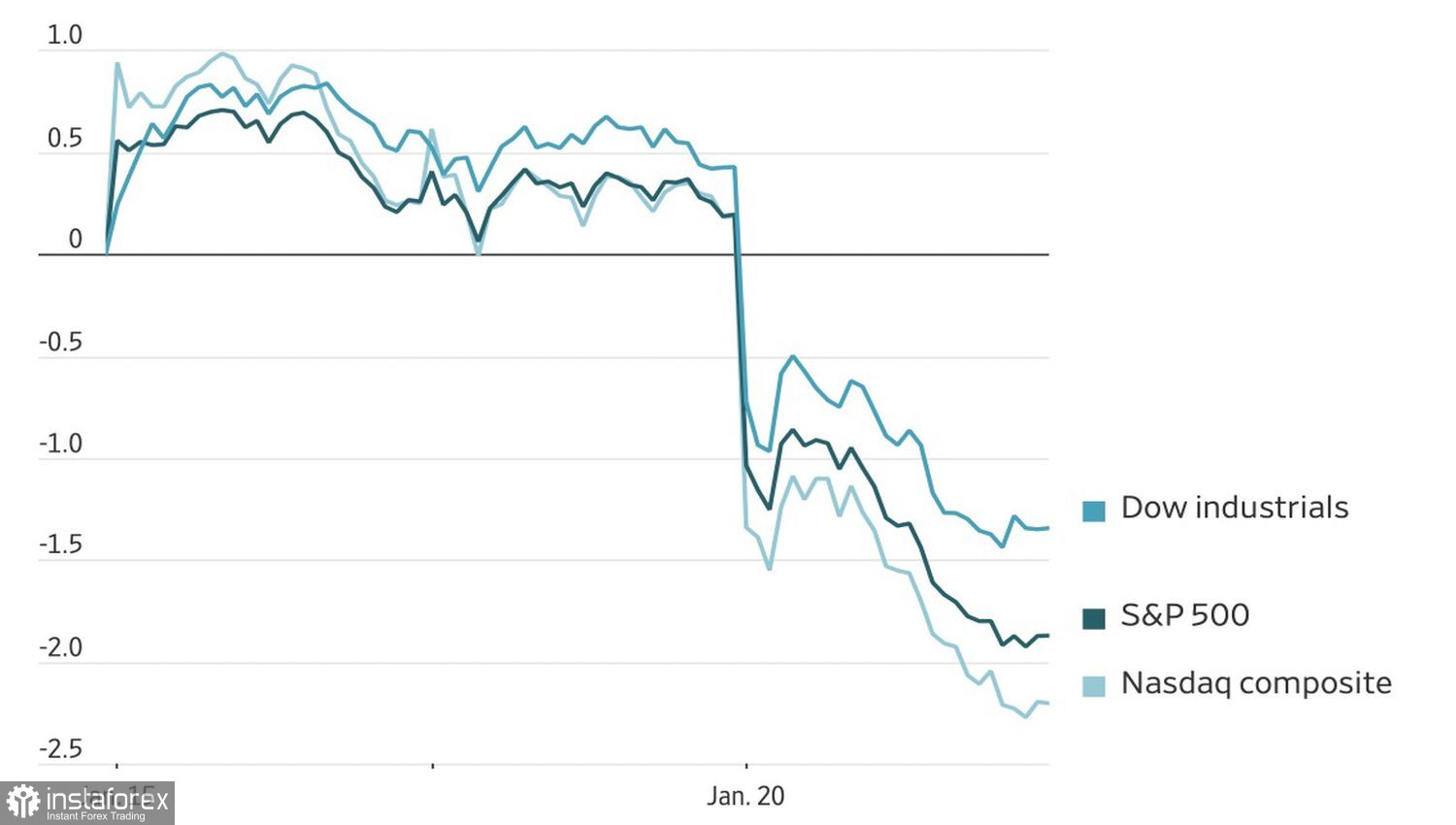

The crash in the US equity market was not as extensive as on Independence Day in April, which suggests that some investor hope for an amicable resolution of the US?Europe conflict. A trade war would slow global economic growth and negatively affect corporate profits. Should we be surprised by the drop in the S&P 500 and other equity indices?

Dynamics of US Stock Indices

According to JP Morgan, the pullback in the US equity market is a message to Donald Trump. After the White House introduced the largest tariffs since the 1930s, the market also collapsed, which forced the administration to adopt a conciliatory tone. Scott Bessent has already taken that line. He urged investors and Old?World partners to remain calm and dismissed the idea of Europe selling off US assets as absurd.

