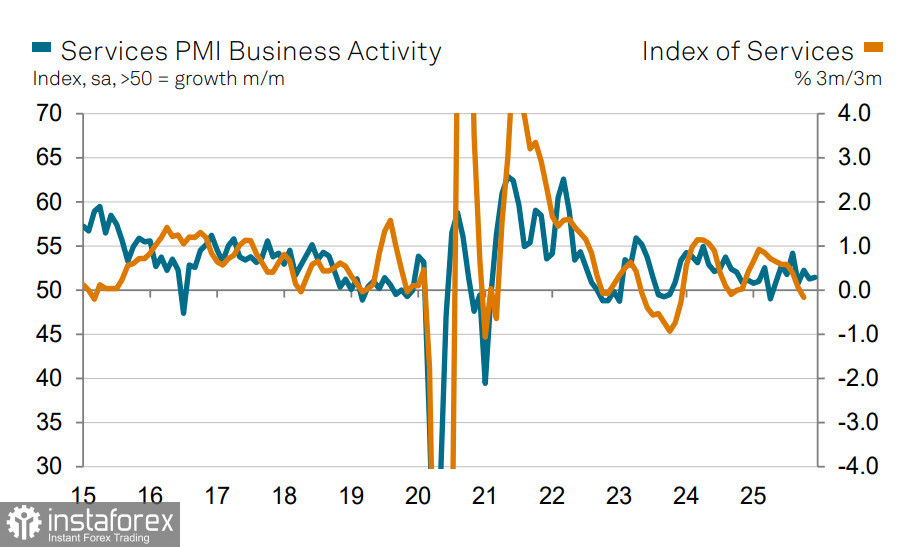

The pound's strong rally since November slowed on Tuesday after the release of the UK Services PMI for December. Business activity growth continued for the eighth consecutive month, but the pace of growth was weak and virtually unchanged from November (51.4 vs. 51.3), while the final reading came in below the preliminary estimate of 52.1. The sub-indices for new orders and sales were broadly unchanged, but the employment situation is deteriorating, with an overall reduction in staff levels observed for the fifteenth consecutive month.

PMI data, in general, do not carry much positive news for the pound, so it was quite natural for the market to react with some weakening of the currency. However, after some time the pound resumed attempts to rise. Possibly this is due to the report noting a sharp increase in costs, which led to the fastest growth in input prices since May; prices for final goods increased noticeably faster than in November. The overall picture therefore looks less attractive, especially from the perspective of the Bank of England: economic growth is weak, employment is declining, and prices are rising—that is, the threat of high inflation remains amid an unstable economy.

The Bank of England cut the rate in December to 3.75%, but the votes of the Committee members were split 4–5, indicating a complete lack of consensus. The threat of accelerating inflation adds arguments for the hawks, so the probability of a shift toward a more accommodative policy has decreased, which is a bullish factor for the pound.

Thus, as of Wednesday morning, the pound has fairly strong positions to continue rising, but not everything depends on it. The second half of the week risks being much more volatile, as later today the U.S. ADP private-sector employment report, the ISM Services PMI, and the JOLTs job openings report will be released. The state of the U.S. labor market raises many questions, as there are increasing signs of an economic slowdown, and the key December employment report expected on Friday could trigger a surge in activity, since the probability of deviations from forecasts in either direction remains high.

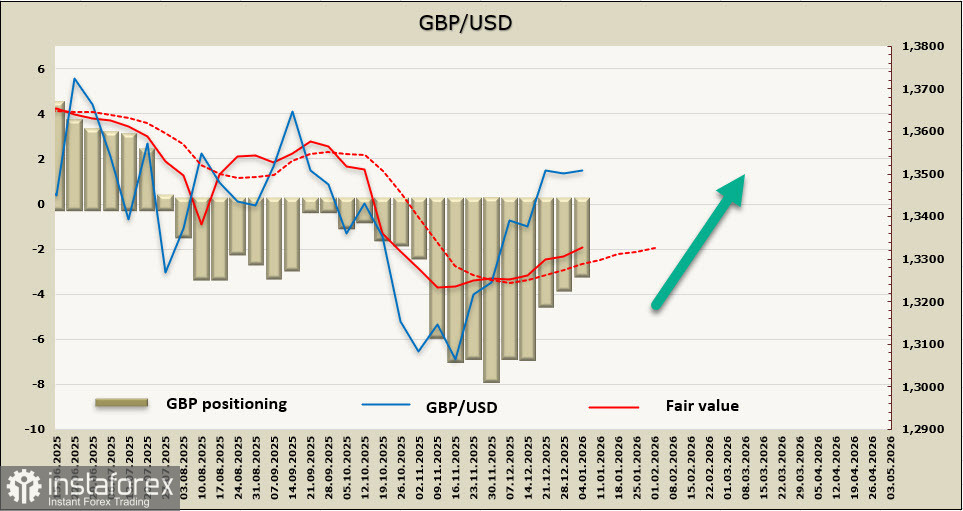

The calculated price remains above the long-term average, suggesting further appreciation of the pound.

In the previous review, we noted that the pound would aim for the 1.3620–1.3640 resistance zone; this forecast remains valid. The pound has started the year more confidently than the dollar and has reached a three-month high, returning to the levels it held before the important Fed meeting in September. The likelihood of a correction is minimal: there will be no major news from the UK until the end of the week, and the dynamics of GBP/USD will be entirely determined by news from the United States and geopolitical factors.