Last Friday, the stock indices closed with gains, with the S&P 500 up by 0.64%, the Nasdaq 100 gaining 0.52%, and the Dow Jones Industrial Average increasing by 0.47%.

Global stock markets continued to rise, strengthening for the fourth consecutive trading day amid expectations of a year-end rally. The MSCI All Country Index rose on Tuesday after setting a new closing high in the previous session. The Asia-Pacific stocks index climbed by 0.5%, while American stock futures displayed a less vigorous rally, remaining stable. In the commodities market, gold reached yet another historical high, marking the 50th day this year when it has set records. Silver also hit a new peak.

The Japanese yen has remained a focal point for currency traders, strengthening for the second day in a row and surpassing the 156 yen per dollar mark. This occurred after Finance Minister Satsuki Katayama stated in an interview that the country has "freedom of action" to take decisive measures against currency fluctuations. These comments served as a stern warning for speculators following the yen's weakening to 157.78 yen, even after the central bank raised interest rates last Friday.

Positive sentiment among equity investors has helped the S&P 500 index recoup December losses on Monday and paved the way for an eighth consecutive month of growth, marking the longest streak since 2018. Leaders in growth among major companies included Tesla Inc. and Nvidia Corp.

Following another successful year for the stock market, the key question is whether investors will maintain this positive sentiment in 2026. Positions in the stock market are increasing, while fund managers maintain record-low cash levels. Their expectations for further growth outweigh concerns about inflated valuations of technology companies.

Federal Reserve Chairman Stephen Miran stated that the central bank risks triggering a recession if it does not continue to lower interest rates next year, which has only fueled appetite for riskier assets.

Chinese stocks performed the worst in Asia after analysts at Citigroup Inc. downgraded their ratings, citing less favorable profit forecasts and disappointing macroeconomic outlooks.

Meanwhile, oil prices stabilized after four days of increases, amid reports that the US continues its blockade on oil supplies from Venezuela. Brent crude prices approached $62 per barrel after rising about 5% over the previous four sessions, while West Texas Intermediate crude was priced around $58. It is worth noting that the US has taken control of two Venezuelan tankers and is seeking to capture a third, all part of Washington's measures to pressure Nicolas Maduro's government.

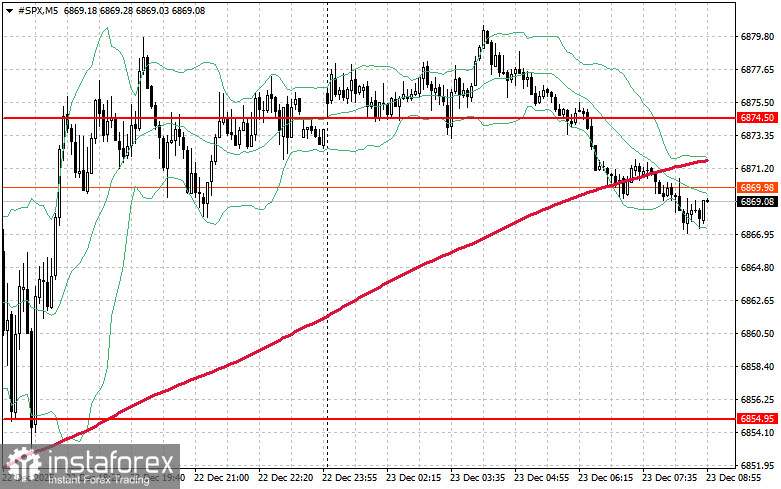

From a technical perspective, the main task for buyers in the S&P 500 today will be to overcome the nearest resistance level of $6,874. Doing so would indicate growth and open the opportunity for a surge to a new level of $6,896. An equally critical task for bulls will be to establish control above the $6,905 mark to strengthen their positions. In the event of a downward movement amid declining risk appetite, buyers must assert themselves around $6,854. A break below this level could quickly push the trading instrument back to $6,837 and pave the way down to $6,819.