In financial markets, everything is accounted for—even when data is scarce, investors turn to leading corporate earnings as signals. In this context, the optimistic outlooks shared by General Electric, Philip Morris, and Coca-Cola speak louder than recent U.S. labor market concerns. For these manufacturers, the glass is half full, casting doubt on the likelihood of aggressive Fed rate cuts and lending support to EUR/USD bears.

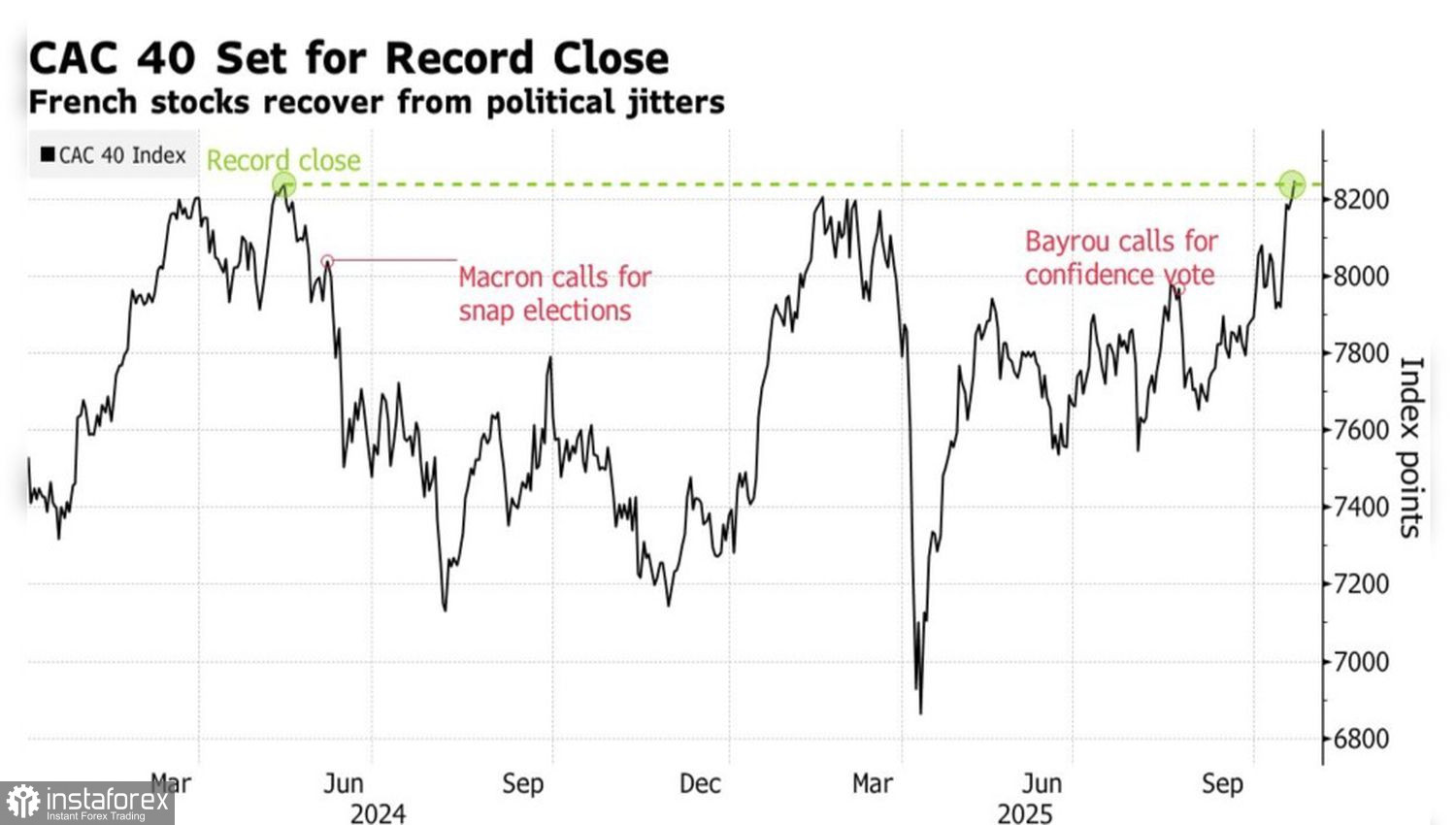

Many are citing France's S&P Global rating downgrade and the looming budget battle between Prime Minister Sebastien Lecornu and the French parliament as the primary reasons for the euro's weakness. However, the CAC 40 index reaching a record high and stable spreads between French and German government bond yields suggest that political risk has already been factored into asset prices.

