remained weak at 0.1% QoQ. Tighter fiscal policy will become yet another restrictive factor for the economy, and the labor market is weakening. Additional borrowing in the current budget means revenue remains weak, despite high inflation.

The delayed effect from changes in inflation forecasts also played a role. As is well known, the Bank of England kept interest rates unchanged at its August meeting, but the split in the vote was significant, as were revised inflation forecasts toward higher values. Market expectations for the rate remain unchanged—a 25bp cut in November—but it is uncertain if this decision will be made if inflation shows even higher growth. Uncertainty is rising, as is the risk premium.

Again, additional growth in public debt, with an already high current account deficit, means the pound could react with a sharp decline if capital inflows slow, which is already happening, considering the negative investment dynamics.

As a result, the pound is now more vulnerable than the market recognizes, and the risk of further decline is notably higher than the risk of a resumed rally.

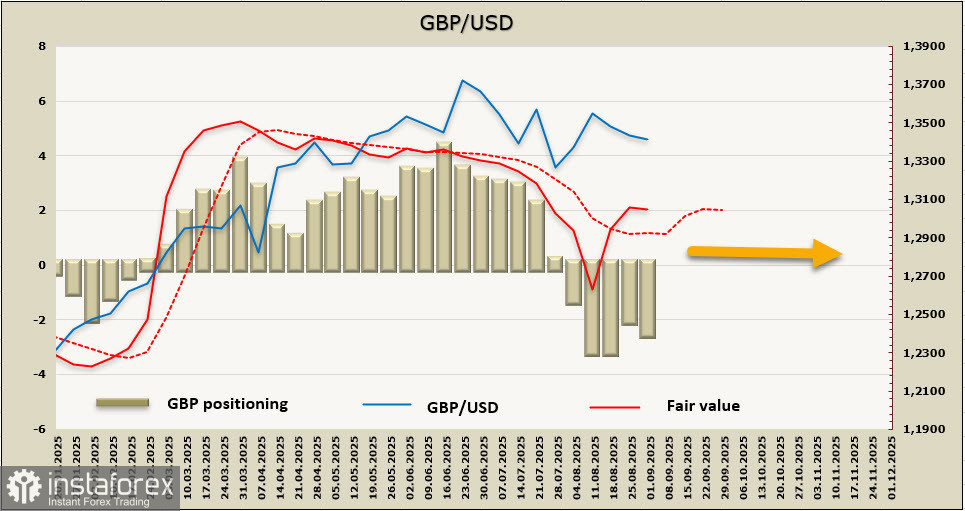

The net short position on GBP increased by £0.5bn in the reporting week to -£2.6bn; speculative positioning is bearish, and the estimated price is above the long-term average, which provides grounds to expect a potential resumption of the uptrend, but there is no clear direction.

The pound continues to consolidate after strong growth in the first half of the year, and it seems this period is coming to an end. The nearest support is at 1.3310/30; we expect it to be tested soon, and if the pound falls lower, the next target will be the local low at 1.3140. A resumption of the bullish trend is unlikely.