Markets keep the TACO strategy, or "Trump Always Chickens Out", in mind, while Polymarket assigns just a 17% probability to the imposition of 10% tariffs on all eight European countries from February 1. The odds that at least one of them will face import duties are assessed at 37%. In reality, investors expect concessions from the Old Continent. It reacted as menacingly as in April to Trump's tariff threats, but in 2025, it backed down and agreed to 15% levies.

Some countries are now calling for non?compliance with that agreement, yet Brussels does not want to escalate the conflict. Officials say, "a deal is a deal."

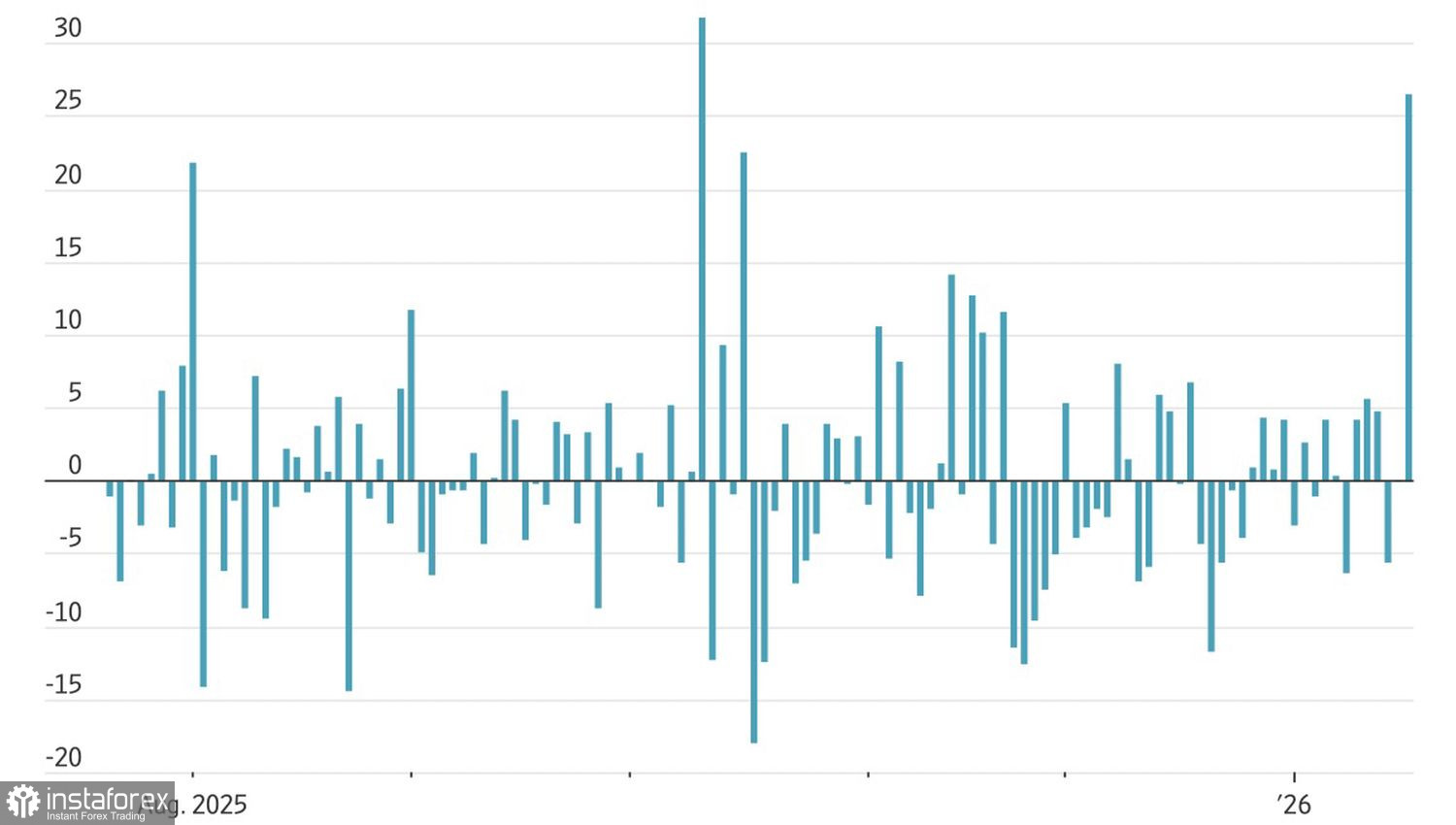

That does not make it easier for markets. The market capitalization of the Magnificent Seven stocks fell by $653 billion as a result of the sell?off, and Apple shares plunged by 3.5%. The VIX volatility index recorded its largest spike since October, when Donald Trump threatened China with 100% tariffs.

Stock Market Volatility Dynamics

The Supreme Court did not come to the S&P 500's rescue. It decided not to rule on the legality of the White House tariffs and went on a four?week recess. The final decision may be postponed until June, which gives Donald Trump more latitude in the Greenland dispute. Had the judges forced the rollback of import duties, that would have been seen as fiscal stimulus and would have helped US equities.

