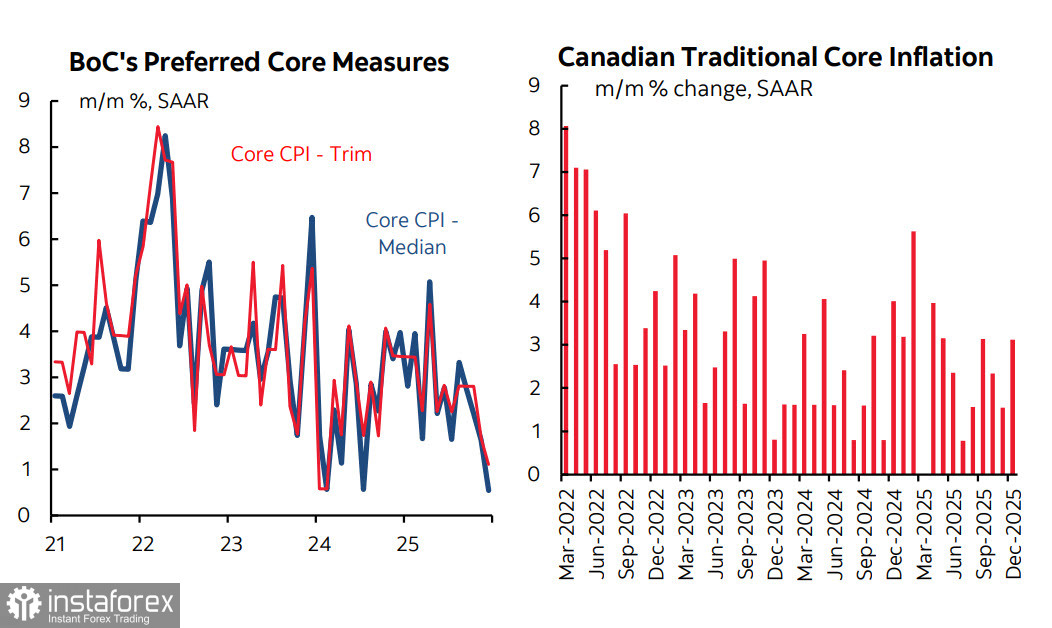

The Canadian consumer price index in December exceeded forecasts, rising from 2.2% year-on-year to 2.4%, but the markets virtually ignored this result. Part of the reason is that the core index dropped from 2.9% year-on-year to 2.8%, and since it is a key indicator for the Bank of Canada, the reaction was calm. The median inflation rate also decreased, with the trend over the last three months showing that the target and median inflation were 1.5% and 1.9% (year-on-year), respectively, both below the Bank of Canada's target of 2%.

Earlier, the Bank of Canada had already stated that it would stop adjusting interest rates unless significant events occurred, and obviously, December's inflation does not fall into that category.

Let us also note the Bank of Canada's quarterly survey on business outlooks. The overall indicator in the fourth quarter rose slightly but, in historical terms, remained at a low level of -1.78, with the share of companies expecting a recession decreasing from 33% to 22%.

Overall, changes are positive, but weak—investment intentions increased slightly, expectations for future sales turned positive, wage expectations stabilized after several quarters of decline, and inflation expectations for the year ahead decreased from 3.2% to 3.0%.

The Bank of Canada characterizes sentiments as "cautious."

Overall, the dynamics are positive, but the pace is low, which is exactly the situation the Bank of Canada anticipated, meaning that it does not plan to take any active measures in the foreseeable future.

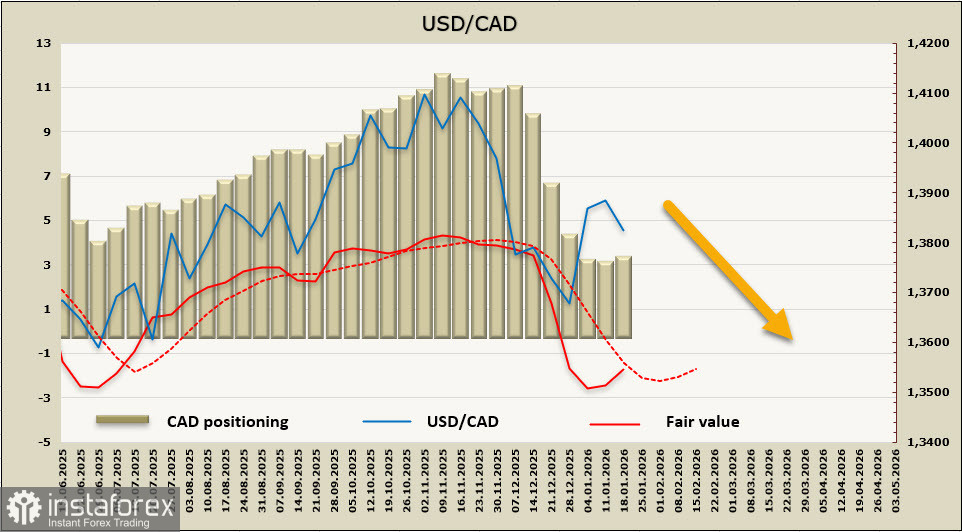

The net short position on CAD has hardly changed over the reporting week and currently stands at 3.0 billion; the calculated price has clearly lost its downward momentum but is still below the long-term average.

The USD/CAD pair resumed its decline after the correction that began at the end of December; however, this week's decline is due to developments surrounding Greenland and the broader weakening of the dollar.

No additional reasons for continuing the movement towards 1.3536 have emerged, and a stable equilibrium is observed.

Before the Bank of Canada meeting on January 28, no macroeconomic releases are expected to disrupt the loonie's equilibrium; we anticipate range-bound trading, with a slow downward shift towards 1.3536.

The situation may change if the U.S. data on personal expenditures significantly differ from forecasts in favor of higher inflation.