CAC 40 Performance vs. Rating Downgrade

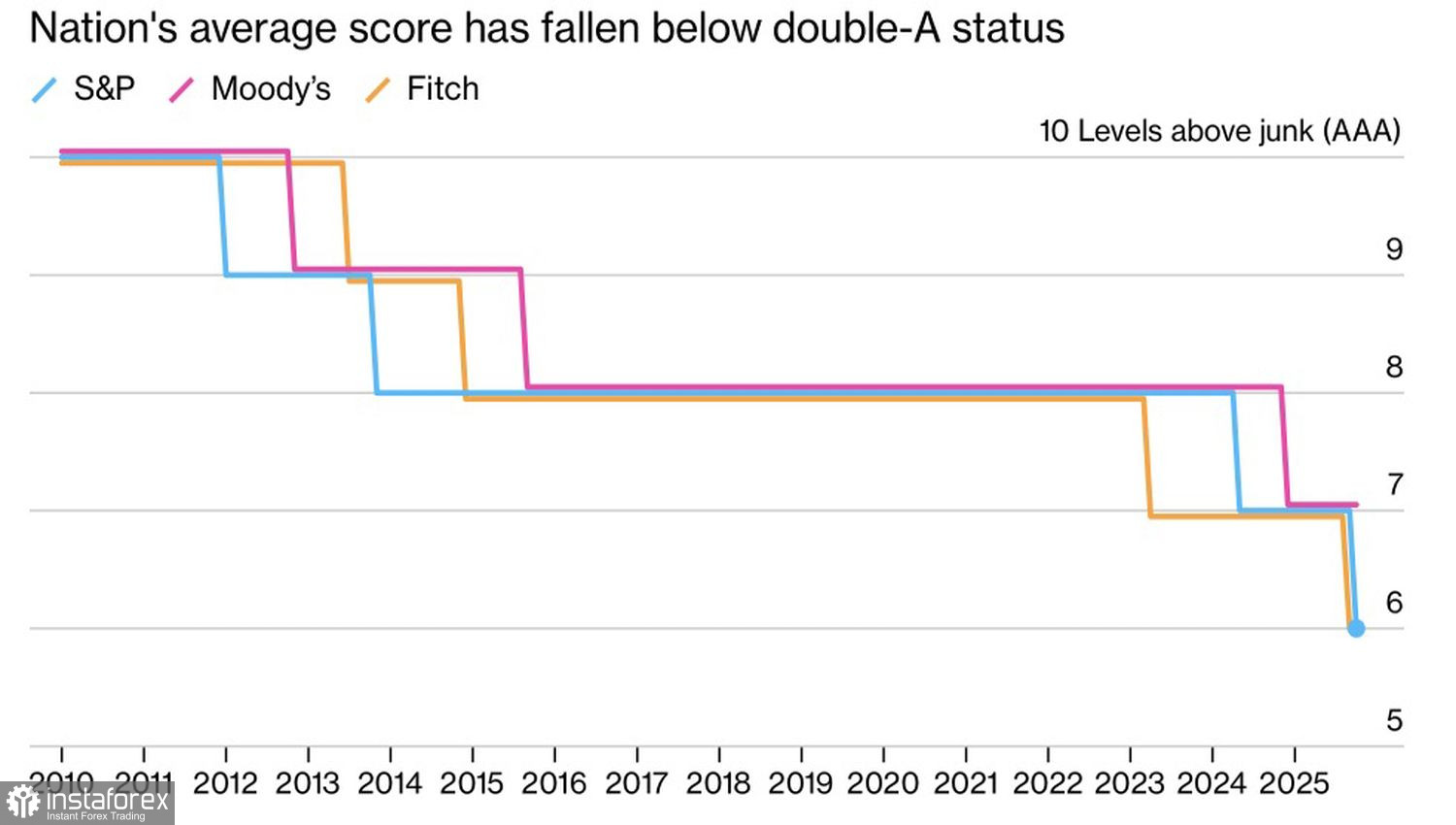

The prospect of a downgrade by S&P Global had been widely discussed in advance, as had the upcoming Moody's review scheduled for October 24. In theory, downgrades should trigger forced selling by investment funds with strict mandates. In reality, many of these funds are waiving those restrictions to hold onto assets they still deem valuable. The weakness in the euro is clearly being driven by factors extraneous to French domestic politics.

Indeed, Lecornu's initial proposal to reduce the fiscal deficit from 5.4% of GDP to 4.7% may struggle to gain traction in parliament. However, the prime minister retains some flexibility—he has previously suggested a figure slightly below 5%, while S&P Global referenced 5.3%. That level could gain cross-party approval among both left- and right-wing lawmakers.

The real bearish momentum in EUR/USD is being fueled by strong Q3 earnings from U.S. corporations and fading hopes for peace in Ukraine. A statement from Donald Trump regarding a potential meeting with the Russian president in Hungary briefly boosted the euro amid speculation over a peace deal. Trump voiced strong intentions to pursue a resolution, but Moscow responded with a clear signal that it is not ready to negotiate an end to the conflict. Had peace talks shown real promise, a reduction in geopolitical risk would have supported eurozone currencies.

Dynamics of France's credit ratings

The Kremlin demands territorial concessions it cannot currently capture, while Kyiv appears willing to freeze the conflict along the current front lines. The gulf between both parties remains vast, so a breakthrough at a Trump–Russia summit seems unlikely. The euro remains under pressure, while upbeat U.S. corporate earnings embolden EUR/USD bears.

Technically, the daily EUR/USD chart shows a rejection from dynamic resistance levels represented by key moving averages. This increases the likelihood of a corrective phase forming against the prevailing long-term bullish trend. Short positions initiated from the 1.1640 region are justified and might be strengthened if support at 1.1600 is broken.