Pressure on the S&P 500 was amplified by the rise in 10?year Treasury yields to levels not seen since August. The sell?off drivers included not only investors' desire to shed US exposure but also a surge in Japanese bond yields as a result of the Takaichi trade. Markets increasingly describe the idea of snap elections as the prime minister's political gamble. Its fiscal stimulus risks stoking inflation and provoking voter discontent.

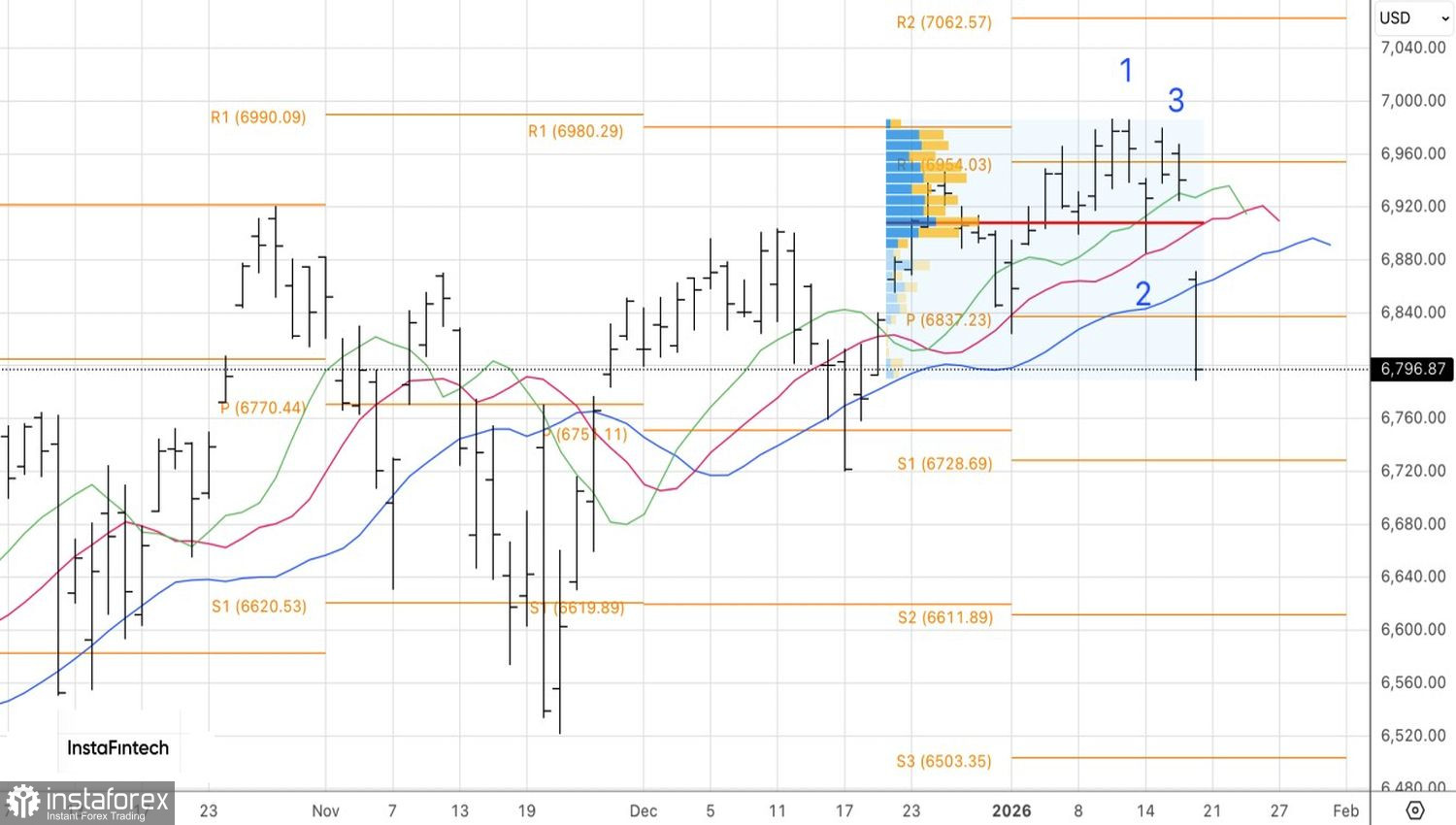

Turning to technical outlook for the S&P 500, the daily chart shows a 1?2?3 reversal pattern. The risks of a corrective move toward the pivot levels of 6,730 and 6,620 have increased. As long as the broad index is below the resistance level of 6,835, emphasis should remain on short positions.