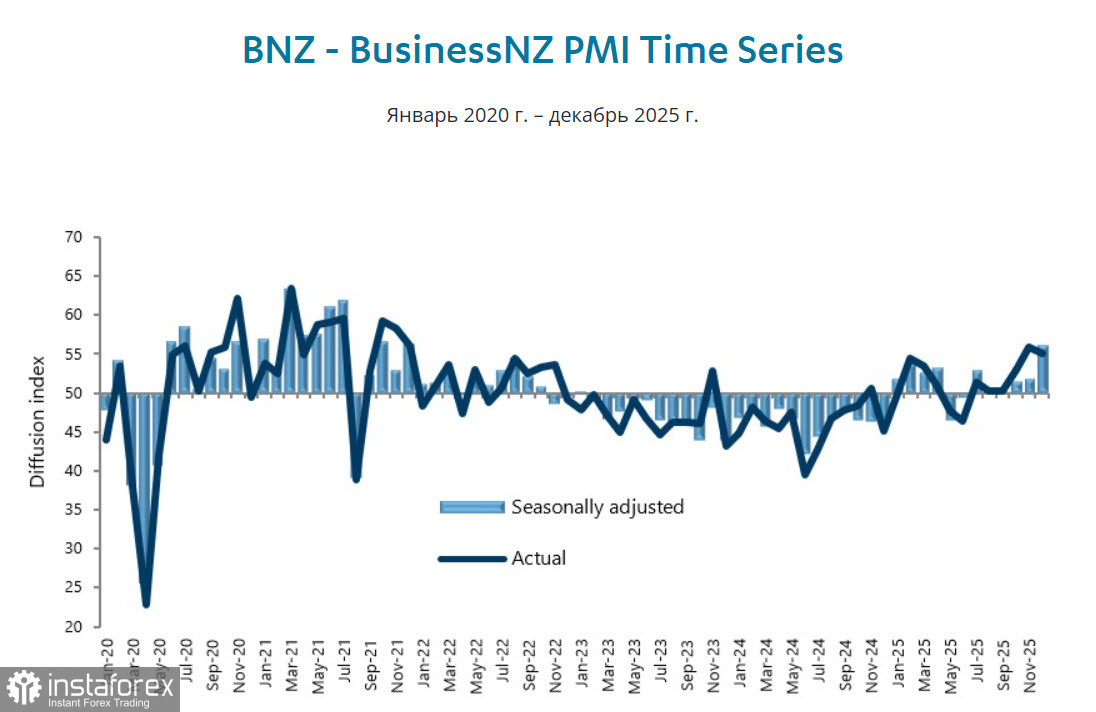

PMI indices in December showed an impressive rise, confirming forecasts of a rapid recovery in New Zealand's economy in Q4. Manufacturing activity increased from 51.4 pts to 56.1 pts — the largest monthly gain in over four years for a single month — while the services sector posted a more modest but still notable increase to 51.5 pts versus 46.9 pts a month earlier. Looking at the report details, the new orders sub-indices recorded the highest increase in both sectors, indicating a strong positive impulse driven by a noticeable improvement in demand.

Since the quarterly NZIER survey published earlier also showed a marked positive outcome, taken together, there is clearly potential for upward revisions to short-term forecasts.

From the Reserve Bank of New Zealand's perspective, the most worrying aspect is that 25% of firms intend to raise their selling prices. This is a substantial jump compared with 7% who held the same view a quarter earlier. Moreover, this level corresponds to annual inflation that is well above the upper half of the RBNZ's target range.

But what is a threat to the RBNZ is a strongly bullish factor for the currency, since it is an obvious argument for raising rates rather than cutting them. On January 22, the consumer price index for Q4 will be published; it is expected to show 2.9% year-on-year, slightly below the Q3 figure, but the risks that the outcome will exceed forecasts are visibly rising. Any deviation from the forecast, even if minimal, will prompt a revision of long-term forecasts and exert pronounced bullish pressure on NZD/USD.

The US dollar has fallen sharply this week, and whereas on Monday the move was only nascent and looked like a correction, by Wednesday it had taken on the character of a collapse. There are no economic reasons for such activity, and it is clear that the market is rebalancing on the basis of geopolitical factors. The market is waiting to hear what will be announced in Davos regarding Greenland and the tariffs that Trump threatens to impose on Europe.

So far, the explanation for the dollar's decline and for US equity indices is directly linked to the situation around Greenland. Trump's threats to impose tariffs on European allies over Greenland have triggered a repeat of the so-called "Sell America" trade that arose after the US announced tariffs in April last year. Investors fear potential retaliatory measures and a likely acceleration of the de-dollarization process. Add to that the still-present concerns about the US Supreme Court's verdict on tariffs and the question of Fed independence, which do nothing to reduce overall uncertainty.

The Trump administration acts as if the US is the absolute hegemon, able to unilaterally set the rules of the game on a planetary scale. But reality is already completely different, and instead of making America great again, the opposite result could occur. Such concerns are increasingly being voiced, including by US allies, putting the stability of the global monetary system as a whole at risk.

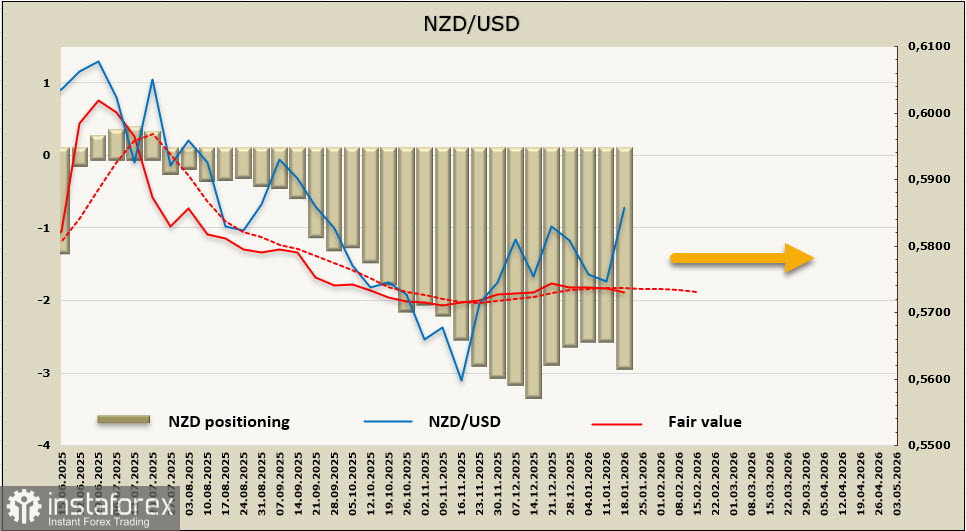

The net short position in NZD increased over the reporting week by 0.3 billion to -2.81 billion; the calculated price is near the long-term average with a downward trend.

In the previous review, we suggested that, given the lack of obvious reasons for NZD/USD to fall, we expected the development of a new bullish impulse toward 0.5910. Indeed, the kiwi has approached a four-month high since the start of the week, with a clear intention to move higher. The dollar's weakness, evident across the currency market, is supported by strong PMI increases in both New Zealand sectors, and if the Q4 inflation report turns out to be positive for the kiwi, nothing will prevent further gains toward 0.5910. The decline in the calculated price is due to speculative positioning that, so far, does not take into account the latest geopolitical developments and is therefore of limited informational value.